(IJCH) Business Loans and Your Personal Credit

(Meaning: My Warped, Personal Opinions and Musings)

{kind=link}

From the Author:

Salutations.

I am JaiChai.

And if I haven't had the pleasure of meeting you before, I'm delighted to make your acquaintance now.

I invite you to interact with everyone, learn, and have as much fun as possible!

For my returning online friends, "It's always great to see you again!"

Business Loans and Your Personal Credit

As a new (or prospective) small business owner, it's natural to wonder, "Does a business loan affect personal credit?"

The answer to this question is not so clear cut.

Whether a business loan can affect the status of your personal credit depends on these 3 Key Factors.

#1. Personal Guarantees

The overwhelming majority of small business loans are guaranteed by people just like you - an individual small business owner, a sole proprietor.

As such, you are the Guarantor of that loan and ultimately responsible for

any unpaid debt from the business loan.

In short, the lender will soon come looking for you if your company does not adhere to the agreed upon payment schedules.

If you don't pay, the lender has every right to report your negative consumer behavior to a credit bureau; causing your personal credit score to diminish.

What about "Business lines of credit" and "Business credit cards"?

{kind=link}

Contrary to popular belief, a line of credit or credit card that is labeled "Business" is not a magic shield that will protect the business owner from paying for the financial misdeeds of his company.

In reality, a "Business line of credit" or "Business credit card" is treated the same way as a business loan.

If you guarantee it, you implicitly agree to pay any unpaid debt incurred by your company - including unpaid advances on your "Business line of credit" or missed monthly payments on your "Business credit card."

If preserving your personal credit score is the goal, the use of personal, non-business funding (i.e., personal loans, home equity loans, "emergency" loans, personal credit cards, etc.) is totally foolish.

Going that route ensures that any missed payment can easily trigger negative reporting that causes your personal credit score to tumble.

Devastating business losses still do not absolve you from the obligations of personal loans or consumer credit card debt.

In the end, delinquent or sporadic payment behavior only ruins YOUR, not your business', credit worthiness.

I strongly recommend you consult a tax lawyer or CPA before going the non-business loan route. There might be an alternative funding method for you that you are not aware of.

For example, did you know that a loan against your 401(k) or other retirement plan, doesn't show up on any consumer credit reports?

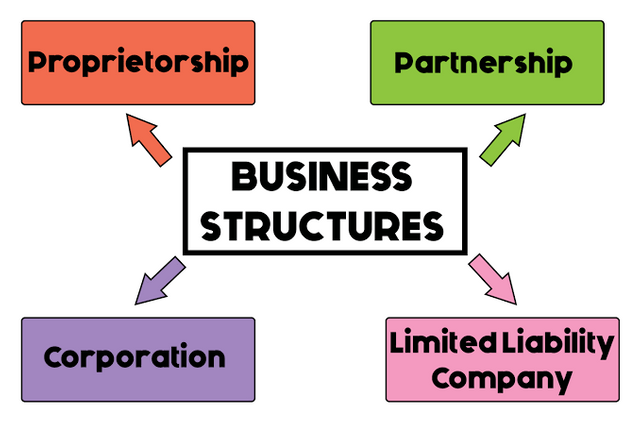

#2. Business Structure

According to U.S. Law, “As a sole proprietor, your business and personal credit are considered one and the same."

Other business structures (such as an LLC, S Corp. or C Corp.) can separate your business' financial operations from your personal finances.

You should investigate the advantages and disadvantages of those business structures and compare them to what your sole proprietorship currently offers.

If you decide that another business structure might be better, the next step should be a consultation with a business lawyer or CPA to discuss the eligibility requirements, fees, tax schedules, etc.

#3. Lender Policies

Most lenders and creditors will, without proper disclosure in advance or applicant consent, check personal credit reports during the business loan application process.

Be wary.

These inquiries are not benign and definitely have a negative effect on your personal credit rating.

BEFORE signing any loan application, ask the lender, "Will you be checking my personal credit report."

Then you can, based on the lender's response, decide to proceed or walk away.

Loan reporting policies vary greatly from lender to lender. Some report all their loans to the credit bureaus as soon as proceeds are handed out.

Others have a grace period or don't report at all. It all depends on the local business laws governing their business operations.

The same goes for reporting cases of chronic and willful noncompliance, fraudulent financial disclosures and an assortment of other malevolent actions considered "negative consumer behavior".

One lender might submit a negative report to a credit bureau after a singular missed payment, while others have a grace period or offer alternate payment options before submitting a negative report.

Before signing anything, review the whole contract.

Be especially keen on the wording describing the degree of your personal guarantees.

What are you specifically agreeing to do under the loan contract?

Are you putting up anything as collateral?

If so, is it fairly appraised and on an industry accepted depreciation schedule?

What is the lender specifically promising to do for you (e.g., loan amount, interest rate, maturity date, penalties, etc.)?

What is the lender's policy and timeline for recoupment of loan value or seizure of collateral should you default on the loan?

Always take the time to read the fine print of any contract you put your John Hancock on.

Key Points to Remember -

Review what your Personal Guarantees actually imply.

Investigate alternate Business Structures, especially if you're a sole proprietor.

Verify the lender's credit check practices and loan reporting policies BEFORE signing any loan application.

Avoid getting a non-business loan or using personal credit cards to fund your business.

Talk with a business lawyer or CPA to discuss your prospective business loan, its potential effects on your personal credit rating and explore other methods to fund your business; especially the ones with less potential for adversely affecting your personal credit record.

By JaiChai

And if you liked my post, kindly Upvote, Comment, Follow, and Resteem.

About the Author:

.jpg)

Believing that school was too boring, he dropped out of High School early; only to earn an AA, BS and MBA in less than 4 years much later in life – while working full-time as a Navy/Marine Corps Medic.

In spite of a fear of heights and deep water, he performed high altitude, free-fall parachute jumps and hazardous diving ops in deep, open ocean water.

After 24 years of active duty, he retired in Asia.

Since then, he's been a full-time, single papa and actively pursuing his varied passions (Writing, Disruptive Technology, Computer Science and Cryptocurrency - plus more hobbies too boring or bizarre for most folk).

He lives on an island paradise with his girlfriend, teenage daughter and two dogs.