Meta Platforms: This Reasonably Valued Tech Growth Stock Could Explode in 2024

Meta Platforms (META) is looking good from a technical standpoint as the stock remains in a strong uptrend. The uptrend can continue in 2024 as advertising spending growth is expected to accelerate. Meta's valuation remains reasonable which should allow the stock to outperform as earnings grow at an above-average pace. Meta also has long-term future potential growth from its artificial intelligence offerings.

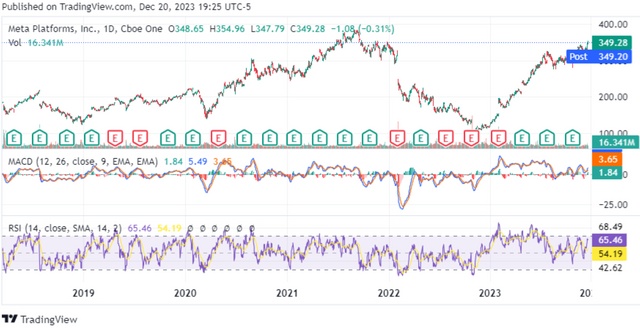

Meta Platforms Technical Outlook

Meta Platforms Daily Chart w/ MACD & RSI (tradingview.com)

We can see that Meta's stock had a strong uptrend over the past year. The stock almost fully recovered to the 2021 high of about $384. The MACD indicator recently made a bullish crossover on the daily chart with a reading above the zero line at 3.65. The RSI indicator is also bullish as it remains above 50 at 65.46. Given the positive momentum, I will watch for the stock to maintain its rise above the previous resistance level of about $348 to $349. If the price can turn this level into support, it could head back to the all-time high in the $380s. This price increase could be driven by Meta's strong expected double-digit earnings growth.

Closer Look at Meta's Bullish Change in Trend

Meta Platforms Daily Chart w/ MACD (tradingview.com)

The daily chart above shows the stock price at the top with a clearer view of the price candle sticks at the top and the MACD indicator at the bottom. The green candlesticks have been dominating in December as the stock had more strong rallying days than down days. We can also see the blue MACD line just beginning to cross above the red signal line with the histogram changing back to green. This shows that a new uptrend is underway.

The overall technical set-up shows that the stock has more room to run higher and there are fundamental catalysts that can keep the uptrend going. However, a negative earnings report and/or negative guidance could cause the trend to change to bearish. Meta reports earnings on 1/30/24.

Meta's Growth Catalysts

Expected Increases in Ad Growth

Increases in Ad spending growth can be the catalyst to drive Meta and Alphabet's stock higher. Analysts from Morgan Stanley expect advertising spending growth to accelerate in 2024. This is expected to be led by digital ad spending which Meta offers to businesses of all sizes. The forecast calls for 10% ad spending growth in the United States in 2024. Online advertising is expected to grow at a stronger pace of 12.5% in 2024 as compared to 8% in 2023.

Meta has been trending well with ad revenue growth in 2023. For the first nine months of 2023, Meta increased ad revenue by about 13% to over $93 billion as compared to the first nine months in 2022. Meta can build on this positive trend in 2024 with the expected ad industry growth.

The expected increase in ad spending growth could provide Meta with a positive tailwind for revenue and earnings growth in 2024. Meta is expected to grow revenue at about 13% and earnings at about 21% in 2024. Competitor, Alphabet (GOOG) (GOOGL) is expected to grow revenue at a lower pace of 11% and earnings at 16% in 2024.

Meta and Alphabet both have strong double-digit expected top and bottom line growth and are likely to perform well in 2024. Both companies are likely to benefit from the expected increase in ad spending. However, Meta has the advantage with higher expected growth rates.

Artificial Intelligence as a Potential Catalyst

Meta has another potential positive growth catalyst for the future in Artificial Intelligence [AI]. One part of Meta's AI offerings includes AI translation models. Meta's model has nearly 100 languages that can enable natural communication across different languages. This includes speech and text translations. This can be used to help global businesses to communicate more effectively by breaking down language barriers.

Another part of Meta's AI involves using augmented and mixed reality for more enhanced instructional 'how-to' tutorials. This can help individuals learn new skills with the help of AI. This could also be used by businesses to help train employees on certain tasks in a more efficient way.

Llama 2 is another aspect of Meta's AI offerings. Llama 2 is Meta's open source large language model for generative AI. This is a competitor to other large language models such as GPT-3 and PaLM 2. Llama 2 is currently free for research and commercial use. However, Meta could consider offering a subscription tier in the future for new revenue generation.

The global market for generative AI is expected to grow at about 24% to reach $207 billion by 2030. This market is estimated to be worth $44.89 billion in 2023. Meta has the potential to take advantage of this growth by monetizing its AI offerings.

Meta's Valuation Advantage

I like to use the PEG ratio when measuring the valuation of high growth companies like Meta. The PEG factors in multiple years of expected earnings growth which provides a long-term picture of the valuation.

Meta is currently trading with a PEG ratio of 1.2 based on its expected annual EPS growth of about 20% over the next 3 to 5 years. This is lower than the sector median PEG of 1.53 and lower than Alphabet's PEG of 1.42. Alphabet's PEG is based on its expected annual EPS growth of about 17% for the next 3 to 5 years.

Overall, both companies have more room for stock growth as the PEG ratio is reasonable for both at a level below two. However, Meta has the valuation advantage with a lower PEG, giving the stock more room for upside runway.

Risks for Meta Platforms

Competition is the biggest risk for Meta Platforms in my opinion. Advertisers could find Alphabet's advertising offerings to be more attractive or effective (ie. Google search & Youtube). Advertisers could also shift to other competitors if they are found to be more effective in converting ads into sales.

Another risk for Meta is that there is no guarantee that its AI efforts will be successfully monetized. Offerings from other companies could turn out to be the go-to AI solutions. So, Meta will have to make its AI offerings resonate with users so that it remains attractive as a go-to solution.

Final Thoughts on Meta's Outlook

Meta should benefit from the expected increase in ad spending growth in 2024. The company also has longer-term growth potential if it can successfully monetize its AI offerings. Meta has positive technical momentum, strong above-average growth and a reasonable valuation as measured by the PEG ratio. This can enable the stock to outperform the S&P 500 (SPY) in 2024 and beyond.

I didn't intend to publish this in the Newcomer's Community. It should be place in the #stocks thread.