DeFi's next stop: stable and magnified returns in fixed_finance fixed interest rate markets

DeFi ushered in explosive growth in 2020, and many financial sectors were born. Today we will review and analyze, speculate on the huge market that may emerge in the future: fixed interest rate market, and introduce an important project in this field-fixed.finance.

DeFi's current form and different sectors

This is the TVL (total lock-up volume) trend chart of DeFi over the past year calculated by DeBank. It can be seen that the overall situation has begun to rise since June 2020. In December 2020 and early 2021, the rising slope of TVL increased sharply. This is closely related to the prosperity of DeFi and the rising prices of mainstream assets such as ETH and BTC. The 62 billion US dollars in the picture data includes DeFi endogenous assets, and the net locked assets are 46.7 billion US dollars (data on March 9, 2021). The growth of dozens of times in the past year is just the beginning of DeFi. The current overall scale of DeFi is only equivalent to a good fund in traditional finance, and it is still in its infancy. With the continuous improvement of the DeFi ecosystem, there is still great room for growth in the future.

And what are the sectors in the current DeFi ecosystem?

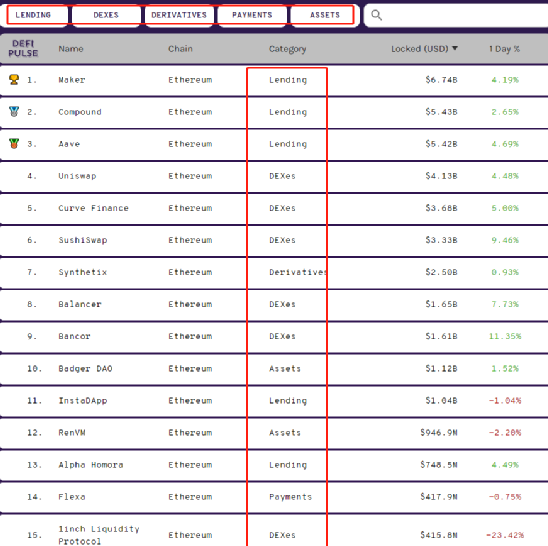

The picture above is from DeFipulse

We have selected the top 15 TVL of the ETH mainnet DeFi project, which can be roughly divided into: 1/3 is lending (borrowing), 1/3 is DEX (decentralized exchange), and the remaining 1/3 is asset management Categories, derivatives, payments, etc.

All of the top three are borrowing. Especially the recent rise of AAVE is the most obvious. AAVE has made two innovations: credit entrustment and lightning loan. Compound and Maker do not have similar functions. Although these two functions are not so useful for most users, lightning loans belong to technical geeks, and credit entrustment belongs to acquaintance circles and B-end users. But this also proves a truth: some small innovations, even if they are not so useful for most people, are enough to make a project in the DeFi field stand out.

Daily understanding of fixed interest rate markets

Let's think about a question: What is one of the largest sectors of the financial market? Are there any outstanding DeFi benchmarking projects in this sector?

There is no need for in-depth financial knowledge here. Our understanding of finance should start from the daily routine-this is also the classic thesis of the famous economist Professor Zhang Wuchang. We thought through this thinking and found that for ordinary people, the most commonly used and most widely used scenario is bank financing, especially time deposits. Because the income of fixed deposits is stable and the interest rate is high.

However, through the above data, we will find that the DeFi market has no products with excellent projects, high TVL rankings, and stable income with fixed interest rates.

Nowadays, APY (annualized rate of return) is 10% today (some LP liquidity mining can exceed 3000% in a short period of time), and tomorrow will fluctuate sharply, and user income will be like a mirrored picture. For users with low risk appetite, it is impossible to get a lot of money into such a pool full of great uncertainty.

"According to ICMA data, as of August 2020, the overall size of the global fixed income market is approximately US$128.3 trillion." Even if this data is reduced by 100 times or 1000 times, the market is huge for the fixed income sector of DeFi. What we want to explain below is a fixed income project with great potential and importance in the DeFi field: fixed.finance.

How does fixed.finance realize fixed income?

Let’s first take a look at the project introduction: “After users deposit in the Fixed-Rate Protocol, these funds will enter the basic revenue platform for cooperation (such as Compound, Harvest, Curve, etc.), and these platforms provide floating annualized returns. Fixed -Rate Protocol provides a variety of mechanisms to ensure the safe payment of fixed income (rigid payment)."

The basic logic here can be simplified and understood: the fixed interest rate comes from the fixed interest rate model and the floating interest rate model.

- The fixed interest rate model uses 75% of the index average index of the basic platform as a safe fixed interest rate;

- Floating interest rates are in the form of bonds, requiring participants to judge the rise and fall of interest rates in the future. When it rises, the bond gains, and it has leverage properties, and the return will be amplified; when it falls, fixed.finance also has a mechanism to protect it, and the bond will not lose money if the interest rate falls within 25%.

Among them, platform currency mining is added to the fixed income model. The fixed interest rate can be understood as the guaranteed interest rate, and the reward of the platform currency will magnify the income on the guaranteed fixed interest rate. In the early stages of the project, the rewards of platform tokens may be very large, far exceeding the benefits of fixed interest rates.

For example, here are two users A and B:

User A wants stable returns and has a very low risk appetite. Deposit 10,000 US dollars on the platform (fixed.finance) with a fixed interest rate of 10%. After one year, the withdrawal is 11,000 US dollars, and the fixed income (profit) is 1,000 US dollars. It is stable and risk-free in the long term.

User B has a higher risk appetite and is willing to take a certain degree of risk. Buying $1,000 in bonds, if the platform APY (annualized income) rises to 20%, how much should B get at this time? 10000*20%-10000*10%=1000 U.S. dollars (the 10,000 U.S. dollars here refers to the funds of user A), then what is the APY of B? 1000/1000=100%. Interest rates fall below 10%, the same calculation method is used.

That is to say: Bond user B is equivalent to using user A’s funds as leverage. Under this mechanism, fixed income can be guaranteed to A when interest rates fall, while Type A users let go of the increase in interest rates. The proceeds go to type B users (bond users), and part of the risk is also passed on to bond users.

There is a balance between risks and benefits, and people with different risk preferences have different product choices.

Note: This article refers to stable currencies such as DAI, USDC, and USDT as US dollars for the convenience of understanding.

In addition to the balance between fixed interest rates and floating interest rates, the platform also mentioned the following points:

1. Global interest liquidity pool

The global interest liquidity pool can provide a buffer against floating. When the interest rate of the basic income platform is higher than the fixed interest rate provided to the user, the interest of the liquid pool will be larger than the interest that needs to be redeemed by the user. This part of the surplus can be used to balance the debt brought by the fall in interest rates. The global interest liquidity pool is transparent and visible on the blockchain.

2. Community Governance Fund

The establishment of the community governance foundation is to support the business development of the product and at the same time reduce the risk of redemption. 10% of the deposit income will be released to the community governance foundation, and the platform currency will also be returned to the community governance foundation. As the business grows, the base will continue to grow, which can provide a layer of protection for the increase in interest payments. Although we believe that the probability of using the community governance base to redeem interest is almost zero. The foundation of community governance is also transparent on the blockchain.

3. High-quality modern partners

After a comprehensive survey, data analysis, and security review of multiple basic revenue platforms in the situation, excellent platforms and products are selected from a professional level, and a certain structured configuration is made. This can reduce the risk at the source and guarantee the rate of return.

4. Open up the NFT channel

The assets of the Fixed-Rate Protocol and floating rate bonds all use ERC721 standard NFTs as vouchers. In this way, you can interact and connect with your own DEFI mode. Here, ERC20 can be used to split and trade the tokens on the platform. The NFT under the ERC721 agreement can be used as an exclusive mortgage certificate, and the image of these NFTs can be customized, and the NFT can interact with the upstream and downstream of the platform and more NFT communities. Add a variety of gameplay.

The above content is summarized in the official white paper information. Users participating in fixed.finance fixed-income products and floating exchange rate products will get the platform's tokens and can participate in high-yield liquid mining pools.

to sum up

The DeFi market is booming, but there is a lack of excellent fixed interest rate products to attract large funds to enter the market. Fixed.finance provides fixed income and floating income (bond users) products for different user groups. The income is stable, and there are mining, NFT, community governance DAO and other incentives, among which the fixed interest rate + platform currency reward model can help users amplify their returns in a very low-risk environment (guaranteed basic returns), which is worthy of market attention.

After this project goes online, it is likely to trigger an upsurge of early liquidity mining. Whether the project can eventually become the next hub of DeFi depends on the optimization and stability of its interest rate model, which requires a certain period of observation.

Fixed.finance official website link: https://www.fixed.finance