Financial- Literacy-And-Financial-Health

Even though you may have completed your education, you're not done acquiring financial literacy. It's best to be proactive. Even if you didn't learn money skills at home or at school, it's never too late to catch up. Re-aligning your focus and adjusting your finances now will make all the difference for your future.

What is financial literacy?

Financial literacy is the ability to understand and effectively apply various financial skills, including personal financial management, budgeting, and investing. Financial literacy helps individuals become self-sufficient so that they can achieve financial stability.

%20(2).jpeg)

Understanding Financial Literacy

Financial literacy also involves the proficiency of financial principles and concepts, such as financial planning, compound interest, managing debt, profitable savings techniques, and the time value of money. The lack of financial literacy may lead to making poor financial choices that can have negative consequences on the financial well-being of an individual. Consequently, the federal government created the Financial Literacy and Education Commission, which provides resources for people who want to learn more about financial literacy.The main steps to achieving financial literacy include learning the skills to create a budget, the ability to track spending, learning the techniques to pay off debt, and effectively planning for retirement. These steps can also include counseling from a financial expert. Education about the topic involves understanding how money works, creating and achieving financial goals, and managing internal and external financial challenges..

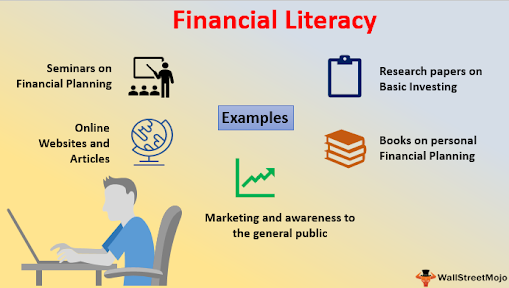

Benefits of Financial Literacy

Financial literacy focuses on the ability to manage personal finance matters efficiently, and it includes the knowledge of making appropriate decisions about personal finance, such as investing, insurance, real estate, paying for college, budgeting, retirement, and tax planning. Those who understand the subject should be able to answer several questions about purchases, such as whether an item is required, whether it is affordable, and whether it's an asset or a liability. Financial literacy education should also include organizational skills, attention to detail, consumer rights, technology, and global economics

%20(3).jpeg)

how to begin?

(1). Identify your starting point

If you don't know where you are financially, it can be challenging to plan for where you want to be next year, five years from now or decades down the road in retirement. That's why it is important to identify your starting point.

Calculating your net worth is the best way to gauge both your current financial health and your progress over time. Net worth is the amount by which assets exceed liabilities and can provide a wake-up call if you are off track or confirmation that you are doing well.

(2). Set your priorities

Creating a list of needs and wants can help you set financial priorities. Needs are things you must have in order to survive: food, shelter, clothing, healthcare and transportation. Wants, on the other hand, are things you would like to have, but aren't necessary for survival.

Knowing the difference between the two, and being mindful of the distinction when making spending choices, goes a long way when it comes to your financial wellness. You'll need to rank your needs as well as your wants in order to clearly define where your money should go first. This not only applies to your current expenses, but to your goals—which can also fall into the categories of wants and needs.

(3). Document Your Spending

Most people could tell you how much money they make in a year. Fewer could state how much money they spend, however, and fewer still could explain how and where they spend it. One of the best ways to figure out your cash flow what comes in and what goes out is to create a budget, or a personal spending plan.

A budget forces you to put down on paper all of your income and expenses, and this can be an indispensable tool for helping you meet financial obligations now and in the future. As an added bonus, a budget can be a real eye-opener when it comes to spending choices. Many people are surprised to find out just how much money they are spending on superfluous goods and services.

(4) . Pay Down Your Debt

Most people have debt mortgage and auto loans, credit cards, medical bills, student loans, and the like. What makes living with debt so costly is not just the interest and fees, but because it can prevent people from ever “getting ahead” with their financial goals. It can also be an emotional drain on individuals and families.

While the best strategy is to avoid getting into debt to begin with by making practical spending choices and living within one’s means, there are strategies to pay down and get out from under the debt people have already acquired.

(5) . Secure your Financial Future

Due to dire financial circumstances, many people adopt “I’ll never retire” as a retirement plan. This approach has several major flaws.

Firstly, you can’t always control when you retire. You could lose the job that you’ve held for decades, suffer an illness or injury, or be forced to care for a loved one any of which could lead to an unplanned retirement. Secondly, saying you won't retire is often an excuse for those who don’t want to spend the time and energy to develop a real plan, or who simply don’t know how.

Learning more about your retirement options is an essential part of securing your financial future. Even if you can’t save much, every bit helps. Once you've developed a plan, you could end up making better spending choices now that you have a goal in mind.

Financial Health

Financial health is a term used to describe the state of one's personal monetary affairs. There are many dimensions to financial health, including the amount of savings you have, how much you’re putting away for retirement, and how much of your income you are spending on fixed or non-discretionary expenses

.png)

Understanding Financial Health

Financial experts have devised rough guidelines for each indicator of financial health, but each person's situation is different. For this reason, it is worthwhile to spend time developing your own financial plan to ensure that you are on track to reach your goals and that you’re not putting yourself at undue financial risk if the unexpected occurs.

How Financial Health Is Determined

An individual’s financial health can be measured in a number of ways. A person’s savings and overall net worth represent the monetary resources at their disposal for current or future use. These can be affected by debt, such as credit cards, mortgages, and auto and student loans. Financial health is not a static figure. It changes based on an individual’s liquidity and assets, as well as the fluctuation of the price of goods and services.

.png)

Improve Your Financial Health

To improve your financial health you must first take a hard, realistic look at where you’re currently at. Calculate your net worth and figure out where you stand. This includes taking everything you own, such as retirement accounts, vehicles, and other assets and subtracting any and all debts.

.png)

set up a Budget

After you are done improving your financial health Then you need to create a budget. With your budget, it’s not enough just to plan for where you’ll be spending, but it’s also important to take a hard and close look at where you already spend. Are there areas where you could cut back? Recurring subscriptions that you don’t really need such as cable? It’s fortuitous to understand what your “needs” are versus what your “wants” are.

Emergency Fund

Building an emergency fund can materially boost your financial health. The fund is meant to be money that is saved and readily available for emergencies, such as car repairs or job loss. The goal should be to have three to six months’ worth of living expenses in your energy fund.

Debt

Pay down your debt. Use either the avalanche or snowball methods. The avalanche method suggests paying as much as possible toward the highest interest debt while paying the minimum on all others. The snowball, meanwhile, suggests taking the smallest debt balance first and then work your way up to the largest debt.

%20(4).jpeg)

{kind=link}

%20(2).jpeg){kind=link}

%20(3).jpeg){kind=link}

.png){kind=link}

.png){kind=link}

.png){kind=link}

%20(4).jpeg){kind=link}

Business Financial Health

The financial health of businesses can be gauged by comparable factors to assess the viability of a company as a going concern. For instance, if a company has revenue coming in and cash in the bank, yet is spending its resources on new investments in production equipment, office space, new hires, and other business services, it may raise questions about the long-term financial health and survivability of the company.

If more money is spent that does not contribute to the overall stability and potential growth of the business, it can lead to a decline that makes it difficult to pay regular expenses such as utilities and employee salaries. This may force businesses to freeze or cut salaries in order to give the company the ability to continue operations.

I know it's a Lengthy article but its really helpful. Spare few mintues and do read this carefully and it will help you learn more about finance. Also really good if you are running a business. It is more likely "Wealth management" also i am a Commerce student so i learnt most of it during my school and after this in graduation. I Hope you guys like this article.

PS- It is a "Steem Only" post

20% of post rewards goes to @ph-fund to support Project HOPE

If you wish to join the project hope community then head over to LINK

for further information.

5 Easy Ways to Check Your Personal Financial Health

As a follower of @followforupvotes this post has been randomly selected and upvoted! Enjoy your upvote and have a great day!

@rishabh99946 first of all very nice article , every one should have knowledge of how to maintain their finance.

Thank you, Yes @adityajainxds it's necessary because in today's competition is on extreme level everywhere in every field you must play Wise and smart :)

Financial education is as important as having a very good financial health. It is a different thing to be financially educated and it is a different thing to be financially healthy.

Yes, but don't you think there should be proper balance of both?

This post has been rewarded by the Steem Community Curation Project. #communitycuration06

Thank you @steemcurator06