Government Deficits and Debt, Biases versus Reality.

The ability of government deficits in order to help the overall economy has been an ongoing controversy in economics. Some theories argue that deficit spending should be avoided by any costs, some that it might help the economy in a short-run during the periods of economic downturn, but will fail in a long-run and some that government deficits are necessities during recessions. Economists who believe that fiscal policy is an effective tool to end or balance the down-turned economy derive their ideas from John Maynard Keynes. Keynes believed in the power of fiscal policies during times of economic recessions and depressions. The reason for excessive government spending is to bring back the aggregate demand, restore healthy economic growth, inflation and levels of employment.

Keynesian theory argues that fiscal policy is an effective government tool. According to Keynes, deficit spending implemented correctly can help a weakened economy to become stronger and end the recession. Increases in government spending under the condition of high unemployment essentially brings up the aggregate demand, by creating demand for business output, therefore GDP rises along with level of employment. When the government deficit is spent on increases in human capital, such as education, healthcare and infrastructure; not only does it create jobs but it also leads to increases in both short-run and long-run output.

An essential part in interpreting Keynesian ideas and understanding the benefits of government deficits is Canadian professor of economics, William Vickrey. Vickrey wrote “Fifteen Fatal Fallacies of Financial Fundamentalism “, and was awarded the Nobel Memorial Prize in Economic Sciences, for his writing

Vickrey's Fatal Fallacies

In the “Fifteen Fatal Fallacies of Financial Fundamentalism”, William Vickrey argues about false of modern “economical wisdom” (Vickrey). He argues that most people and politicians build their views and understanding of economy on, “Incomplete analysis, contrafactual assumptions and false analogy”(Vickrey), of course this paper was written in 1996 and some of that economical wisdom has been changed and shaped through years especially since the recession of 2008. However, the ideas that William Vickrey were arguing for has been proved to be true, partly because of the recession. I will discuss and evaluate several fallacies that are arguing directly about government debt and deficits.

Fallacy I

The first fallacy is the belief that deficits are “Sinful profligate spending at the expense of future generations who will be left with a smaller endowment of invested capital.” (Vickrey) In other words this is the idea that deficits are effective in a short-run but in a long-run it will contract public investment and hurt the economy. Vickrey argues that it is exactly opposite; deficits increase net disposable income of the individual. They provide markets for business outputs, forcing producers to increase their production, which leave future generations with already higher output.

In Keynesian theory, the economy is highly dependent on aggregate demand and when this decreases the circulation of money stops, leading to a recession. In this case deficits force private savings to be recycled and invested; therefore money is circulating again and the economy grows back up. A real life example of this is the economic prosperity of 1950’s and 1960’s. At the beginning of WWII, American economy was still slowly recovering from the Great Depression. When the government started to run massive deficits on war expenditures it boosted the recovery. As a result not only did it reduce unemployment and stabilized the economy in the short-run, it had positive effects in the long-run. The economy was roaring in the 1950’s and 1960’s with low unemployment rates and healthy growth of GDP.

Fallacy II

The third Fallacy is that Government borrowing crowds out private investment. In Vickrey’s view when borrowed funds are being spent they enhance profits of private investments by increasing the demand for private goods and increasing overall output. Than multiplier plays its role each borrowed dollar that is spent multiplies and creates more than one dollar of private investment. Although he agrees of possible crowding out effect as an inappropriate implication of monetary policy as a response to the deficit.

Indeed the Government deficit in theory should not have crowding out effect on private investment; however, private investments after recent recession in United States were low for several years. Crowding out private investment can be considered an issue of expectations. Even though monetary policies brought interest rates low, it took a while for people to start investing again, because their expectation were very low. According to Keynesian theory of expectations, expectations are irrational, for people tend to think that present is much more serviceable guide to future, rather than logical evaluation of past events. Therefore it took time for people to set into a relative stability and start investing. (Fig. 1). The graph represents private investments as a percentage of GDP. The investment spending is show as rising over last five year, continuing to have a rising trend and currently at 16.937 percent of GDP. It is not as high as it was before the recession, however it is important to keep in mind that it is on the rising. As more stable the economy will be the higher private investments are going to be.

Fallacy IIX

The eighth fallacy is the assumption that if the government keeps running deficits, the debt will “Swamp the fisc” (Vickrey), in other words the debt will become too big and consume all the tax revenue, confidence will fall, and bonds could not be sold anymore, as a result government borrowing could not be possible. Vickrey argues that the economy will be sustained at or close to a full employment with healthy growth and inflation, the most part of the debt will be financed out of the growth, leaving minor part of the debt to be paid from the taxes. He points out a very sufficient point that bigger debt is easier to deal with if the economy is healthy, as not that much needed to be spent for unemployment benefits and welfare; meanwhile it is much harder to take care of a three times lesser debt when the economy is struggling, “In the doldrums with its equipment in disrepair” (Vickrey).

Consistency

This argument, in fact all of them, are very much consistent with the Nobel Memorial Prize winner in Economic Sciences, Paul Krugman's argument about debt. Krugman argues that people in DC have a wrong understating of debt and that they are incorrect about short-run and long-run effects of budget deficits. “The way our politicians and pundits think about debt is all wrong” (Krugman, Debt). He compares their view of the U.S debt to the family who have troubles paying their monthly mortgage payments. He points out that American debt is money that are not owed to somebody else but to owed “ourselves”. Government borrows by issuing bonds, securities and bills. And of course government must pay interest and in order to pay the interest taxes must be levied. Therefore debt these days does not have that much meaning as it may seem. Krugman and Vickrey both argue that debt is not as dramatic as it might appear. Krugman said that debt matters, but several other things are more important, “We need more, not less government spending to get us out of our unemployment trap”(Krugman, Debt). Indeed Vickrey’s argument is that priorities must be set right, debt is much more feasible to deal with when the economy is at or close to full employment and have a healthy growth with healthy inflation and unemployment at natural rate. Krugman’s and Vickrey’s arguments are basically complements to each other, those fallacies illustrate the most recent recession of 2008.

Origins of United States crisis of 2008 has roots not only in a low interest rates but in a prolong period of economic growth and stability. Banks issuing subprime mortgages to low income families, with funding through securitization, in other words by issuing bonds. People had really high expectations convinced that the value of their houses will keep rising. Of course the risks of mortgage backed securities have been highly underestimated. While they were aggressively defaulting, insurance companies, banks, and investors were losing. Government acted immediately by supporting and bailing out banks in order to sustain aggregate demand. Besides expansionary monetary policies large government deficits were applied in order to help the economy, The Economic Stimulus Act of 2008 enacted with the total cost at $152 billion which increased budget deficits from 5% to 15% of GDP (Radice). Later the American Recovery and Reinvestment Act of 2009 (ARRA) was enabled.

ARRA was signed into law on February 17, 2009 by President Barack Obama, the main purposes of the act were to create new jobs and save existing ones, spur economic activity, invest in long-term growth, foster unprecedented levels of accountability and transparency in government spending. Total expenditures estimated at about $840 billion and allocated between tax benefits, contracts, grants and loans and entitlements: currently around $816.3 billion were paid out (Recovery.gov). Some economists, such as Joseph Stiglitz and Paul Krugman advocated that the deficit spending should be more in order to back up the economy. Krugman says that the problem with ARRA that is was “Too small and too short-lived to do the job” (Krugman, The Stimulus Anniversary), government expected that the healthy state of the economy will be back quickly, however, as we see it is not exactly the case. It is undoubted that the Stimulus has a positive effect on the U.S economy. There is a large possibility if the government would not reacted as they did and would not run massive government deficits the U.S economy could have faced something very similar to The Great Depression of 1929 and had a long recovery period. Nevertheless, current debt has a different aspect. A lot of it is held by foreign and international investors.

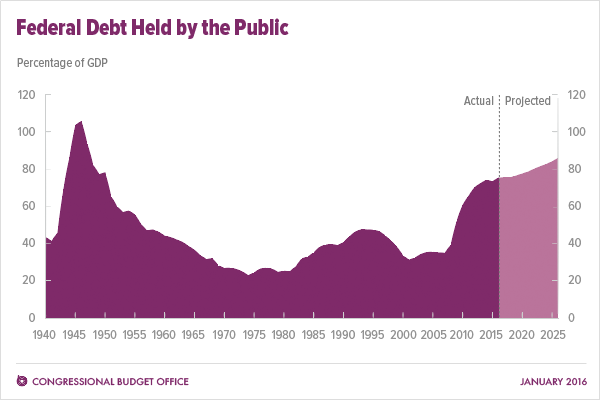

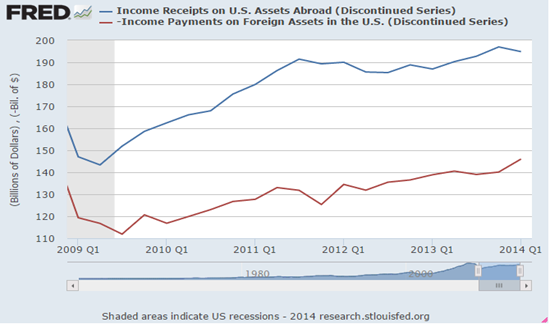

The amount of current debt is $18.96 trillion of dollars or about 75% of GDP, meanwhile the amount foreign debt before the recession in 2007 was 2,294.5 billions of dollars or 17.09% of GDP (U.S. Department of The Treasury. Fiscal Service). There is a tremendous increase in foreign debt, however it is not bad. Most foreign investors tend to put their investments into safe assets that do not have a large yield. So U.S. assets abroad are bringing more money that the payments on foreign-owned assets in U.S. (fig 2). The graph represents the income receipts on U.S. assets abroad (blue line) and income payments on foreign assets in the U.S. (red line). As we can see receipts are higher than payments. Aside of very biased common knowledge that U.S. is very much bound to foreign investors, especially Chinese, foreign debt actually generates revenue for the American nation. So it has a positive effect on the economy. The reason why it should not change for while is because foreign investors are interested in keeping the U.S. economy healthy. They have already invested more than enough to not want the American economy to fall into recession again, as those investments generate profits for them.

Overall we see that in theory government deficits are essential in helping the economy during economic downturns. It is important to realize that deficits are not the tool the government can use in order to fix the economy, monetary policies may be implied to. For instance if excess government spending resulted in higher interest rates which could crowd out private investment, crowding out could be prevented by increase in money supply which is supposed to bring the interest rates down. When the economy is restored there is no need for large deficits or deficits at all. Debt should not be a problem either with healthy growth in GDP and inflation while unemployment rates being close to natural rate, majority of interest on that debt is going to be covered by growth, meanwhile minority can be covered through tax levy.

In conclusion it is safe to say that government deficits helped the American economy to get out of two major crises: The Great Depression of 1929 and The Great Recession of 2008. However, it would be unfair to expect the same long-run consequences as they were after the Great Depression. We live in a different century where much has changed since then. It is also important to remember that WWII left majority of the developed world shattered, meanwhile the United States was almost untouched.

Works Cited.

"Recovery.gov/Arra." Recovery.gov Is the U.S. Government's Official Website That Provides Easy Access to Data Related to Recovery Act Spending and Allows for the Reporting of Potential Fraud, Waste, and Abuse. U.S. Government, n.d. Web. 03 Dec. 2014. http://www.recovery.gov/.

Vickrey, William. "15 Fatal Fallacies of Financial Fundamentalism." Vickrey, William. 1996. 15 Fatal Fallacies of Financial Fundamentalism. Columbia University, n.d. Web. 04 Dec. 2014. http://www.columbia.edu/dlc/wp/econ/vickrey.html.

Krugman, Paul. "The Stimulus Anniversary." Paul Krugman The Stimulus Anniversary Comments. New York Times, 18 Feb. 2014. Web. 04 Dec. 2014. http://krugman.blogs.nytimes.com/2014/02/18/the-stimulus-anniversary/.

Radice, Hugo. "Cutting Government Deficits: Economic Science or Class War?" Capital & Class (2011): 35-125. Sage Journals. Sage Journals. Web.http://cnc.sagepub.com/content/35/1/125

"Federal Reserve Economic Data." FRED. Federal Reserve Bank, n.d. Web. 03 Dec. 2014. http://research.stlouisfed.org/fred2/

Krugman, Paul. "Nobody Understands Debt." The New York Times. The New York Times, 01 Jan. 2012. Web. 01 Dec. 2014. http://www.nytimes.com/2012/01/02/opinion/krugman-nobody-understands-debt.html?_r=0.

Excellent blog and well written great content and research thanks for your insight!

Thanks!

This is one of the better discussions of national debt in relation to economic growth that I've seen. Thank you.

Thanks! I'm glad to see your positive review. Follow me, if you want learn more