GET CREDIT SERVICES FOR FINANCIAL IN EASY WITH JOIN TOGETHER WITH L-PESA

GET CREDIT SERVICES FOR FINANCIAL IN EASY WITH JOIN TOGETHER WITH L-PESA

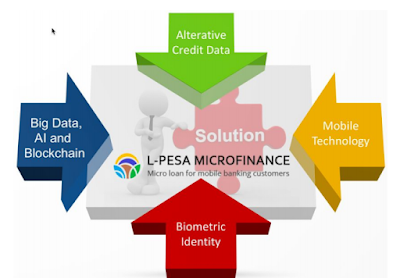

For most people is in need of capital loans. With a capital loan they can advance their business. If the loan is used appropriately then, their business will be fast, to grow. Seeing that L-Pesa created a smart blocker-based loan, which could make people all over the internet to advance their business and become successful entrepreneurs. A reliable visionary can take a loan in Ether or bitcoin and can then join the L-Pesa market that facilitates peer-to-peer loans that are the first crypto loan service in Africa. L- Pesa is a company that has validated its operation model over the last 18 months and has built advanced technology, automating most operations. about 25%. There are four important market forces gathered for scaling. Among them are Big Data, Artificial Intelligence and Blockchain, alternative credit data, mobile technology, biometric identity. However, traditional microfinance has limited reach, and the solution is targeted to poor farmers and small business owners. The middle class consumers and business owners in developing countries can not apply for credit, but the current financial infrastructure in these countries

does not support underwriting credit. The current marketplace presents a number of issues including:

Underwriting. Traditional consumer and business credit reports used for underwriting loans in developed countries are generally unavailable, and loans without underwriting rights will result in high loss ratios.

Lack of bank credit. Traditional bank loans are not widely available in developing country residents.

microfinance only targets agriculture only on traditional microfinance institutions that typically provide loans to poor farmers in rural areas. Middle class consumers

do not have access to microfinance

Outdated Operating models of banks as well as microfinance institutions are already high overhead costs, struggles with lack of data for underwriting loans, and generally fail to be taken

advantages of new technology

Microfinance is targeting the poor only to consumers, farmers and small business owners in Indonesia. Developing countries above the lowest poverty levels have little chance of getting credit.

Most consumers are un-banked. Many consumers, farmers and small business owners in developing countries do not have bank accounts.

Solution

The solution of the barriers presented above is described as barikut:

Large Data, Artificial Intelligence, and Blockchain The new tool enables the storage of large amounts of data and extensive data analysis at a fraction of the cost some years ago.

Advances in Artificial Intelligence provide a new opportunity for automated loan underwriting. Blockchain technology allows for faster, more secure, and

exchange rate is cheaper. Blockchain technology has just begun to revolutionize financial services and will result in enormous efficiencies over the next ten years - the blockchain has been described

as internet money and will do for internet financial services for information and

trading.

Alternative Data Credits. Just a decade ago, there was little data available in most people in the world. This has changed with the emergence of social media and related trends of new tools that have been developed to make this data useful for decision making in underwriting loans. L-Pesa has developed a unique exclusive credit with

a model based on user behavior combined with traditional and alternative credit data. L-Pesa competitors have developed their own proprietary models. The experience over the next decade will lead to revise best practices, which ultimately become the industry standard.

Mobile technology. The rise of mobile phones over the past two years has been one of the most profound, technological and market changes in human history. Most humans now have mobile phones, and many own-owned smartphones. Mobile financial services such as M-Pesa have been available in many countries and support both banked and unencumbered populations. Based on market penetration of mobile phones (smartphones and feature phones), mobile money services like M-Pesa, Tigo Pesa and Paytm have very fast growth and have enabled L-Pesa.

Biometric identity. Traditional microfinance relies heavily on large branch networks since identity verification, online and directly. India's Aadhaar biometric ID system leads

world and has registered 99% of India's 1.2 billion people. Other countries that are expected to successfully follow India for the implementation of biometric ID will be generated dramatically reducing the cost and ability to provide financial services without a physical branch of the network.

L-Pesa Service System

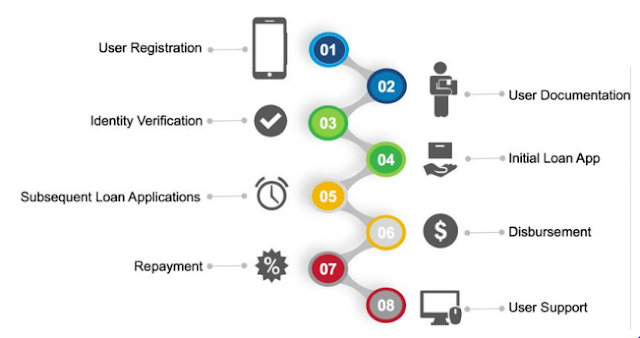

Users register accounts in L-Pesa, often in response to social issues

media messages or SMS marketing messages. Over time, L-Pesa expects a large number of accounts to come from existing user referrals.

Users add documentation to their L-Pesa account, usually

identification documents such as driver's license or passport

Users register accounts in L-Pesa, often in response to social media messaging messages or SMS marketing messages. Over time, L-Pesa expects

that a large number of account openings will come from referrals from existing users

Users apply for initial loan, usually for local equivalent to $ 1.00. In many cases, this app automatically

The next loan application is handled in the same way: automation

Based on the user's credit score is the key to success and scale

Once the loan is approved, the disbursements are processed in real-time

mobile money services such as M-Pesa or Tigo Pesa.

Users are given a payment plan and are expected to do regular

loan payments. Repayment is also made using mobile money service. Users can make prepay without penalty. Payment arrears will be

impact the user's credit rating and will generate automated messages to the user. Handling delinquency is very efficient, resulting in a loss ratio of less than 10%.

User support is handled by the L-Pesa back-office team in Tanzania. User support is available in English

Target market

The L-Pesa market target is a market of 40% of the population in the continent of Africa, India and southeast Asia. Its population is 3 billion and the population is growing very fast. India

is at 92% penetration and many African countries are above 70%. L-Pesa

work on smartphones and feature phones. L-Pesa relies on mobile money service providers for liquefaction and collection, making the process quick and efficient. Many countries were initially targeted by L-Pesa to have a high proportion of un-banked service populations

on mobile money like M-Pesa is a good choice. India has a higher level

percentage of population with bank account, and Aadhaar biometric ID

The database is now connected to the bank account, making the disbursement and

Collections in India are potentially very efficient in the near future.

Dependency on African money service users restricts L-Pesa users

basis for users with mobile money service wallet. Until mid-2017, there

about 170 million wallets are used in Africa. In India, more than 1 billion

Aadhaar users have connected their bank account.

The available L-Pesa market will far exceed L-Pesa's loan capacity

and all its competitors in the future. Limiting factor for

Growth is not expected to users will want to try L-Pesa but vice versa

availability of capital for loans.

The key business model of L-Pesa is:

● A highly automated back office system that allows virtually complete task automation tasks

● Integration with mobile money providers to obtain efficient loans

disbursement and collection of payments.

● The process of loan origination is very efficient - fully online and almost

fully automatic

● Model of customized credit rating that has been adjusted

The first 35,000 loans issued by L-Pesa resulted in a loss ratio below 10%.

Advantages

L-Pesa customers have access to affordable financing options

helping them improve their lives

Provider of third party capital L-Pesa may use its capital

get interesting results

Shareholders and employees of L-Pesa can obtain reasonable returns on their investment and workforce

Token L-Pesa

Token name: KRIPTON

Token ticker: LPK

Owner Token: L-Pesa International Business ltd., Gibraltar.

Financial Auditor:

Token type: Ethereum ERC20

Total Token issued: a maximum of 3,200,000,000. The final amount

the token created will be calculated according to the final contribution amount.

The final number will be issued at the end of ICO.

Bonus: during the pre-sale period, the participant will be eligible for

the following bonuses:

A. Tier1 - During the first 4 days - 15%

b. Tier2 - Over the next 14 days - 10%

c. Tier3 - Over the next 28 days - 5%

d. Tier4 - Over the last 14 days - 0%

Day bonus amount

Airdrop for 30 days no bonus, Presale 30 days 25%, Level 1 4 days 15%, Level 2 14 days 10%, Level 3 28 days 5%, Level 4 14 days 0%

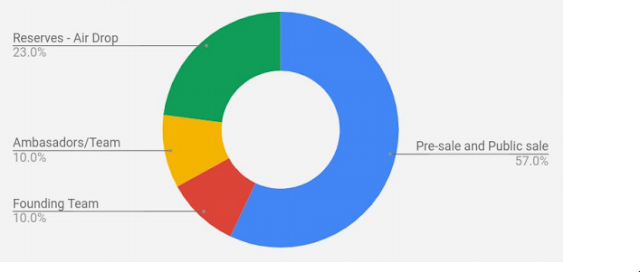

Token distribution

57% Public (out of all created tokens),

Team and Advisory 20%,

Bounties Program 1%

22% Reserve (airdrop)

Locking period: L-Pesa underwent 12 months of confinement.

Transfer Token: Token will be transferred to buyer upon payment of ICO confirmation / settlement. Token will be activated only after ICO completion. Furthermore, token transfers will only exist

probably after successfully completing ICO.

Intelligent Crowdfunding Contract

The campaign will have two general stages:

Presale, where the minimum contribution amount will be set

up to 5 ETH and bonuses offered will be 25%. Presale will take place for

30 days.

General sales, where there will be no minimum contributions and bonuses offered are as follows:

a. During the first 4 days - 15%

b. Over the next 14 days - 10%

c. Over the next 28 days - 5%

d. Over the last 14 days - 0%

Public sale will last for 60 days.

The minimum funding objective (soft cap) is $ 5,000,000 and the maximum of funds received (hard cap) is $ 25,000,000. One token tentative price is USD 0.01.

Let's join before the pre-sale token!

You will get 1,000 coins ($ 18.00) for free directly to your wallet

Coins automatically exchange tokens when distribution begins.

Sign up below to get your free coins right now!

LIST

L- Pesa ICO timeline

Pre-sale ends on April 9, 2018

ICO starts on 10 April 10 2018

ICO expires on 10 June 10 2018

Wedsite: https://kriptonofafrica.com/

whitepaper: https://kriptonofafrica.com/static/pdfs/L-Pesa_ICO_white_paper_Jan_7_2018.pdf

ANN: https://bitcointalk.org/index.php?topic=2873068.0

facebook: https://www.facebook.com/kriptonlpk/

telegram: https://t.me/joinchat/HbNNkBLQJkw7765Ri7tg7w

twitter: https://twitter.com/LPesaMicrofin

bounty: https://bitcointalk.org/index.php?topic=2910183.0