The Fed's "last rate hike" is the end of the short? Bank of America: history tells you not to bet

The previous experience was to "buy at the last rate hike", while the strategy in an era of hyperinflation is to "sell at the last rate hike".

The market has been suffering from Fed rate hikes for a long time, but if the Fed does turn, will the market get the long-awaited surge? In terms of historical truth, the opposite may be true.

Bank of America's team of star strategy analysts believe that although investors have been impatient with the Fed's rate hike cycle into the end, they can't wait to rush into the stock market to make a big profit, but history shows that investors should remain cautious in the case of persistently high inflation.

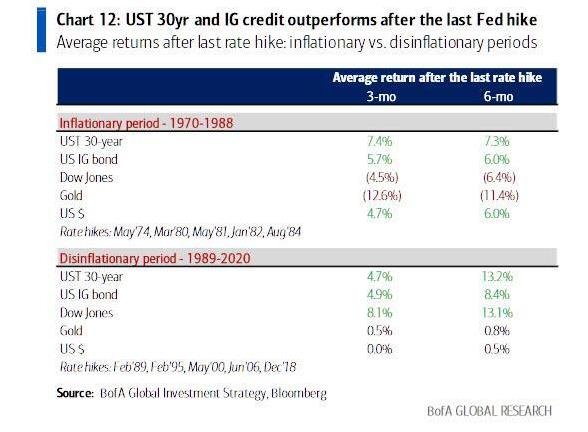

An analysis by Michael Hartnett (Michael Hartnett) shows that in the past 30 years of the journey to fight inflation, once the Fed stopped raising interest rates, the stock market usually outperformed, but in the 1970s and 1980s during the period of high inflation, the Fed raised interest rates after the last time, the stock market slumped.

In short, the previous experience was to "buy at the last rate hike", while the strategy in the hyperinflationary era was to "sell at the last rate hike". Hartnett summarizes the asset returns 3 and 6 months after the "last rate hike" in the 10 rate hike cycles of the last 50 years.

Bank of America analysts have concluded that once the "last rate hike" comes, the buying strategy should be

Buy Treasuries: Returns on Treasuries have been positive in 9 of the last 10 "last rate hikes".

Buy credit bonds: investment grade bonds have returned positive returns in 9 of the last 10 "last rate hikes".

Sell equities during inflationary periods, as the stock market fell after the "last rate hike" in the 1970s and 1980s, as punitive interest rate levels would send the economy into recession.

Buying stocks during non-inflationary periods, buying stocks after the "last rate hike" has been the right choice during non-inflationary periods for the last three decades; the central question here is whether the inflation of the last two years was a long-term or one-time event.

Buying dollars and selling gold was the right strategy in the inflationary period of the 1970s and 1980s, but not in the non-inflationary period of the last 30 years.

So, the next crucial question is when will the last Fed rate hike occur in the current rate hike cycle?

The answer will likely depend on when the U.S. recession begins. Hartnett has two scenarios, the bearish scenario is that it may occur in 10-12 weeks, that is, the Fed's last rate hike may be in March 2023. And the more optimistic scenario is that the U.S. recession will not start until the second half of next year.

In fact, not only the Bank of America, Strategas Securities' chief investment strategist Trennert (Jason Trennert) has long warned that investors betting on the Fed's shift to a dovish stance should reconsider their positions.

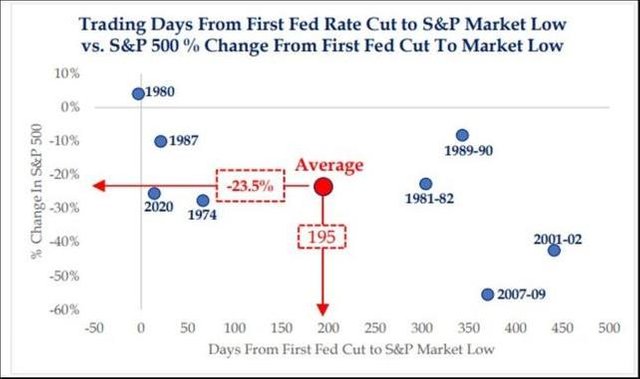

After studying monetary cycles and stock market performance since the 1970s, his team found that a real shift to accommodative monetary policy often signals pain for stock market bulls.

The firm's research showed that in previous easing cycles, the S&P 500 fell after the first rate cut, with only one exception. On average, the S&P fell 24% before hitting bottom.

Trennaert writes.

In many cases, the market has pinned its hopes for a stock price rebound on a turn in the Federal Reserve's monetary policy. However, history suggests that investors should be wary of such thinking.

Rich Weiss, chief analyst of multi-asset strategy at American Century Investments (ACI), a leading global asset management firm, says "short-sighted" investors who focus on whether the Fed is hawkish or dovish to choose when to enter the market often overlook one fact.

Investors are obsessed with the Fed's interest rate policy so they ignore the eventual outcome - the reality of a recession will squelch any rally in the stock market.

While investors cheer the Fed's turn, the reality is this: when interest rates fall, the economy is usually already in recession and the stock market has nowhere to go.

After a four-quarter rally, U.S. stocks have started to retreat this week on concerns that the Fed will maintain a hawkish stance for longer, leading to the risk of a recession next year.

A Bloomberg survey of global fund managers also showed that stubborn inflation and recession are the main risks to stocks in 2023. Strategic analysts collectively expect the S&P 500 to fall next year for the first time since 1999.

In terms of capital flows, Bank of America, citing EPFR global data, said about $5.7 billion flowed out of global equity funds in the week ended Dec. 7.

Against the backdrop of continued high inflation, Hartnett suggested that investors could invest in commodities, bank stocks, small-cap stocks and value stocks, European and emerging market stocks may also chop better returns, and areas of investment that should be avoided include technology stocks and private equity.