Concerning delayed gratification in regards to annual tax returns

Receiving one’s tax return can seem like a windfall for an average wage-earner. You rigorously stick to a budget that begrudgingly yields piecemeal scatterings of spare cash week to week, allowing little in the way of big-ticket spending outside of reaching tentatively for that well-worn credit card… Then once a year at tax time you get a lump-sum return thanks to a diligent accountant or studious application of one’s own expense-claiming expertise. There it sits, in your account, a sum of cash you’re not used to seeing on your balances page, and you want to go out right this instant and purchase the 4K TV of your dreams. You want to put that sudden windfall to immediate effect and treat yourself. It’s tempting, and I think it’s fair to say we’ve all used that tax-refund in a manner that is perhaps not the most conducive to securing a stable financial future. I certainly have.

There is, however, a way to afford many 4K TVs, a room full of gadgets humming softly with the sound of cooling fans which perhaps echoes one’s own awed sounds of gorged satiation. It does take, and here’s the rub, delaying your immediate gratification for a big payoff in the near-term future. As we are wont to do, Countinghouse has looked at average Australian tax return statistics as well as other pertinent factors and uncovered just how impactful diversifying one’s annual tax return can turn out to be.

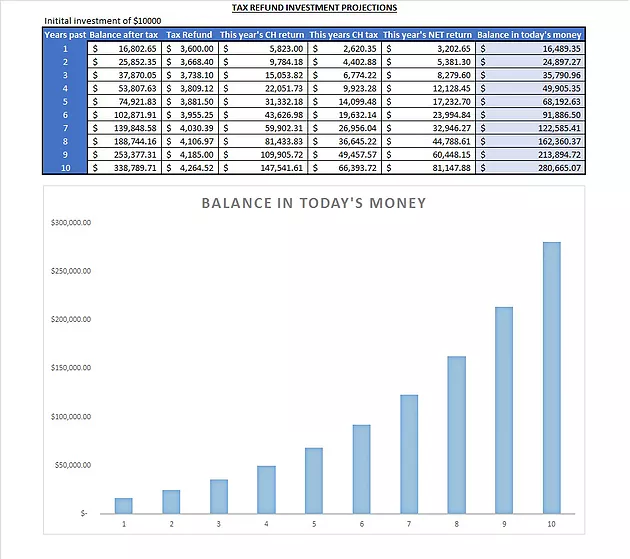

The average Australian tax refund is $3600 per year. With income inflation factored at 1.9% per annum, average returns from a high-yield portfolio like Countinghouse Fund’s algorithmic trading products factored here at a conservative 58.23%, and tax factored with a rate of 45% per annum we can draw a projection that shows what investing one’s returns could potentially yield (Figure One).

Figure One: Showing the impact of re-investing one’s annual tax-return

What you see above is a hypothetical case study where an individual has invested their tax refund each year, after an initial investment of $10,000 (Which can of course be saved up for using tax returns). Tax is shown to be paid for the growth each year, which is assuming this individual took all profit from their investment per year and didn’t simply hold on to their portfolio’s profit long-term. What can be seen is the offset provided by the annual investment of an individual’s tax return on the income tax payable from their capital gains. What can also be seen is a healthy profit.

Utilising a tax refund in this manner can significantly impact an investor’s portfolio over a ten-year timeframe, allowing for the purchase of many guilt-free televisions provided one invests now for future gain.

Sources:

-http://www.abc.net.au/news/2017-02-22/wage-growth-remains-at-record-lows/8293704

The use of a tax refund in this form can significantly impact an investor's portfolio over a ten-year period, allowing for the purchase of a lot of fault-free television provided one invests now for the future benefit".,"

Tim Dawson,Mike Pomery is our Director

Visit Please : https://www.countinghousefund.com/ico

#CHT #Countinghouse #hedgefund

Very useful information. Thanks.

Tim Dawson,Mike Pomery is our Director

Visit Please : https://www.countinghousefund.com/ico

#CHT #Countinghouse #hedgefund