Homelend Platform designed to modernize the hypotharoid P2P system

Hello friends! In this opportunity, I will share information about a new and fantastic project that goes by the name Homelend is a decentralized platform that allows the next generation of mortgage financing for homebuyers. Homelend creates an interface for direct interaction between borrowers, lenders and other parties involved in the mortgage value chain. By doing so, it allows crowdfunding of mortgages using a peer-to-peer model with the security, transparency and automation provided by distributed ledger technology (DLT) and smart contracts.

The Homelend platform is designed to modernize the current mortgage system in order to make it more functional, operationally effective, efficient and customer-focused. The platform will be more fabulous and pious in its operations. It will also expand the ability of people to borrow and borrow to have a good home. This will adapt to them and their lifestyles. Therefore, your lifestyle or your employers do not affect the loan or loan process that Homelend offers. This will be done through Ledge Distributed Technology (DLT) and crypto smart blockchain contracts.

This will lead the lenders and borrowers to harmony in a more rational automated process that will be transparent and modest for the users.

How does Homelend work?

1- Each pre-approved mortgage will be divided into smaller identical units. For example, John wants a loan of $ 200,000. But first the platform will divide it into twenty units of $ 10,000. Let's call these units, "Slices."

2- Each of these twenty Slices will be assigned a risk score, which the lenders can access in the terms of the pre-approval of the loan. The higher the risk score, the higher the interest rate.

3- People will have the opportunity to lend financial resources to borrowers by purchasing these Slices. A lender does not have to buy all slices from a lender. He or she can lend money to as many borrowers as they want by purchasing different pre-approval mortgage loans.

That means that John's $ 200,000 loan will be provided by twenty different lenders.

4- The crowdfunding is finalized only after buying the Slices of a pre-approved loan. The mortgage will be sent to the final closing. Note that individual investors will have 30 days to finance Slices. If all the slices are not sold within this period of time, the process will be canceled and all investors will recover their funds.

Perhaps the most important part of the whole system is the use of the cryptocurrency for the financial flow, although the prices of the listed houses, the amount of pre-approved loans and their "Slices" are determined by decree.

Main Features of Homelend:

Homelend P2P Mortgage Loan Facility

The point-to-point loan (P2P), also known as "alternative financing", is the process by which people can borrow and lend to each other without the intervention of banks or other financial intermediaries. The Homelend P2P platform works by incorporating the commercial logic of mortgage loans into intelligent contracts. This is the main functionality of the platform. By creating a set of smart contracts that execute business processes, HomelendIt allows people to borrow money from their peers in a reliable, transparent and secure manner. The key idea is that borrowers and lenders are not linked through a financial intermediary (ie, a bank or a centralized P2P loan platform), but through intelligent contracts that automatically execute a predefined business logic.

Financial flows

At Homelend, the flow of financial resources from lenders to borrowers (and ultimately sellers) is executed only through intelligent contracts. There is no financial intermediation, control or decision making by Homelend, after a buyer receives a preapproval of the system, with respect to a specific property, the corresponding mortgage loan is "on the list" on the Homelend platform. By then, the borrower has committed a specific initial payment and the amount of the mortgage is determined.

Commercial model

Homelend is being developed as a blockchain solution that will significantly increase the possibilities of financing housing for many people and families. Our value proposition is socially sensitive and anchored in a progressive P2P approach that aims to use technology for the benefit of society. However, Homelend is also based on a solid and profitable business model, which consciously extends to address an unattended market. On the one hand, Homelend creates an investment opportunity for many people, with a solution that unites a traditional industry such as real estate with innovative technology such as blockchain. On the other hand, it makes it possible for many people (who due to various circumstances, including the current limitations in traditional models of credit risk.

An archaic $ 31 billion economy that craves interruptions

The United States mortgage market is worth $ 14 billion, and the global market is expected to reach $ 31 billion by the end of 2018. However, no matter how socially and economically the market is, the traditional mortgage loan system It is still very primitive, based on a long and complex paper-based process that involves several intermediaries, a process full of inefficiency and overload for borrowers and lenders. In addition, most mortgage loans are not affordable for a new generation of young borrowers, including millions of creditworthy people who obtain a mortgage loan due to outdated evaluation criteria.

Homelend advantages:

From manual and extensive to simplified and efficient

By incorporating predefined business logic into intelligent contracts, scanning documentation and eliminating unnecessary processes, Homelend will automatically execute an end-to-end origin process, reducing it from 50 days to less than 20 days.

From Ambiguous & Clunky to Transparent and easy to use

Homelend aims to create a loan process that is not only intelligent, but also simple and fair. It will allow borrowers to easily request a loan, track the status of their application at all times and interact directly with the mortgage lenders.

From costly to profitable and intermediate intermediation free of charge

The immutability, security and transparency provided by DLT allow transactions, including loans, to be recorded without banks acting as intermediaries. This will reduce costs for borrowers and lenders, while minimizing the distance between them.

From Vulnerable and unreliable to Reliable and secure

Centralization and paper processes are the key factors behind the insecurity and vulnerability that characterize the traditional mortgage industry. DLT's unique features and smart contracts allow Homelend to provide a platform for people to exchange large amounts of money reliably, transparently and securely.

Main methods you will use:

P2P LOAN METHODS

It is expected that Homelend will present three methods of peer-to-peer lending. These include; pure crowdfunding, grouping and auction. Let's explore them, okay?

METHOD OF CROWDFUNDING

This is the simplest method where potential lenders are expected to find investment opportunities in the form of "Slices". Different investors will be able to finance pre-approved mortgage loans by the borrowers through these segments.

POOLING METHOD

Unlike crowdfunding, lenders will have the opportunity to invest through an intelligent contract before the approval of the specific mortgage loan. The same principles of purchase of "Slices" that crowdfunding applies. The only difference is that; the lenders will be able to pre-purchase them.

The main advantage of this method is the level of financial cushioning it offers without the need for an intermediary.

AUCTION METHOD

The auction is not expected to offer any form of financial cushioning. It looks more like crowdfunding, except that lenders will have the ability to offer borrowers better conditions than the platform pre-approved.

TOKEN GENERATION EVENT

To serve the economic dynamics of the platform, a token generation event will be organized. It is assumed that the HDM token offers access to the services offered on the platform. It does not matter if the services are provided by Homelend to third parties that work with Homelend, users will still need the token.

Token

On the platform, the HMD card will be used as a means of payment.

Standard: ERC201

ETH - 1,600 HMD

The total amount is 250,000,000

Soft cover: $ 5,000,000

Hardcover - $ 30,000,000

Distribution of tokens

36% - basic sale

28% - preliminary sale

20% - reserve fund

8% - advisors and rewards campaign

8% for the team

Distribution of funds

40% - project development

35% marketing

25% - for the team

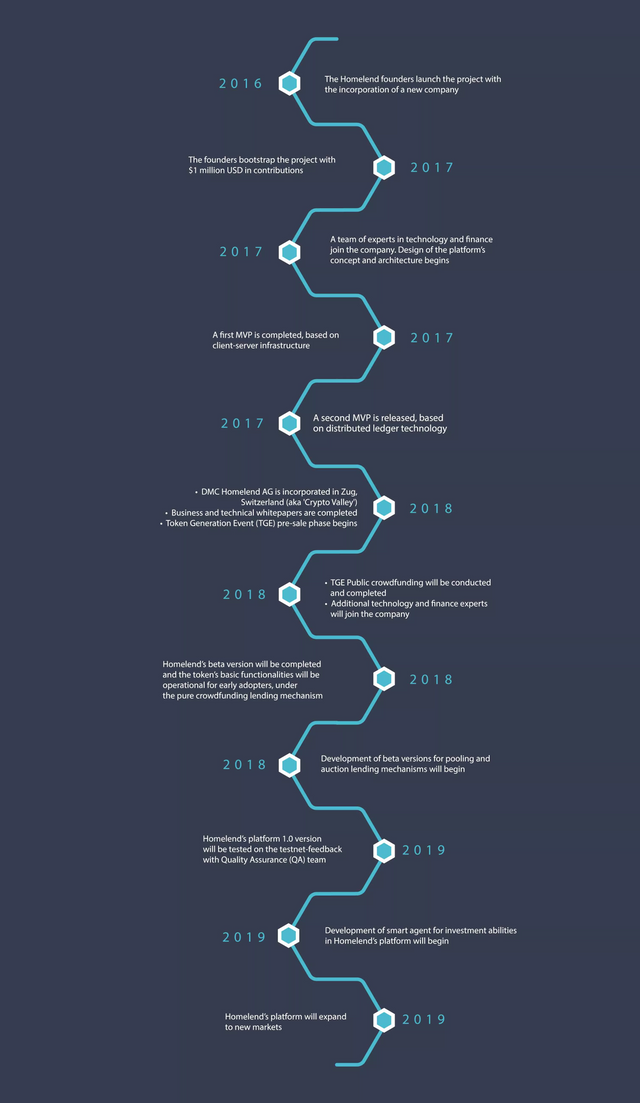

Route map:

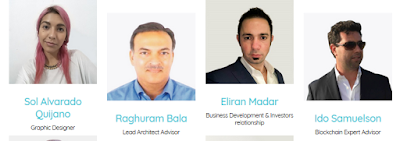

Team of Visionaries:

Under what legal framework does Homelend operate?

DMC Homelend AG was established in Zug, Switzerland, also known as 'Crypto Valley'. The initial offer of currencies (ICO) will be carried out based on the guidelines and the publication of the regulated

Important links

User: cococoins

Profile Bitcointalk: https://bitcointalk.org/index.php?action=profile;u=2015961

Email: [email protected]

Portfolio: 0xC6290409EA01419C11E80e86d0be57bF6a85Eb33

Telegram: @cococoinss