ICOPASS Easiest way to do KYC checks

Initial coin offerings are valuable financial tools in the cryptoeconomic era. They, having unregulated structures, provide a viable platform for illegal operations such as scams/frauds, and money laundering.

Crypto projects are backed up by ICO events where crowd sales of tokenized digital assets are exchanged for cryptocurrencies in the hopes that on completion of the project, the value of the tokens would appreciate due to the financial and systemic stability of the product.

However, large sums of money have been traded through this platform in the range of 9 figures. The estimated worth of cryptocurrencies is over $200 billion dollars within a short frame of time; this figure has been viewed to surpass early stages of venture capital funding.

ICOs have certain similarities to crowdfunding campaigns and initial public offerings. But in this case, rather than giving the investors an already established product, the owners of the project offer the promotors digitized real world assets in most cases or plainly “tokens”. These digitized assets (tokens) have been classified into two: those in the form of utility tokens and others which represent securities registered under a financial authority.

Utility Tokens: most organizations issue “utility tokens”- a basic form of digital voucher rewarded to investors granting them rights to the project’s products for sponsoring or donating to the project which is yet to commence its full operation. Tokens have no inherent ownership rights, but they are tradeable on the crypto exchange market.

Securities: on the other hand, have had their place in most ICO conventions, although most Initial Coin Offerings do not want to associate their tokens with securities nor be categorized as security trading projects due to unregulated nature of the crowdfunding activities.

One of the fundamentals of the blockchain technology is the provision of anonymity. While the blockchain ledger is made public, only the public key is accessible by the network. the private key which usually contains data of the owner are not shared on the blockchain but serve as two-step verification methods for accessing and approving fund transfer from one block to another. In other words, one would need both public and private keys to access a blockchain wallet/account.

Anti-Money Laundering / Know Your Customer (AML/KYC) juristic protocols with respect to ICO projects help prevent undue scrutiny from financial and security regulatory agents.

Since most cryptocurrencies are digitized forms of real-world assets, they retain the value of their composite tokens. In other words, once cryptocurrencies are transferred from one wallet to another or exchanged from one form of crypto to another, their respective values are commensurate with the real world asset value.

Therefore, large sums of money are laundered through the blockchain network and converted from one cryptographic currency to another until they are untraceable – in a sense.

The responsibility of KYC and AML policies cannot be relegated to a third party. Since there exists a possibility of creating cryptocurrencies and ICO projects are simple and straightforward, there is little barrier placed for the illegal market.

In other words, if viewed on a wider scale, most of the funding of crypto projects are from the illegal market with little or no interest in the projects that are proposed only meant as a means of transit to move illegal money around. In many cases, no matter how diligent or crafty the offender, there still exist a trace of analog and digital prints of the money transited.

Sophisticated investments may include the plot to reveal public keys by private investors in order to distinguish investments from black market activities.

AML associated with a Smart Contracts’ coding may just be the only way to interface between real investors with genuine resources and illicit operations of the black market, by requesting identification that are digitally mapped and stored in a database. This would invariably affect the sustainability of the ICO community, as one of the perks most online entrepreneurs enjoy from the blockchain is the maintenance of anonymity.

ICO projects without the application of an AML code embedded within the smart contract often have the tendencies to discourage Token purchase, as investors’ confidence is depleted in the project.

Although, while it may be possible to send Ether through a contract, the advance technology behind the blockchain makes it challenging to fund illicit activities.

Know Your Customer (KYC) are effective processes whereby a particular company employs a data verification system to confirm customers’ real identities solely meant to underscore the type of business partners the investor will be once the smart contract protocol has been initiated. The aim ultimately is to preclude clients with illicit objectives and crime sponsoring agendas.

Some jurisdictions make KYC/AML easier to comply with encouraging Initial coin offering activities in the long run.

Terms of service are also useful tools provided by Initial Coin Offering campaigns; they are viable legal substitutes pending when regulatory standards are released by jurisdictional interest parties.

No doubt innovations surrounding ICO projects are exponentially increasing, along with a bunch of regulatory queries to subsidized the breach in financial policies. The blockchain technology is still in its infancy, and a new economic territory currently under the auspice of the Fintech industry.

As for the financial regulators, it would be quite challenging to adapt to the evolving phenomenon as to place a concise but yet extensive regulatory function to ICO conventions and their derivatives that will neither deter the blockchain technological advancement nor expose investors to outright financial insecurity.

Businesses that want to stay ahead in the game, must put in more effort to align their objectives with jurisdictional policies while maintaining the core values of the blockchain technology.

However, ICOs must continue to uphold strict coherence with Anti-Money Laundering and Know Your Customer jurisdictional laws. As there are no current rules guiding ICO operations, the current legal premise and regulatory frameworks have been applied in many jurisdictional settings.

However, there lies the potential for crypto projects to create innovative protocols for payment gateways, fundraising, and value creation – this cannot be overemphasized. Therefore, these innovators should keep the interest of the society in mind, to ensure that their legal compliance to protect the community is a top priority at all times. This will enable them to move forward to create new and impact-driven projects.

Succinctly, most ICO projects and more cryptocurrencies are joining the train of including voluntary abidance with Know Your Customer (KYC) and Anti-Money Laundering (AML) regulatory policies for the following reasons:

Setting up a credibility factor with fiat and crypto-based Banks and payment gateways.

Futuristic purview of larger market perception of cryptocurrencies and tokens as securities.

Prolonged legitimacy

Improved investors-trust base

Extend range of influence and impact

Mitigate against regulatory fines incurred by the fault in financial policies.

As the crowdfunding activities of token sales develop and mature, more organizations (that includes startup enterprises and already established businesses) would find the need to voluntarily cooperate with AML/KYC inclusion policies as it would improve their ICO ratings and public view to attract confident investors and build trust in the project.

In a nutshell, the AML/KYC compliance policies acts as a double edge sword; first, on one hand, it helps ICO verify and validate their investor’s identity, document the investor’s profile, type of business and financial activity and finally it assesses the potential risks for money laundering activities; keeping on the good side of the law.

On the other hand, the blockchain system encourages decentralized autonomy and has been the reason many investors of varying cadre were attracted to it in the first place. With privacy policies, regulations and verification of identities, these potential whales are lost and causes a drawback in the financial pool of the ICO project in question.

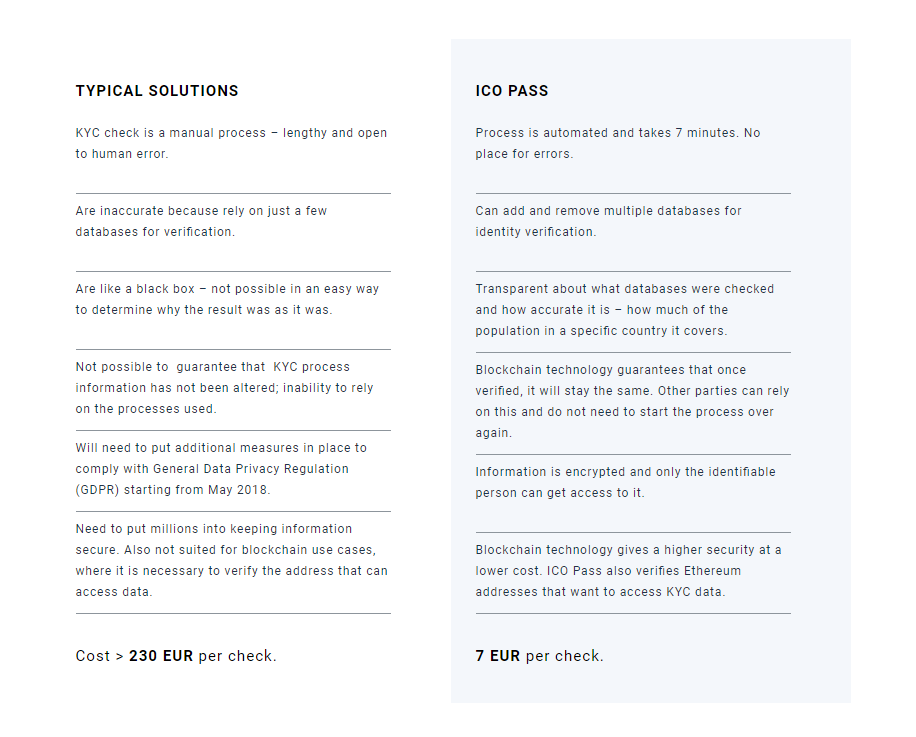

Here there is a new dispatch offered by ICOPASS in processing AML / KYC. Fast, safe, and efficient.

FAST

In a matter of minutes ICO Pass verifies authenticity of person's ID documents, does a face-matching, checks Sanction lists and the country of origin & residency.

SECURE

All data is encrypted and without the consent from person, it is not possible to have access to it.

EFFICIENT

As KYC process is automated and accurate, it is possible to significantly reduce costs. Moreover, once a person is identified - they can re-use the identity for several ICOs.

Maybe some of you also feel that so far there is a very slow procedure in processing KYC verification, with ICOPASS then all your problems will be resolved.

As a very diligent project, I know it will be very useful in the ico world, which prioritizes the use of KYC verification on each user.

Seven Reasons

Why ICO Pass beats the competition

TIMELINE

05.2016 COMPANY (NOTAKEY) ESTABLISHED

Identity solutions for UBS, Credit Suisse, Swisscom and many more are developed.

TBA ICO PASS LAUNCH

Registration starts for Token Sale.

TBA TOKEN SALE

Token Sale starts for the persons that have completed KYC.

03.2018 PRODUCT UPDATE

New databases added to ICO Pass for higher accuracy. First ICOs start using ICO Pass.

04.2018 PRODUCT UPDATE

Video identification with live agents added.

05.2018 PRODUCT UPDATE

ICO organizer communication tool added for contacting ICO contributors.

06.2018 PRODUCT UPDATE

Integration with State Revenue Services, Banking APIs for doing qualified investor check in an automated manner (US).

11.2018 PRODUCT UPDATE

Integration with State Revenue Services, Banking APIs for doing qualified investor check in an automated manner (EU).

12.2018 PRODUCT UPDATE

Interest payout functionality in app.

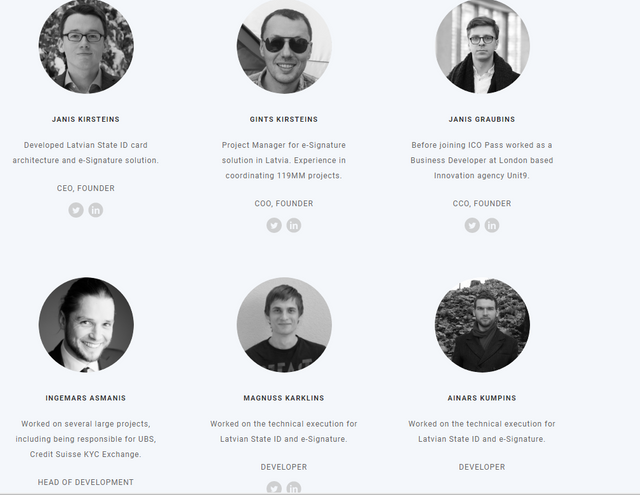

The team

ICO Pass team consists of professionals, who previously developed Latvian State ID architecture and e-Signature solution. For the last two years team has worked together with banks such as UBS and Credit Suisse on building single digital ID, before coming up with a solution for ICOs.

MEDIUM : https://medium.com/@jkirsteins/the-token-economy-ec9ef2ab728

WHITEPAPER : https://drive.google.com/file/d/1hs-RWInvpc_p7UpjIvUU1xNuqIvUi4Rn/view

PROSPECTUS : https://drive.google.com/file/d/1gQvsfRDO5LzR7AWrvv9ouPae7MNdJ3r4/view

WEBSITE : https://www.icopass.id/

AUDIT

The crowdslae base contract has been audited. The audit report can be seen here:

https://github.com/paritytech/second-price-auction/blob/master/parity-audit-final.pdf

usefull link

website : https://www.icopass.id

whitepaper : http://bit.ly/2nkGfoE

blog : http://bit.ly/2BAMtFT

telegram : http://bit.ly/2nsuMTP

github : http://bit.ly/2GtMy1E

twitter : http://bit.ly/2DHowys

facebook : http://bit.ly/2DWfAJe

Ann thread : http://bit.ly/2Fy3djF

author : 0x6b9e41aF4f0fABF7c736eB18473D803cE2C9e82e