Credit Card, Student And Auto Debt All Hit Record Highs In December

Content adapted from this Zerohedge.com article : Source

by Tyler Durden

The US consumer closed out 2017 with a credit bang.

While we reported last month that in November US credit card debt had just surpassed the previous all time high hit in July 2008 just before all hell broke loose when Lehman filed for bankruptcy two months later, there was a slight chance that in December this number had declined after the record surge in November credit-funded spending (which was just revised from $28BN to $31BN).

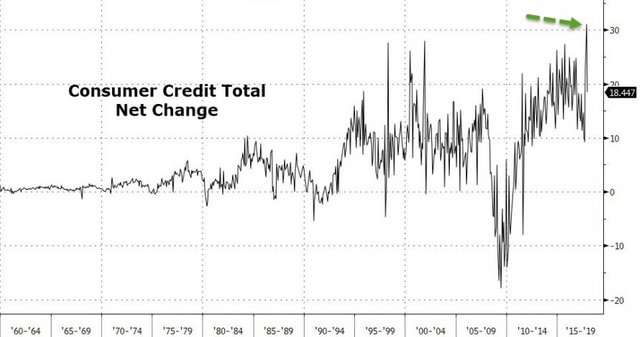

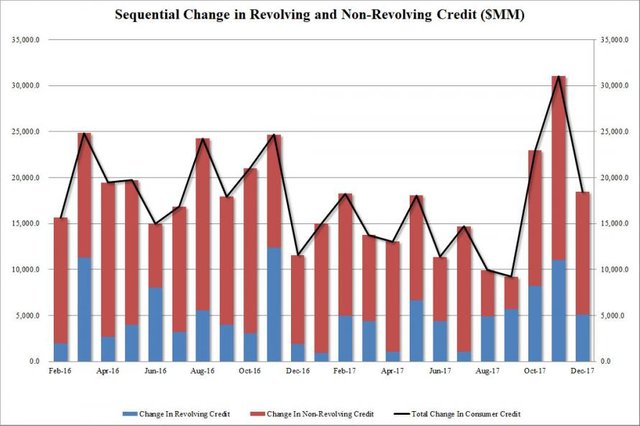

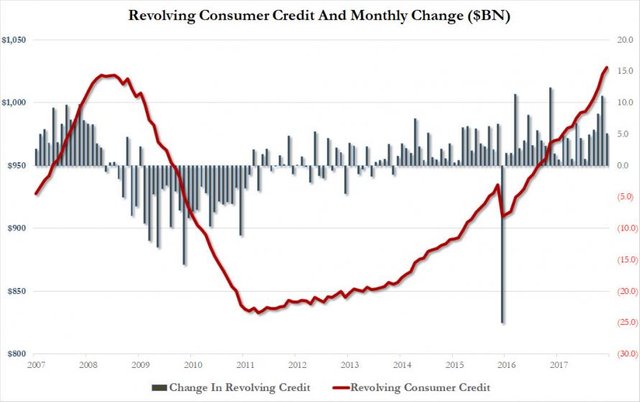

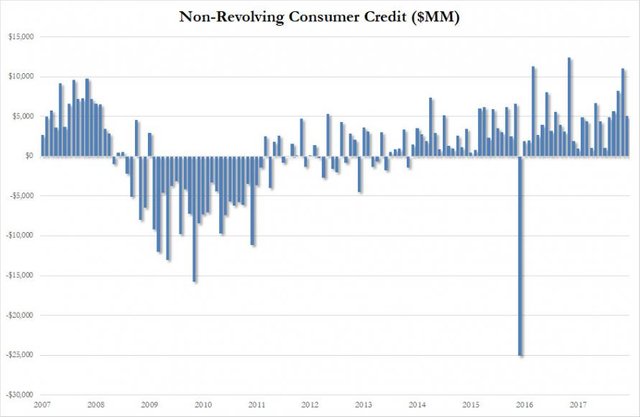

Well, that did not happen, and while December total consumer credit increased by less than the expected $20BN, it was still an impressive $18.45BN, of which $5.1billion was credit card debt and $13.3 billion non-revolving - or student and auto - loans.

More importantly, with the latest $5.1 billion increase in revolving, or credit card, debt the total is now $1.027.9 trillion, the highest number on record.

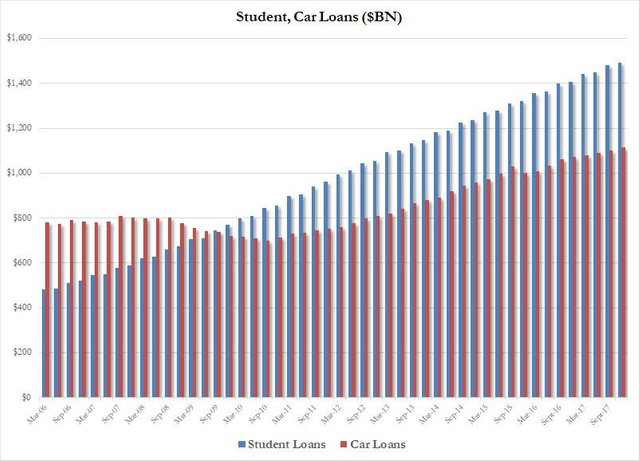

Meanwhile, non-revolving credit which with the exception of one definition change month, has never gone down, also hit a new all time high of $2.813 trillion, a monthly increase of $13.34 billion.  What about its components? Well, with everything else going for record highs, we doubt it will be a surprise to anyone that both student debt and auto loans hit a new all time high in the quarter ending December 2017, with $1.491 trillion for the former, and $1.11 trillion for the latter.

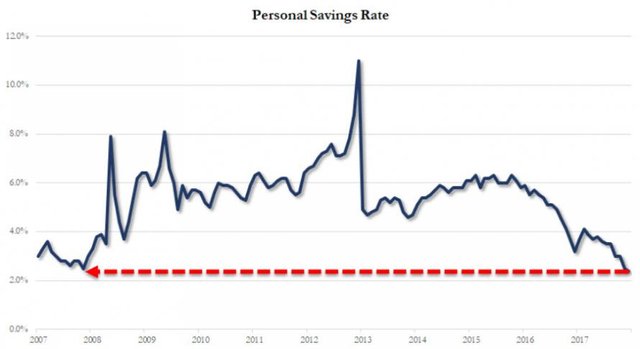

What about its components? Well, with everything else going for record highs, we doubt it will be a surprise to anyone that both student debt and auto loans hit a new all time high in the quarter ending December 2017, with $1.491 trillion for the former, and $1.11 trillion for the latter.  So for anyone still wondering why the US economy closed 2017 with an upward GDP burst, here is your answer. The problem is that with the personal savings rate just shy of all time lows...

So for anyone still wondering why the US economy closed 2017 with an upward GDP burst, here is your answer. The problem is that with the personal savings rate just shy of all time lows...  ... and with US consumers deep in the red on their household debt, just what will keep the US economic expansion going from this point on is far less clear, especially if the stock market has now peaked, as recent events suggest.

... and with US consumers deep in the red on their household debt, just what will keep the US economic expansion going from this point on is far less clear, especially if the stock market has now peaked, as recent events suggest.

Most people hardly ever feel what it's like to not be in debt. How can it be a surprise that savings is so low when credit card debt is so high? The long term health of this countries people is in jeopardy, I mean, you can only take so much before there's nothing left to give and we stop calling it credit card debt and give it's true name, slavery. Though, a lot of people are to blame for buying things they can't afford, there's still a good number of people that, even with good financial sense, can't get out from underneath that damn rock.

Thanks for helping to bring what's going on into a better focus for me! Definitely a good birds eye view of a lot of different things for one who spends a lot of time in the creative world.

The desire to earn easy money is prevailing. When people saw crypto boom, they decided to jump in. The auto loans are increased, because saving went in cryptos and if someone would finance his/her car with 50/50 savings/loan scheme now is financing with 10/90 or 0/100.

This is why I kept saying that all this reminds me the housing bubble but with many different elements, new elements.

what do you think now, after the Q1?

Yeah, FOMO all the way. Then when suddenly the market turns upside down their worse off than before :\ We headed for another financial crisis of some kind, that's for sure.

Credit card companies are trying to protect themselves by tightening credit lines, increasing standards, and closing deposits. These organizations are also reducing rewards, raising interest rates and increasing credit card fees to avoid more harm.In the United States, the administration last month approved a law limiting credit card fees and interest rates.

Welcome to the credit fueled US economy. Is the house's foundation made of flimsy wooden stilts? I've held off from investing in the equities market and am currently hedging the USD and equities market with crypto.

TTGL has come to conclusion that it will go on until hyperinflation is so apparent, the .gov can’t lie anymore. Until then,PPT will prop up any market melt down, print print and buy all the bonds. The date of obvious hyperinflation is anyone’s guess. This shit shoe has gone much longer than TTGL would have ever thought. When the plebes realize hyperinflation, then it ends. TTGL heard of hyperinflation risk going back to 2002, when he came to realization of what crap the dollar is. Been watching the shit show since....in awe.

There are plenty of part-time, high-turnover, temporary and 1099-gig “jobs” at low wage levels, geared to those with “somethin’ comin in’ from spouses, ex spouses or welfare and child-tax-credit welfare. They are often just 19th century sweatshop-style piecwork. The now-doubled, refundable child tax credits up to $6,444 now equal more than 1/3rd of what many full-time jobs pay for the entire year. When you cannot cover a full range of household bills, including rent that consumes half or more than half of your monthly pay, with earned-only income, a job is not really a job. It is a gig, like the babysitting gigs worked by teenagers for pocket money, when their major bills are paid by unearned income from their parents. Employment numbers should separate the bill-including rent that consumes half or more than half of your monthly pay, with earned-only income, a job is not really a job. It is a gig, like the babysitting gigs worked by teenagers for pocket money, when their major bills are paid by unearned income from their parents. Employment numbers should separate the bill-paying jobs from the gigs.

I wonder why so many people are comfortable with debts and loans. If inflation continues and salaries rise, the debt would be less. Don't see many other solution on that.

Thanks for this valuable post sharing...this is the great post dear....resteemit done

i wonder how the US economy functions with so much debt , floating around further more how will the future generation thrive having so much debt?

@zer0hedge..Half of the people on welfare — more when you count child-tax-credit welfare — are white. A higher percentage of minorities are on welfare, though. Sadly, Black men — the group hardest hit by mass-scale, welfare-boosted immigration, get lumped in with the womb-producing welfare consumers, although they qualify for near-zero welfare. The reason Hispanic men benefit is that they are sole breadwinners, rather than their women, in multi-family households, where more than one momma collects $450 per month on average just in free food for US-born kids, when the father of her kids works part time, staying below the earned-income limit for welfare in [traceable] income. Most Black men, like childless/single women, non-custodial parents and single moms This is a self-sustaining system, keeping wages AND, more importantly, hours down, as womb-producing welfare consumers have a financial incentive to work few hours for mostly low wages. They qualify for welfare that way. Too bad Barbara Jordan cannot come back to life, giving the pro-welfare-buttressed-mass-immigration, pro-wage-cutting fake progressives a piece of her mind..thank you for sharing with us

Revolving credit, like credit cards, rose 6% in December, less than half the 13% pace seen in November. Revolving credit is $1.03 trillion, the highest on record. Nonrevolving credit, typically auto and student loans, rose 5.7% in December after an 8.6% rise in the prior month.

In the fourth quarter, consumer credit rose at a 7.7% annual rate, the strongest quarter of the year. For all of 2017, consumer credit rose at a 5.4% rate, down from a 6.7% rate in the prior year. Most of the slowdown was in nonrevolving credit. The data does not include mortgage debt.