Internal Rate of Return of Infinite Banking Whole Life Policies

Sometimes when demonstrating the value of an Infinite Banking designed Whole Life policy, the conversations steers toward the return on the cash values (also called IRR- internal rate of return) and the conversation gets stuck there.

The purpose of this article is to get mentally unstuck so we can get beyond rate of return conversation because the true value of the Infinite Banking strategy is the ability to redirect cash flow back towards our own personal economy instead of through a traditional bank.

The fact we can obtain a Whole Life policy to perform this banking function AND get around 5% IRR based on today’s interest rate environment without taking any market risk should be the cherry on top.

That said, let’s do a deeper dive into the IRR so we can get past this limited rate of return mindset once and for all and instead judge the strategy for it’s value as whole versus just one attribute.

First, I need to share that Whole Life policies when designed for Infinite Banking purposes take advantage of a very special rider called a Paid-Up Addition Rider (PUA). This particular rider turbo-charges the cash value from day 1. Without this rider a person does not have a properly designed Infinite Banking whole life policy.

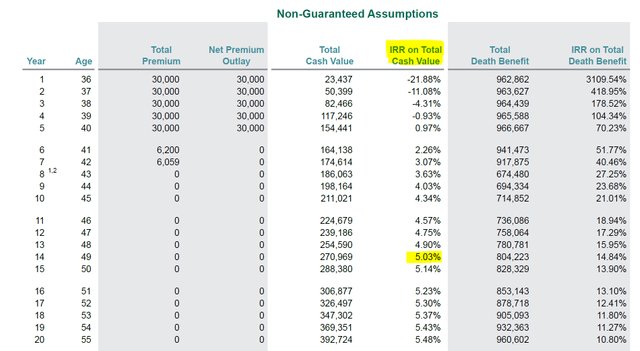

Second, interest growth is guaranteed for the life of a whole life policy but dividends are not. That said, each of the life insurance companies I represent to implement Infinite Banking policies have an unblemished record of paying dividends for over 100 years and counting. For that reason, the illustration below will include non-guaranteed assumptions (interest AND dividends).

Third, when viewing the illustration below try to understand that this projection assumes the dividend scale will remain unchanged for life. Dividends are highly influenced by current interest rates which have been hovering at all time historic lows since 2007. The scales illustrated in today’s whole life illustrations reflect this ultra-low interest rate environment which is to say two things: interest rates could possibly go lower or, interest rates will increase in the near future causing dividends and the IRR to increase over time. You can decide for yourself which seems more likely.

This illustration is based on a 35 year-old in excellent health wanting to re-direct existing assets into a requested Infinite Banking whole policy. Funding is $30,000 a year for 5 years. (Interesting anecdote is that this person is a well connected financial executive for a Wall Street firm, accustomed to managing his own portfolio, and he sought out an Infinite Banking policy for a small portion of his overall portfolio in order to reduce overall volatility, taxes, and provide death benefit protection for his wife and future kids.)

In year 14 I’ve highlighted the IRR on total cash value. It’s in that year that the cash values have reach 5% annualized from the policy inception. Again, this is assuming dividends continue each year and there is no reduction or increase in the current dividend scale. Both the client and I agreed were safe assumptions.

Some people might sneeze at the 5% IRR, especially in light of the current bull market in equities which is the 2nd longest on record. If you are one of these people, remember this illustration was presented to a financial executive who was able to see the bigger value once we discussed the 5% IRR in context to the overall bigger picture. Let’s touch on some of the points I discussed with him.

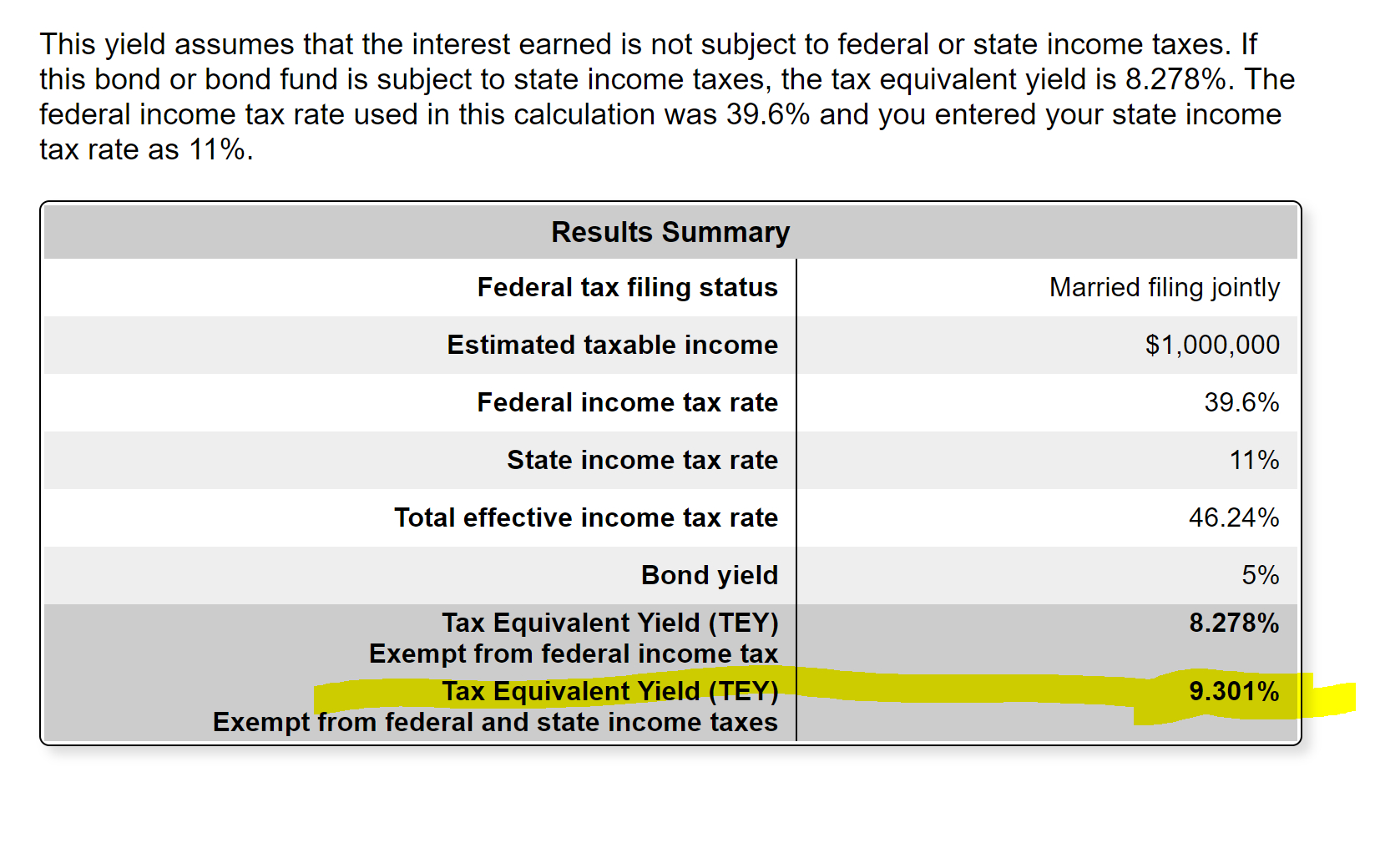

First, let’s look at the Tax Equivalent Yield (TEY) an individual would have to earn in mutual funds just to equal the 5% IRR in the above IBC policy. (I used the calculator at https://www.bankrate.com/calculators/retirement/tax-equivalent-yield-calculator-tool.aspx)

The “bond yield” of 5% is in fact the whole policy IRR in the calculation. I highlighted the Tax Equivalent Yield you’d have to get every year just to match the policy returns. In the example below, I’m working with a client with $1,000,000 household income in the state of California. (I held the California state tax at 11% to offset the new lowered federal tax bracket of 37% for 2018.)

This individual would have to earn 9.301% and do so EVERY YEAR in his mutual fund portfolio just to equal the 5% IRR in the Infinite Banking policy I designed for him. That’s a huge amount of risk to take on to yield effectively the same return after taxes.

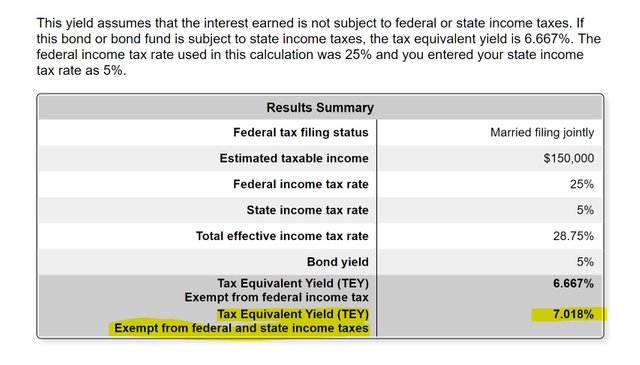

What if your household income isn’t $1,000,000?

Let’s use a household income of $150,000 instead and I’ll adjust the state tax to 5%. You’re still looking at having to achieve a 7% rate of return on your stock portfolio in order to mirror the comparable growth in an Infinite Banking designed Whole Life policy. See below:

One other big point to consider with a mutual fund portfolio are the annual taxes to be paid out of pocket each year. Side note, capital gains taxes can occur even if your fund has a negative annual return. (I learned this miserable lesson when I was in college and had been encouraged to open a mutual fund in order to get a free checking account.)

Owning an IBC designed whole life policy will actually reduce taxes in comparison because the cash values grow without having to pay taxes on it like you do with managed money in taxable accounts or money kept at bank.

I know in theory growing a portfolio at 8-10% seems great but it’s an entirely different story when you are having to pay a larger amount in taxes just maintain a stock-based portfolio. That’s a major reason why “financial pundits” will recommend a 401k retirement plan because the growth is tax-deferred. You don’t feel the pain of taxes each year like the “Buy Term and Invest The Difference” crowd.

For those who are seeking to diversify their portfolio with an uncorrelated asset class versus an alternative to a 401k, there is quite a bit to be said about carving out a portion of a portfolio that has no market risk and no future taxes. From that point of view, how much of your portfolio in this type of asset class makes sense? 5%, 10%, 15%... You tell me.

By redirecting even a small portion of funds to a properly designed Infinite Banking policy, you actually reduce overall portfolio volatility and taxes. And if you’re finally no longer stuck on the true value of that 5% IRR, you’ll find peace of mind knowing that this strategy will give you the ability to own and control your own Family Bank while protecting your family with a death benefit that you’ll always have.

In summary, to better understand the value of Infinite Banking, it’s really important to get beyond the IRR as if it were the only benefit to the strategy. To paraphrase Nelson Nash, creator of the Infinite Banking strategy, it’s like majoring in the minors!

John A. Montoya

JLM Wealth Strategies, Inc.

(925) 386-6639 Office

(888) 472-9757 Fax

Bank On Yourself® Authorized Advisor

IBC® Authorized Practitioner

CA Life#0C42222