What ICO need to know to get a bank account in Switzerland

So far, no Swiss bank accounts for ICO organizers

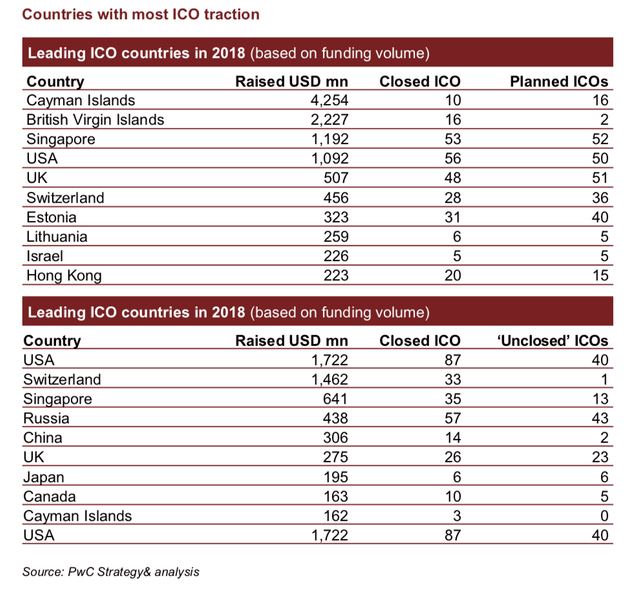

According to a study by PwC, Switzerland, together with the USA and Singapore, is one of the world's leading countries for ICOs. The legal certainty, the technology-neutral legal framework and the positive attitude of the Financial Market Supervisory Authority FINMA offer ideal regulatory conditions that motivate numerous ICO organisers to register their startups in Switzerland and conduct their ICOs from there.

Nevertheless, ICOs in Switzerland have so far been confronted with a huge challenge, which has clouded the glamour of Switzerland as an ICO location: Until recently, blockchain startups were unable to open a bank account in Switzerland to which they could deposit their ICO proceeds converted into FIAT currency. FIAT currency and traditional payment services are still a necessity for many ICOs to pay wages, rents for offices, legal fees, social security, taxes and much more.

The fact that ICOs could not open accounts with banks was mainly due to compliance reasons, especially in the areas of money laundering and fraud prevention. On the one hand, the standards for combating money laundering, and in particular for determining the origin of assets, are comparatively high in Switzerland. On the other hand, however, ICO, crypto currencies and blockchains are new topics on which compliance officers from traditional banks have hardly been able to gain any know-how and experience (incidentally, the few compliance officers with knowledge of blockchain and crypto currencies are poached by crypto banks, crypto asset managers or law firms). In addition, there are almost as many fraudulent ICOs as good and honest ICOs. It was therefore almost impossible for banks or their compliance officers without ICO experience to assess the money laundering and reputation risks associated with accepting ICO funds.

Guidelines by Swiss Bankers Association

Because they could not open accounts with a bank in Switzerland, many ICO organisers transferred their funds to banks in Liechtenstein, Malta or Lithuania or chose a different ICO location. Since blockchain companies in Switzerland now have a relatively strong political lobby and are even being heard on the national political stage, political pressure has increased on banks to provide blockchain start-ups with banking accounts.

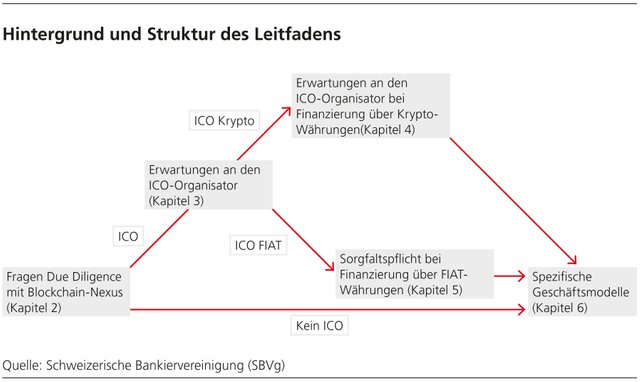

Under this pressure, the Swiss Bankers Association, together with several member banks and the Crypto Valley Association, has drawn up a guideline for opening corporate accounts for blockchain companies.

Although this guideline does not have binding legal force, it is intended to support the banks and in particular their compliance officers in correctly assessing the risks of business relationships with blockchain companies in the form of recommendations.

Guideline distinguishes according to corporate financing

The published guidelines are intended to help banks to open accounts in a differentiated manner, depending on the type of contact points that the blockchain company has with crypto currencies.

The scope of a bank's clarification obligations depends on whether the blockchain company accepts crypto currencies as part of an ICO and credits them into the business relationship with the bank in the form of FIAT currency. In this case, the documentation requirements for companies are most comprehensive. Below is an overview of the recommendations to a bank, depending on whether the blockchain company has performed an ICO or not.

- Blockchain companies without an ICO: Companies whose business model has points of contact with the blockchain technology but which do not use it for corporate financing should not be treated any differently from other SME customers who want to open an account. They are subject to the usual strict legal regulations that regulate the opening of accounts. Companies have a duty to cooperate when opening bank relationships. They must be able to demonstrate that they know and comply with all the regulations relevant to their business model. This is done, among other things, with a meaningful business plan or adequate processes and resources.

- Blockchain companies with ICO: Companies that use blockchain technology to raise public capital for business purposes by issuing tokens can do so in the form of FIAT or crypto currencies. For companies whose ICO is financed by crypto currencies, higher and additional requirements should be imposed - regardless of whether they are subject to the Anti-Money Laundering Act or not. The guideline recommends that the ICO organiser applies the relevant Swiss standards regarding the origin of funds (KYC) and money laundering (AML) when accepting crypto currencies as part of an ICO. It is also proposed that the acceptance of crypto currencies within the framework of ICOs should in principle be treated at least like a spot transaction.

Importance for ICO organizers

The guide is aimed first at banks and shows them what clarifications they should make when opening accounts for blockchain companies. However, most clarifications relate to the business model of the blockchain company and, in the case of ICO, to its investors. Of course, the relevant clarifications cannot be carried out by the bank itself, but must be carried out by the ICO organiser. Thus, the guidelines apply indirectly to the ICO organizers themselves. However, if they wish to open an account with a bank in Switzerland, the clarifications listed in the guide are mandatory. Or to put it another way: If the clarifications are not carried out, there is no possibility of opening an account.

To list all the clarifications would go beyond the scope of this post. For this reason, I would like to mention the most important ones below. For details, please refer to the guidelines themselves:

- Description of the business model

- Whitepaper with detailed description of the token

- Assessment of the obligation to be subordinated under the Anti-Money Laundering Act, ideally a subordination request to FINMA and its response to it

- Directive on dealing with risks arising from foreign law

- Identification of the Contributor (KYC) and determination of the beneficial owner, ideally independent of the fact that the respective token type is subject to the Anti-Money Laundering Act. However, if the token is subject to the Anti-Money Laundering Act, KYC must always be carried out.

- Checks in risk databases to identify politically exposed and sanctioned persons

- Risk-based background check (source of funds) and risk assessment of the wallet addresses (AML) used for participation in the ICO. This is a risk score of the contributor's blockchain wallet or of blockchain transactions processed via it. This check should always be carried out in the case of increased risks.

- Choice of a Crypto Exchange, which itself applies appropriate KYC and AML standards.

- Reporting suspected money laundering to the Money Laundering Reporting Office (MROS)

These clarifications must be carried out before or during the ICO, depending on the ICO, but not afterwards, as it is then too late.

Conclusion

The yardstick for opening a bank account is certainly relatively high for blockchain companies in Switzerland, especially for start-ups that want to carry out an ICO. However, this benchmark is not only set by the recommendations of the Swiss Bankers Association, but also by FINMA's ICO guidance, which was issued earlier this year. FINMA's ICO Guides only comment on the question of which token category is subject to the Anti-Money Laundering Act. The guidelines of the Swiss Bankers Association then specify what must be done if a token is subject to the Anti-Money Laundering Act.

But regardless of whether the due diligence is carried out by the bank or by the ICO organiser, it should contribute to a better quality of ICO and last but not least to more investor protection.

Sources: https://www.pwc.ch/en/publications/2018/20180628_PwC%20S&%20CVA%20ICO%20Report_EN.pdf