Steemit Crypto Academy [Beginners' Level] | Season 4 Week 1 | Homework Post for (@awesononso) | The Bid-Ask Spread

A BRIEF INTRODUCTION

1.Properly explain the Bid-Ask Spread.

Bid-Ask Spread are terms in the crypto market. As in any market, there are buyers and sellers in this market. Commodities are bought and sold, traded between each other.

These buyers and sellers have prices at which they want to buy and sell.

- The maximum price quoted to buy a commodity is called the Bid Price.

- Conversely, the lowest price the seller asks for selling a commodity is called the Ask Price.

- The difference between this highest buy and lowest sell is called The Spread.

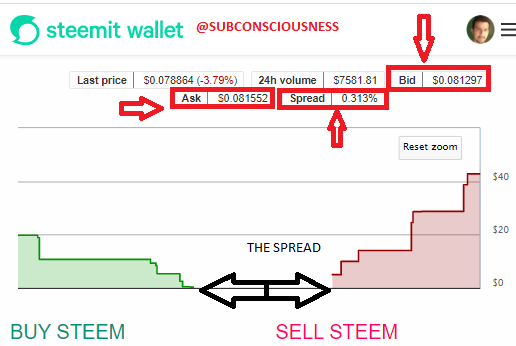

You can see the spread in the SBD/STEEM price in the market that I entered from my account.

.png)

2.Why is the Bid-Ask Spread important in a market?

This value, calculated with the " Bid-Ask Spread = Ask price - Bid price. " formula, is used to determine the liquidity level in the market. Considered in terms of demand and supply, this indicates a balance. Such a market in equilibrium is liquidity. It means that the transaction of commodities to be bought or sold will take place quickly.

If we interpret it from the sbd/steem chart I shared. The people you see in the green area are people who have Sbd and want to buy Steem. In the red area, there are people who want to buy Sbd by selling their Steems.

When the sellers do not want to sell cheap and the buyers do not want to buy expensive, such a larger spread is formed in the chart. In this case, market is illiquid and so the trading volume is also low.

3.If Crypto X has a bid price of $5 and an ask price of $5.20,

Here we will answer questions 3 and 4 using the same formulas.

To calculate the spread:

Spread = Ask price - Bid price

To calculate the spread as a percentage:

%Spread = (Spread/Ask Price) x 100

Let's move on to the question solutions, the formulas will be better understood.

The Bid Price = $5

The Ask Price = $5.20

Bid-Ask Spread = Ask price - Bid price

= $5.2 - $5 = $0.2

%Spread = (Spread/Ask price) x 100

= (0.2/5.2) x 100

= 0.03846 x 100

= 3.8461%.

4.If Crypto Y has a bid price of $8.40 and an ask price of $8.80,

The Bid Price = $8.4

The Ask Price = $8.80

Bid-Ask Spread = Ask price - Bid price

= $8.80 - $8.40 = $0.4

%Spread = (Spread/Ask price) x 100

= (0.4/8.8) x 100

= 0.04545 x 100

= 4.5454%.

5.In one statement, which of the assets above has the higher liquidity and why?

- The Spread of Crypto X =$0.2

- The Spread of Crypto Y = $0.4

The answer is Crypto X. Because Crypto X has a smaller percentage Bid-Ask spread than Crypto Y.

For this reason, Crypto X has a higher liquidity. As a small spread means the market is liquid so we expect that Crypto X's trading volume to be high as well.

6.Explain Slippage.

Slippage refers to the price shift between the price level of the order and the price level where the order is executed.

When closing the opened trade, there is no match with the ask price or bid price in illiquid markets. In summary, this situation, which is more common in commodities with high volatility and spread range, means that the trade is not realized at the desired price. It happens a lot, especially in Crypto Markets.

Market prices can change rapidly and slippage can occur during the delay between order time and completion time. This term is used in many markets and the definition is the same in all of them. But it can happen for different reasons.

To avoid financial loss, we should use limit orders instead of market orders to reduce or eliminate slippage. In this way, we do not place an order that we do not know at what price it will be executed. On the other hand, although it does not have much effect in small-volume transactions, very large losses may occur when making high-volume buying and selling transactions.

7.Explain Positive Slippage and Negative slippage with price illustrations for each.

There are two types as Positive and Negative slippage .

1- A Positive Slippage;

As the name suggests, positive slippage is a slip that results in the profit of the trader, an order is filled at a more favourable price. It means that a seller will sell at a higher price than he intended; and a buyer will purchase at a lower price than he expected.

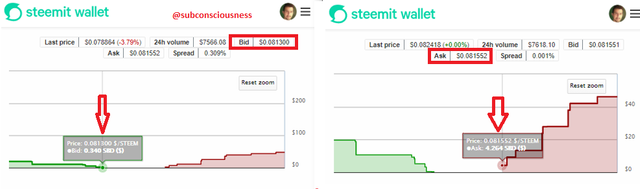

To explain with an example, let's take the SBD/STEEM price.

If a trade was place for Steem to be bought at $0.081400 and instead the trade was executed at $0.081297, the Positive slippage would be;

$0.081400 - $0.081297= $0.000103

Also, if a trade was placed for Steem to be sold at $0.081400 and instead the trade was executed at $0.081552, the Positive slippage would be;

$0.081552- $0.081400 = $0.000152

Since the Spread range that I took a snapshot of on the Steem market account was low, the value here was also low. However, when high volume transactions are made, this value will be multiplied by the amount of steem, so huge profits can be made due to slippage.

2- A Negative Slippage;

Negative slippage is a slip that a a loss occurs for fulfilled orders. The opposite of positive slippage, negative slippage is when an order is filled at a less favourable price. It is the type of slippage that takes a loss, whether when bidding or asking a commodity.This can happen in both directions.

The previous steem example may not be understood because the values are very low. So I'm going to expand the example a bit. For example, let's take the illiquid Crypto Z commodity.

For example, if a trade was placed for crypto Z to be bought at $23.9 and instead the trade was executed at $25.2, the negative slippage would be;

$25.2 - $23.9 = $1.3

Also, if a trade was placed for crypto Z to be sold at $27.6 and instead the trade was executed at $26.6 the negative slippage would be;

$27.6 - $26.6 = $0.2.

If the bid and ask above had been done sequentially and the orders had been taken out as planned.

$27.6 - $23.9 = $3.7 profit would be made.

but since there is slippage in both processes

$26.6 - $25.2 = $1.4 profit was made.

In total, profit was made again, but our profit rate was low.

it is best not to trade too much with illiquid and low volume commodities.

Thus, we have come to the end of our homework by answering all the questions. Thanks in advance for the review, professor.

Cc:

@awesononso

Thanks for your visit.

🙋♂👇Stay Tuned for my Next Post & Stay Well...🙏

Hello @subconsciousness,

Thank you for taking interest in this class. Your grades are as follows:

Feedback and Suggestions

You have clearly understood this topic but there are some explanations that needed to be clearer.

There are also a couple of points still missing.

Thanks again as we anticipate your participation in the next class.

Thanks for review professor..

Reminder: I am sorry to say this but maybe you have forgotten to vote for this post @steemcurator02

Best regards.