10 Cartoons That Masterfully Illustrate the Lunacy of Central Bank Policy

I’m a big fan of Hedgeye. Actually, it’s Bob Rich’s artwork I’m a fan of. He’s the cartoonist who creates almost daily for the investment research firm Hedgeye. His cartoons typically relate to some macroeconomic theme, and often expose the idiotic practices of central bankers.

Central Banking 101

Your central bank controls the money supply in your nation. It does so by manipulating interest rates in the overnight bank lending market, by setting bank reserve capital requirements, and sometimes even by creating new money to buy financial assets (quantitative easing).

Since 2008, central bankers have gone on a money-printing bonanza, nearly tripling the total supply of money around the world. If you’ve noticed your groceries getting more expensive, or your food packages getting smaller, you can thank your central bankers.

Here are 10 of my favourite Bob Rich cartoons, with a little commentary on what I believe is most wrong with our world’s prevailing monetary system:

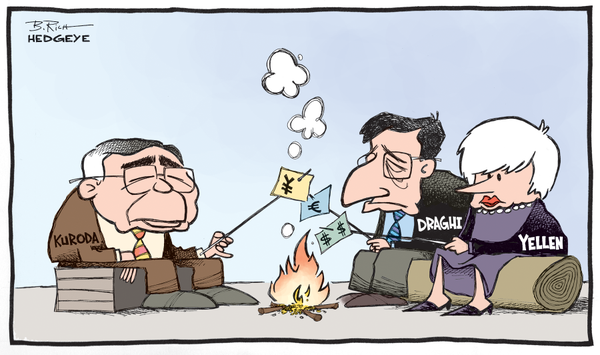

1

The four largest economies in the world are the United States (US), the European Union (EU), China, and Japan. The US alone makes up 25 percent of the world’s GDP, and the US and EU together amount to over 47 percent. Add Japan to the mix, and these big three colluding central banks control over 53 percent of the world’s wealth.

Haruhiko Kuroda heads up the Bank of Japan (BOJ), Mario Draghi presides over the European Central Bank (ECB), and Janet Yellen oversees the Federal Reserve (Fed). They are affectionately caricatured above, roasting their respective currencies over a monetary bonfire.

Around $6 trillion dollars worth of value has gone up in smoke since 2008, thanks to these three. We haven’t yet experienced the full pain of this monetary weenie roast, but it won’t be much longer until we do.

I should probably also give a shout out to Ben Bernanke, Yellen’s predecessor. He’s the one who got the party started, although Yellen was his sidekick until she took over in 2014.

By the way, China, the third largest economy in the world, has had its printing presses running non-stop for the last 15 years. The People’s Bank of China (PBOC) has amassed the largest money supply in the world, inflating annual GDP growth in the range of 6 to 9 percent.

2

These three central banks are no doubt building an economic house of cards. Like any flimsy structure lacking a solid foundation, our current world economic system is destined to collapse.

Prior to the early 1970s, the value of the US dollar was connected to the price of gold. Most currencies could be converted to physical gold, which meant a nation was required to hold reserves of gold as a basis for its currency’s value. This prevented central bankers from printing money willy-nilly. To increase the money supply, they had to either acquire more gold or openly re-price their currency in gold terms.

Economists began to see this adherence to a gold standard as restrictive to economic growth. They believed that other, less tangible factors should be considered when determining how much money a central bank should be able to create.

“Fiat” currency was their answer; money backed by nothing more than a government decree or promise to pay a debt. The chains were off. These fiat currencies were floated on open exchanges for traders to determine their worth, rather than having fixed values. As long as enough people believe in the government backing the currency, then the system is sustainable.

However, without an objective basis for value, central bankers have had very little accountability, and the potential for new money creation has become theoretically limitless. The more money that’s created, the less valuable it becomes, even if currency traders have not yet priced in the full impact of the dissolution.

Since these changes in the early 1970s, the US dollar has lost over 97 percent of its value relative to the price of gold. That’s a massive loss in buying power, and points to the inflationary impact of new money creation.

The longer this goes on, the more fragile the monetary system becomes. More and more cards are laid upon an already foundationless and flimsy base. Even a slight economic wind, like an insolvent German bank perhaps, can unsettle a few connected cards, which causes a chain reaction that brings the entire monetary house of cards down.

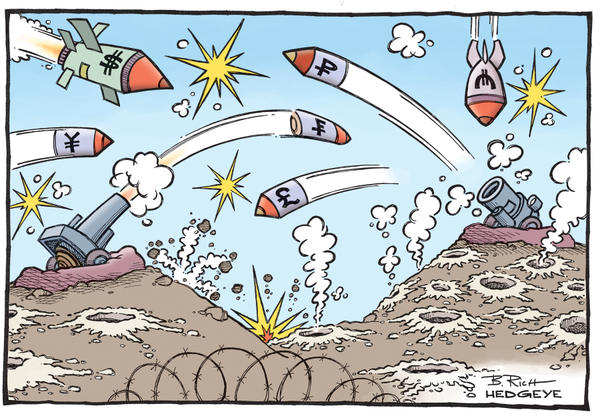

3

When one nation devalues its currency, especially one with a dominant monetary system like the United States, it negatively impacts international trade in other nations. For example, in Australia, we are primarily a raw material and commodity export economy. The export of iron ore to China has been one of our primary sources of economic productivity.

The more the Fed devalues the US dollar, the weaker the Dollar becomes, but relative to the US dollar, the Australian dollar strengthens. Since most nations trade using US dollars, and since China for a long time was pegged to the US dollar, the US dollar devaluation has been a major problem for Australia, because it makes our exports more expensive.

To help our exporters remain competitive, our central bank, the Reserve Bank of Australia (RBA), has responded by also devaluing the Australian dollar. In fact, virtually all central banks have been forced to do the same thing. This is what's referred to as a currency war. Nations are dropping monetary devaluation bombs on other nations in an effort to gain economic superiority.

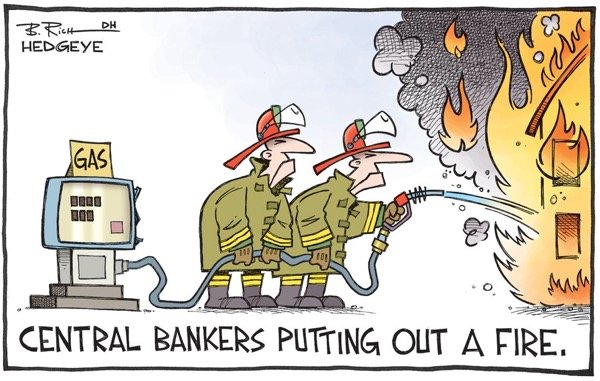

4

These competitive currency devaluations are intended to spur economic growth. One of the major problems with the world economy at the moment is a very low level of economic productivity. Central banks keep lowering interest rates to boost inflation, but none of the new debt being created is improving economic productivity.

The reason is because the lower interest rates and new money creation are the very problem. They are the fuel stoking the deflationary fire. Central bankers think they are fixing the problem, but they’re actually making it worse.

Rather than using the money to invest in productive assets that will improve the economy, investors are borrowing to buy inefficient assets like real estate and company shares. This is called malinvestment, and is one of the biggest problems with artificially low interest rates.

In Australia, property investors continue borrowing to speculate on more and more increases in home prices. In the United States and Europe, bond prices and stock values have continued to rise. Soon, the proverbial house will burn down and these asset bubbles will burst, when either interest rates rise or people lose faith in central bank’s abilities to prop up asset markets.

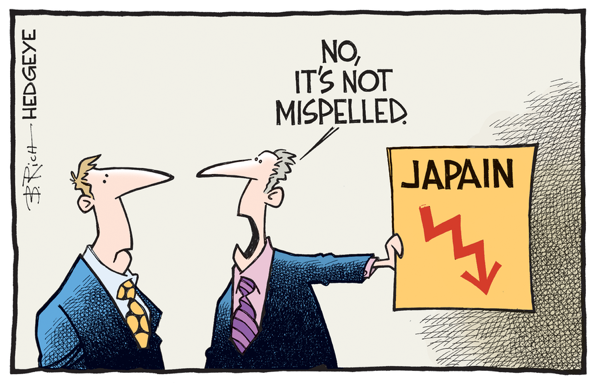

5

Japan is the ultimate example of the futility of central bank intervention. The BOJ has held its target interest rate near zero since 1990, and below zero since January of this year. To what effect? Japan's average annual growth rate since 1980 has been a dismal 0.48 percent.

Japan also has the highest ratio of sovereign debt to GDP of any nation in the world. A third of all of Japan’s government debt is actually owned by its central bank, mainly because no one else wants to buy their bonds.

Has this complete and utter failure of Japan's central bank discouraged other central bankers around the world from taking the same path? Of course not. Just because monetary easing hasn’t work for Japain doesn’t mean it can’t work in the USA, Europe and China.

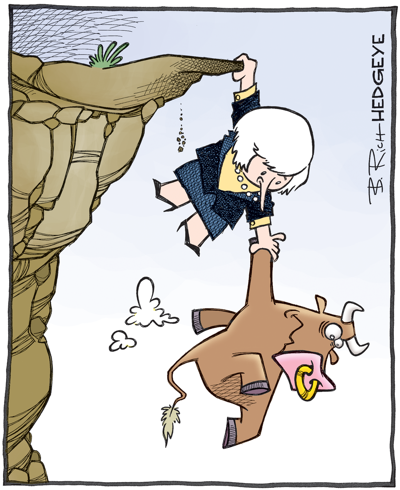

6

Now back to Yellen, and her asset bubble...

The US stock markets have had quite a run, continuing to move higher and higher since their lows of 2009. Whenever it appeared that stock values may fall, the Fed stepped in to prop their values up. For most of this year, stocks have been showing signs of rolling over, but Janet Yellen and company seem committed to keeping the bubble inflated.

At this point, the bull market in stocks is dangling on the edge of a cliff, with only the Federal Reserve keeping it from plummeting to its death.

7

The Fed kept interest rates at a record low zero percent from 2009 to December 2015. Janet Yellen hiked the cash rate 0.25 percent and announced a steady path to normalizing rates to around 4 percent. Since then, she’s made plenty of threats, but because the world economy is growing at a snail’s pace, she’s powerless to follow through; that is, unless she decides to willingly crash asset prices and send the world into a deflationary death spiral.

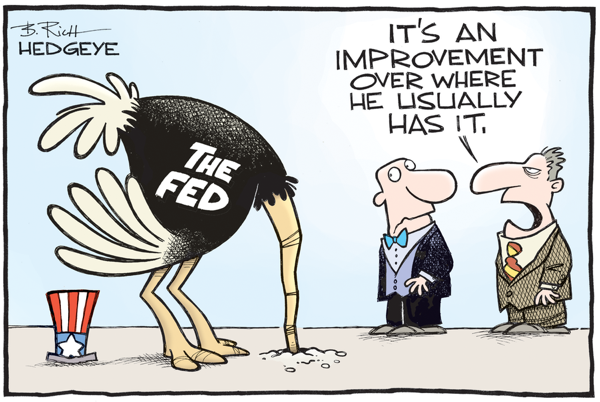

8

Amidst her inaction and empty threats, Yellen needs to save face. It's crucial that people maintain faith in central bankers.

To keep the charade going, she keeps flip-flopping back and forth between hawkish rhetoric (“things are looking up, we’re about to raise rates”) and a dovish stance (“the economy is struggling, so we need to hold rates steady”). It’s only a matter of time before the world wakes up and realizes the Fed is powerless to truly fix anything.

9

This one is my favourite. It needs no explanation :)

10

One of the greatest current threats to the 7 billion people of the world is the prevailing centralized monetary system. That’s one big reason I’m here on Steemit – to take part in what could become a viable decentralized alternative to the lunacy of central bank policy.

For more from Bob Rich, check out his latest work on Hedgeye’s “Cartoon of the Day” or follow Hedgeye on Twitter: @hedgeye.

Image Credits:

- featured image of Kuroda-Draghi-Yellen

- 1. currency burning

- 2. house of cards

- 3. currency wars

- 4. fuel on the fire

- 5. Japain

- 6. hanging on

- 7. Paul Revere on a snail

- 8. hawk-dove

- 9. ostrich

- 10. curious aliens

All images have been shared under fair use.

@jasonstaggers

Please follow me if you enjoyed this post. Thanks!

Great explanation and cartoons that are spot on! From our previous convos it sounds like it's time to short the Australia housing market. Wonder if they have MBS trading there cus we didn't in the U.S. until someone had them created so he could short the housing market.

Australia market really is starting to sound like U.S. just before the housing bust. Big opportunity may be sitting at our feet. I need to dig into this and see how far along you guys are in these housing boom.

The banks here have bundled their loans and sold them as MBS, but they are preforming relatively well so far. Arrears in the subprime market are around 4%, and 1% on prime loans. Many Aussies have large savings and are ahead on their mortgage payments so things look ok for now.

But that doesn't mean it's a safe market. All loans here are variable, so once rates start to tick back up, it could be a major problem, especially for those who have bought in the last 2 to 3 years, at the peak.

Credit default swaps against MBS were created prior to the GFC and have hung around here in Aus as hedges for investors against bond defaults. If you wanted to bet against the Aussie property market, shorting the bank stocks would be the way to do it for a small time investor. Or buy gold miners, which you can afford to be a little early on and not get into trouble.

There was quite a lot of talk about shorting Aussie real estate a few months ago. Here's one article: http://www.smh.com.au/business/big-short-on-aussie-banks-will-take-years-if-true-jpmorgan-says-20160303-gn9zpu.html

Thanks for the insight. Will check out the article. Warning signs in the U.S. started in 2005 and it really wasn't until 2008 when stuff hit the fan.

Very true. I would have said there were warning signs here a few years ago, although not flashing like they are today. With the RBA committed to low interest rates, the party may keep going a few more years. I think the primary risk to Aussie property values is the overseas lending market drying up. Another credit crunch would be devastating. When it happens, so many people will be caught off guard.

Awesome. Brilliant compilation and thanks for sharing. Upvoted and shared on Twitter✔ for my followers to see. Great post. Cheers. Stephen

Many thanks Stephen.

Love the cartoon, the post wasn't to bad either lol. Give the money to you and you can sort the world out :)

Haha, no thanks. I'm sure I'd screw it up too :)

You couldn't do any worse.

Good point!