Which cryptocard to choose (VISA / MasterCard)?

So about a year ago I had a problem. Being abroad, I was in urgent need to send money to a friend. There was an issue of paying for housing and an ordinary bank transfer wasn’t an option. Firstly, it was Thursday and the money would only come on Monday (it takes up to 3 working days for an international bank transfer), and secondly, I had to pay a considerable commission. And don’t forget about money loss on currency exchange. In total: 4 days and a loss of 5–10% of the value. Fortunately, we were used to cryptocurrencies and it took us about 1 hour and 2% of the commissions to solve that problem — I sent him bitcoins, he cashed them through localbitcoins. Unconditional benefit of cryptocurrency and a huge drawback of the banking system.

A lot of time passed after that situation, my cryptowallet balance increased, there was a desire to spend part of the cryptocurrency. It is very pleasant to see how capital is being multiplied, however, sometimes it is just necessary to treat yourself, otherwise positive emotions fade away. Buying a cup of coffee for bitcoins seems to me as a terrible waste of money, since the commission for such micropayments will be comparable to the price, if it does not exceed it. Buying something more expensive makes sense.

Cashing out Bitcoins through localbitcoins is quite simple, but there are a number of inconveniences. To begin with, the seller you prefer to trade with is not always online. Secondly, you have to justify the money that come to your card (in Europe the receipt of more than € 2,500 will be checked by the bank). In addition, I do not like banks. A number of times banks caused inconvenience or even serious problems to me. Sometimes, it was a fault of an unskilled employee, more often — the banking system’s fault. 5 times I paid fines for overdraft, which I disabled, several times I have not received SMS to access online banking, as I was abroad, dozens of times I found withdrawals of small amounts on behalf of the bank, the essence of which nobody could explain. I am sure that you yourself will remember about a dozen other similar stories that happened to you or your friends. In the end, I was tired of proving anything to banks, and decided to find a way to keep only small amount of money necessary for paying utility bills or gasoline on my bank card, while the rest is stored in a cryptocurrency.

The market of prepaid cards that can be replenished with Bitcoin (or other cryptocurrencies) is quite diverse, so I decided to thoroughly understand available options. The first filter was the card issuer. We all know the most popular of them — Visa, Master Card, American Express. At least half of the options immediately failed the test, because for a long period of existence in the market, they have not received the so-called accreditation from these issuers. Well, and who wants to use the card, which is almost never accepted? As a result, 10 cards went to the final selection, which looked quite serious. I’m going to tell you about them now.

AdvCash

AdvCash is a company of the international team that quickly and thoroughly got on its feet in the online banking niche in Europe, Asia and the USA. The process of registering an account is quite simple, and it is the same for all the cards below, so I will do it only once.

Classic login / password -> email confirmation (as usual, come up with a complex password, no dates of birth, namesurnames, pet names, etc.)

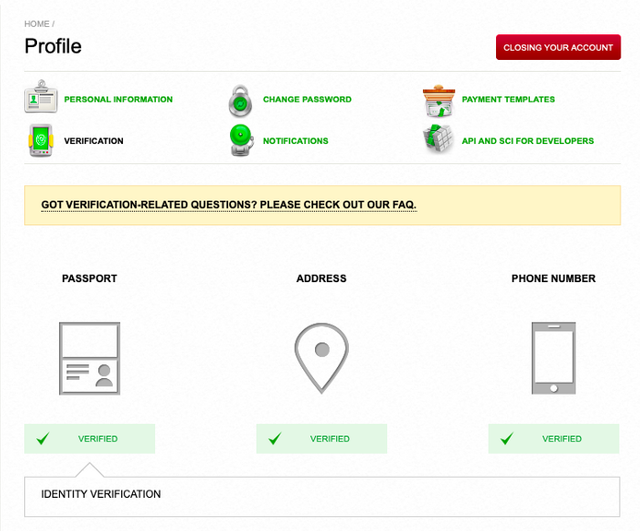

Verification. Passport — Address — Phone number. Self-explanatory steps, you will see the instructions on the screen. The support service is quick and attentive, and within a day your account will be verified.

Security. Do not postpone the security of your wallet. You have a choice of 6 options, choose any to your taste.

Intellectual Identification — IP address binding— SMS authorization — Payment Password — Code Card — 2FA

I will note only that SMS authorization has repeatedly shown itself to be a bad choice, since a good hacker can easily access your phone, and therefore also an SMS. I prefer the token, AdvCash uses analogue of Google Authenticator — Protectimus application. It is practically impossible to hack it (possible, of course, but other security measures will not stop the one who is able to do it).

Congrats! The registration and verification is completed. As I said, the process is identical for other “competitors”, with the exception, perhaps, of the site design and the number of security options.

By default, you will be able to set up accounts in dollars or euros.

As soon as you get your documents verified, order a card. For quite a long time (more than a year), the status of cryptocurrency was unclear in many countries, which has affected the attitude of Visa and MasterCard to the projects under consideration. Therefore, almost all cards have been recalled, and only from May 14, 2019 they are they gradually entering the market again. June 19, 2019 AdvCash officially announced that they are starting beta testing of cards for residents of Russia and the EU. Visa has become a new issuer! For those who already had a card — re-issue is free. I got my card during the beta-test period.

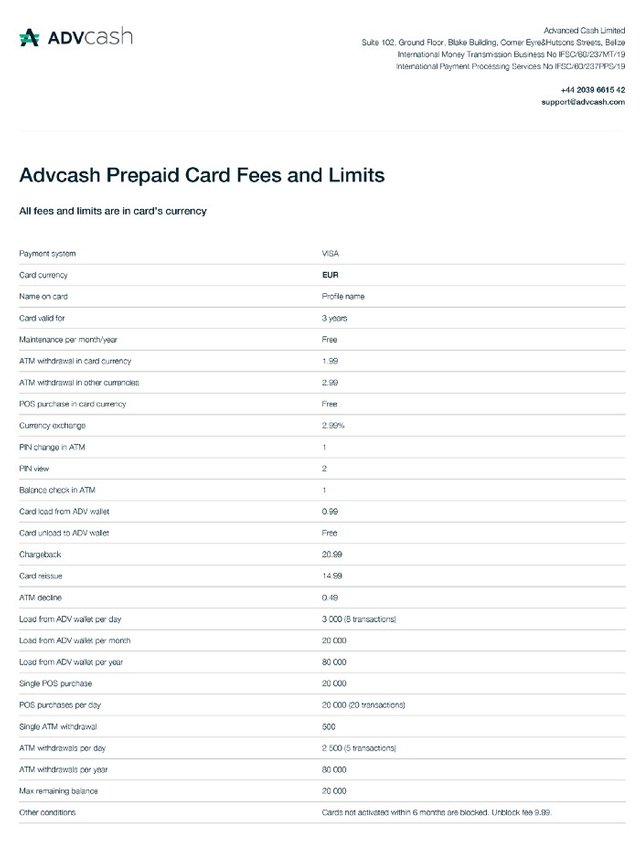

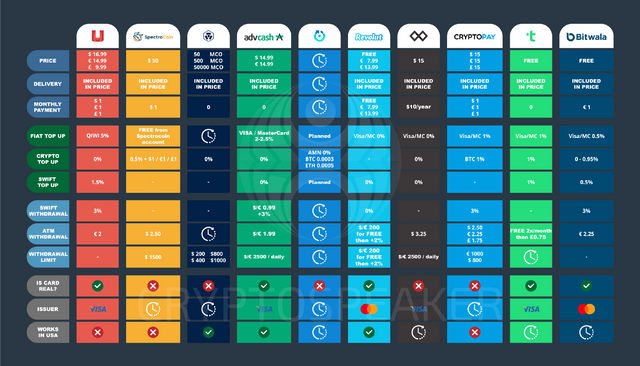

I know for sure that there will be two types of cards — Standard and Pro. Standard card is $/€ 7.99 if you order it in the first days after you set up a new account and $/€ 14.99 after few weeks. Additional cards (up to 5) will cost $/€ 14.99 each. The validity of the card is 3 years. There is no (!) monthly payment for services. Commissions when withdrawing funds from an ATM is $/€ 1.99. The daily withdrawal limit is $/€ 2500. To understand how to work with advcash, you need to consider your account as a bank account and a card. When replenishing the balance (cryptocurrency or fiat) funds are deposited into the account. After that it is necessary to transfer them from the account to the card. It costs $/€ 0.99. So, if you want to withdraw $2 from the exchange, a half will go to the commission. The daily limit for spending from the Standard Card is $/€ 20000. There is no information on how Pro version would be different to a Standard one, but I will update this article as soon as they release full updates.

I don’t think I should explain that during registration it is necessary to indicate the real data, without fictitious names, addresses, etc. You are applying for a bank card after all…

To pay for your card you need to deposit money into the account. There are plenty of options to do — with your credit card (Visa, MC, Amex, JCB, Diners Club), bank transfer (SWIFT, SEPA), electronic money (Payeer, Bitcoin, Perfect Money, Payza, Epay).

How long does it take for a card to be delivered? Officially 3–4 weeks. I got my in just 1 week (free delivery). Upon arrival, activate the card through the website, you will see the PIN code in the process.

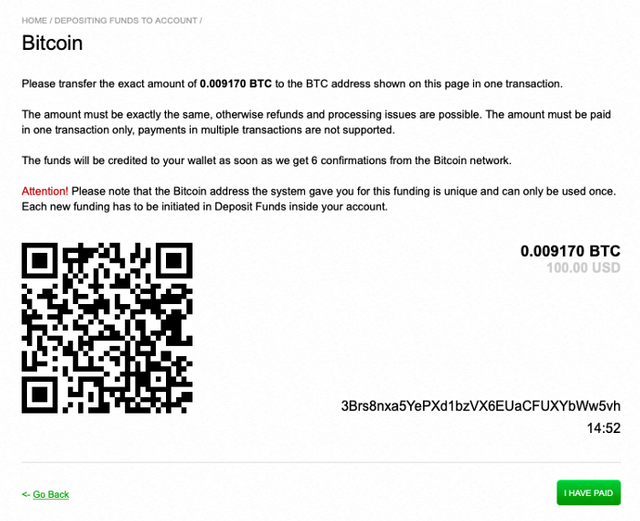

Well, and to the main thing — how to replenish cryptocurrency. Using the example of Bitcoin — we choose for what amount we want to replenish our account (it is important to immediately select the account currency). Then a temporary wallet will be created (15 minutes), its address and the exact amount in BTC will appear. IMPORTANT: when transferring from a wallet or exchange, make sure that the amount you will recieve is exact to what you are asked for, initially add the service commission to the sent amount, otherwise the transfer will take much longer and/or will not happen at all, and the money will be returned. At the end of the payment, click “I have paid” and wait for transfer. The waiting time depends on the speed of receiving 6 confirmations (on average from 15 minutes to an hour).

What is nice, the bitcoin rate on advcash is always close to real (unlike, for example, TenX, where the rate is different by $ 500–1,000). If you want to get $ 100 to advcash, you will eventually send ~ 102–107. Another little tip. For each transfer from account to card, advcash will charge you $ 0.99 or euro, depending on the wallet. If you want to buy something exactly for $ 100, then recharge your account balance by $ 101.

A distinctive feature of the AdvCash project is constant discounts on commissions. Every month, sometimes it happens more often, the official AdvCash social networks publish information about a discount in commission for some ways of replenishment. The most popular methods of replenishment are cheaper, such as transfer from another Visa / MC card, QIWI, etc. In parallel with discounts, less popular methods of replenishment are becoming more expensive. Keep your eyes open.

AdvCash team has long promised to start developing an official mobile application, but so far there are no results. They’ve told me that the application was being made, but they would not disclose any release dates in order to avoid community anger in case of unplanned delays.

UQUID

The company is registered in England, Coventry. Although, not from the first attempt, but they were able to agree with Visa on the issue of cards. The main distinguishing feature from most of other cards is the possibility of issuing an altcoin card, which can be replenished with 89 altcoins.

It costs $ 4 more than advcash, plus, there is a monthly service fee of $ 1.

It is rather expensive to replenish the balance with a bank transfer (1.5%) or with QIWI (5%). However, it is argued that no interest is charged for the replenishment by cryptocurrencies, only the miners commission.

Card delivery is free (of course, because everything is already included in the price), delivery within 2–3 business days in Europe.

Of the known drawbacks — the support service does not always promptly cope with requests. Does not work in the United States.

SpectroCoin

SpectroCoin is an English-Lithuanian project that was also negotiated with Visa.

The disadvantages of this card are the terrible price of a $ 50 for a plastic card. Monthly payment $1/€1/£1. When you replenish with Bitcoin, you will pay 0.5% + $1/€1/£1 commission. You will also have the highest cash withdrawal fees at ATMs — $3.75/€2.50/£2.25.

There is no need to verify your documents for ordering or using a plastic card, however limits will be set. After verification, any limits on replenishment, withdrawal or purchase will be removed. You can order up to 6 cards, 2 for each currency — GBP, USD and EUR, so that you have one card and a spare at home in case of loss, or for your relative. Finally, you can use this card to verify your PayPal account. Does not work in the United States.

Monaco

Monaco is an interesting project with its own cryptocurrency MCO. At the moment there is no real product (plastic cards), but you can get in line to receive them. There are several “levels” of cards for holders of MCO tokens — 50MCO, 500MCO and 50000MCO, each of which offers its own advantages. It promises absolutely commission-free servicing, replenishment and cashing, however, it is already known that there will be daily limits for withdrawals at ATMs of $200, $400, $800 and $1000.

There is not enough initial data, however, nothing prevents you from registering in the program for receiving a free card through the Monaco mobile app. If the developers roll out a really cool product, then you will already have it on hand, and you can use it without waiting.

In fact, Monaco cards are available for customers from USA. EU clients have to wait a bit longer.

Revolut

One of the most successful fintech startups, the Amazon of banking industry, a unicorn in the world of finance … That’s how Revolut is described by many publications and such honours are quite deserved. Revolut quickly launched into the financial industry due to the focus on the regular customer without millions at the Seychelles. They have all the features of ordinary banks, plus a lot of their own. It allows you to buy a cryptocurrency in three clicks, without any third-party wallets. It’s incredibly convenient when traveling. I think enough dithyramb, I already did a full review of their service, read it — be surprised.

https://medium.com/@cryptospeaker/revolution-that-does-not-require-sacrifice-16012446d03d

Amon

Amon is a project that causes ambivalent feelings. On the one hand, there is too little information about him, so little that in the comparative table Amon is the wild card. On the other hand, what is already known is impressive.

Perhaps, I will follow that way of the known-unknown:

What is yet unknown:

Price, delivery time and monthly payment. It has not yet been announced whether it will be possible to withdraw money from the card via SWIFT, what are the cash withdrawal limits and ATM comissions.

Whats is planned:

Most likely, it will be possible to replenish the card with a transfer from another card, SWIFT and other services (QIWI, PayPal).

What is know for sure:

There will be two types of cards — regular and gold. Gold card holders will have a separate support service, commission-free service, cashback in AMN tokens with each transaction, AI support.

In a nutshell — Amon is a project with its own AMN token, which is similar to BNB on Binance. With its help, it will be possible to trade cryptocurrencies inside the wallet with minimal commissions (or without them at all). The wallet will allow you to store not just the top 5, but will become a full-fledged multi-currency altcoin wallet, like Jaxx. Any cryptocurrency can be spent in a store or cafe with the built-in exchanger. In addition, AI will automatically calculate the most favorable rate at the time of purchase and offer the user to spend exactly that token.

As I said, there is not enough information, but on paper this is what we are all waiting for — a multi-currency wallet that works like our regular bank card, supports many altcoins, plus a cashback to boot.

Problems:

Support. Requests are answered for a long time, too long for an online bank. Perhaps the situation will improve in the future.

TokenCard

Another British player. The company entered the market with perfect timing and avoided problems with the issuer. Only a month and a half and beta testing of their applications for Android and IOS was opened, and a couple of weeks later the release of the first cards began.

Of the features — this is a card for those who are not the first day in the subject of cryptocurrency. To begin with, your funds are stored on a smart contract. The wallet supports most popular ERC-20 tokens and Ethereum. In order to use the wallet, it is also necessary to replenish Gas Tank, from which funds will be used to account for commissions. The user gets full control over his wallet and with such force comes a serious responsibility. You will need to select your daily spending limit and Gas Tank replenishment limit. Once and for all! This information is recorded in a smart contract! Separately, you can specify 5 Ethereum addresses to which you can send any amount to bypass the limits. Changing them in the future will also be impossible!

Problems:

This is my personal, subjective opinion, but users are given full control over their finances and smart contract. Sadly, but 80% of users will face the problem of daily limits. Users are not ready to assume such responsibility, they will need help. And this leads us to the second issue.

I do take into account that now only the alpha period of the cards and application will change a lot, but the support service is still far from ideal. To answer, the team takes 2 business days. In fact, it turns out more, much more. My first card, for example, was sent to the house, and not to the apartment. The support service said that the issuer “forgot” to indicate in the letter my floor and apartment, but I have little faith in this. Having offered a reissue of the card with the control of the correctness of the address, the support was again dissolved in the air. To my question “Should I wait for the reissued card?” they did not respond for several days. After a week or so my reissued card has arrived with a personal letter from CEOs and TokenCard Team, which was really heartwarming.

A very nice addition that allows you to see in the project not just a distant bank with inaccessible directors, but an interesting startup in which they understand the importance of being close to the client.

In addition, there were nice additions. First, all the participants of the alpha testing of the mobile application were sent 50TKN, which, depending on the prices on the stock exchange, varies between $25-$40. Moreover, the first 1000 people who downloaded the application, ordered the card and activated it received 15DAI. In total — about $60 just for downloading the application and ordering a free card. Very nice!

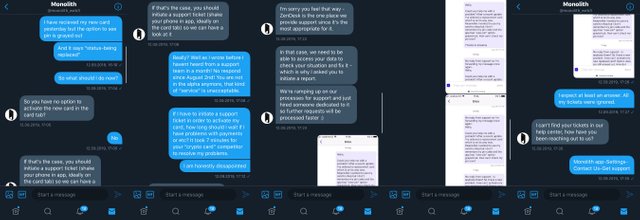

UPD(22.09.19): Recently, TokenCard has gone through the rebrending and now it’s called Monolith. All clients have been suggested to reorder new card, which has got new design. Thats where the problems come. I might be just unlucky but it takes ages for my card to be delivered. However, my friend got her new card quite quickly, yet she still can’t use it. Once you launch re-ordering process your app says that the card status is changed to “Active-Being replaced”. Also your PIN won’t be available until your new card arrives. And your recent card is not accepted in shops anymore… Yes, you heard it right. If you forget your PIN you won’t be able to see it, but it doesn’t matter as your card is useless now and your money will be frozen WITHOUT ANY NOTICE! Support team just sucks, they “don’t see my message” for over 14 days and when I contact them on Twitter they say that there are no requests from me. Guess what happens after I send them screenshots of my support tickets? They never reply.

After the third attempt support team asked for the last 4 digits of the old and new card in order to activate the new card. After all these inconveniences we found out that it’s a bug that Monolith app doesn’t have an option to activate new card. It is not a unique bug, I see the same problem on my app as well. Once my card arrives I’m gonna have to go through that process once again… As you might guess, nothing happened after we sent them the requested info. 10/10 Monolith, 10/10. I have made my decision about Token/Monolith, it’s a no-no. Once you leave Alpha-version your service has to be spot on, but Monolith seems to be understaffed and unprofessional, concentrating on the Rick&Morty style rebrending more than on improving customer service.

Each of the cards reviewed has its pros and cons, so I couldn’t choose the best one. Is there my personal interest in promoting one of these projects? Well, you decide:

Two years ago, I set up an AdvCash account and couldn’t get enough of it until they had recalled the cards. A few months ago I’ve recieved a new one. I have been using the Revolut card for two years and advise it to many friends. I participated in the Amon Private ICO and I am waiting for my Golden Card. I have been using the Token card for a month now. I’m queuing up for Monaco cards. Why so many? I do not keep all the eggs in one basket. I like it when there are a lot of cards in the wallet. I do not know which project will be the best, but I believe in the prospects of many. Choose which option you like.

Well, finally, for those who read it till the end and found it useful. I started this article in December 2017. It’s time to update it and when the new cards enter the market I’ll do it again. This is the most detailed analysis of such a number of cryptocards and I hope it will help you decide. If you have any questions — contact me on Telegram, I will answer your questions with pleasure. Do you think the article is useful? You can share it with others and order cards with these links:

AdvCash - http://wallet.advcash.com/referral/f2356ba0-b9cd-4203-af43-d47655a1a7f9 — A small percentage of the commissions that AdvCash would receive will drop to me

Revolut - https://revolut.com/r/glebdqrz — I’m not even sure if I get something. But you can get a free card or €4.