Cryptocurrency: A valid retirement plan?

Setting the Stage

As a young recent college graduate in the U.S. I find myself in an interesting position as far as my financial future is concerned. I find myself attempting to compare my financial position to that of my parents during the same stage of their lives and wondering; “will I ever get to enjoy the same level of financial security and prosperity as that of the current crop of middle aged Americans?” This is a profound question and one worth exploring in some detail.

The idea of retirement and wealth building investment is not on the forefront of the minds of many young Americans, or is not easily accessible to those that are looking ahead to their future. A personal belief that I hold is that government retirement programs will not be reliable going toward the future and therefore, I need to take a different route to secure my future. An exploratory analysis of current economic conditions in the U.S. will provide valuable insight into the question presented by the author.

The Federal Reserve Economic DataBase (FRED) reported a 35.14% increase in Rent CPI from the first quarter of 2010 to the last quarter of 2019. Furthermore, the FRED Rent CPI report indicates that the rise in rental prices has risen an average of 19.54% in the past four years.

A pertinent frame of reference for this inquiry lies in the reported FRED CPI Inflation Rate for the years 2010 to 2109, 18.86% with the value in the past four years at 10.13%. With the Rent CPI outpacing the CPI Inflation Rate a certain level of concern arises for the average young American.

In addition to these issues, we must consider debt both in student loans and other debts incurred by the average young American (Car loans, Credit Card Debt, etc.). First the total amount of student loan debt, as reported by the FRED database, has risen from $800 Billion to $1.6 Trillion, a 105.38% increase from 2010 to 2019. Rising costs of education and increasingly high levels of personal student loan debt increase the financial strain on young americans. Credit card debt is rising in the U.S., likely a result of increased levels of consumer confidence and some rising incomes in certain sectors. It is difficult to deny that the ownership of a personal vehicle is necessary to many in the U.S. As such, this functional necessity in modern society creates another point of headache in the calculus of the young American’s budget.

As a teenager a common piece of investment advice prevailed in discussion among family members, teachers, and close friends; BUY A HOUSE. I have been told throughout my life that purchasing a home would be the most critical investment that I make in my life. Having spent my young life in a suburban neighborhood in Washington State, this seemed like a good idea. I still carry the belief that this is true however, increasingly I find myself wondering if that goal is within my reach. For those interested in this path I recommend spending some time looking at housing prices throughout the U.S. The National Association of Realtors provides insightful tools into the housing market and would serve as a great basis in your exploration of this goal.

Pausing for a moment of reflection, it seems that the goal of owning a home, retiring comfortably without reliance on government programs and getting out of debt is unachievable. Let’s explore some options related to cryptocurrencies and diversification of investment.

How Cryptocurrency Fits Into the Equation

To begin our discussion of where cryptocurrencies can fit into our financial toolset we will investigate the performance of cryptocurrencies, compare their performance to other investments and discuss risk.

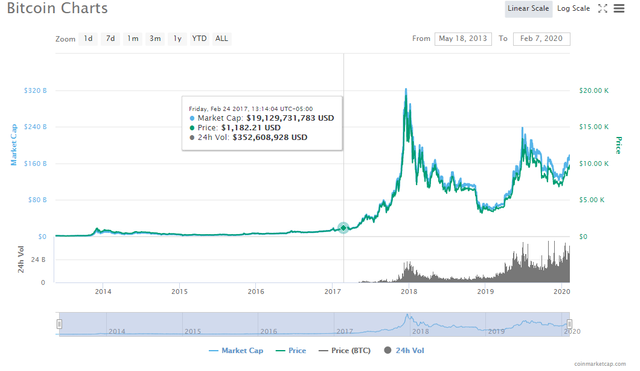

First, let’s dive into the performance of bitcoin. The following chart shows the value of bitcoin overtime.

The performance of Bitcoin in the past three years is indicative of an environment where trading in this instrument is viable as a source of income. Returns on cryptocurrency instruments have been increasing at a rapid rate recently. The following chart displays the rate of return of return on two common instruments versus Bitcoin (chosen as it is the most popular of cryptocurrencies on the market) returns in 2017.

| British Pound (%) | SP500 (%) | Bitcoin (%) | |

| Monthly return | 0.8 | 1.8 | 30.8 |

| Standard deviation of return | 1.8 | 1.6 | 25.4 |

Clearly Bitcoin has performed exceptionally on a return basis during that period, which is very exciting.

This sounds like rainbow and butterflies but, the question is will this trend continue? At this point it is difficult to say from a technical analysis point of view whether these investments will be viable far into the future. It is also important to consider the sources of risk in these markets are somewhat unpredictable. However, it seems that overall interest in these instruments are increasing in popularity and general acceptance. Consequently, there is an increasing interest in leveraging crypto-markets as a tool for diversification and short term investment income.

Additionally, the youth of these markets makes prediction of future trends and reaction to other economic conditions difficult to ascertain. Regardless of these factors, a short term investment in these investments, for those with a higher risk tolerance and a dash of patience, may be entirely viable. Furthermore, these investments are shielded from interest rate changes due to Federal Reserve activity.

Building an initial basis of wealth utilizing cryptocurrencies can provide an excellent platform for those looking to diversify holdings. With a certain degree of prudent budgeting and savvy investment an enterprising individual could find an avenue through which financial growth could be achieved. Note, I am always an advocate for frugal living and discipline in building savings, but that is a discussion for a later time and outside the scope of this exploration.

In closing, it seems that in the short term cryptocurrencies are likely very effective in jumpstarting the process of saving for retirement. The viability of these currencies in the long term is a matter for future exploration, however, I have confidence that these tools aren’t going anywhere and we will see increased utilization of them going forward.

Disclaimer and Author’s BIO:

Logan joined TheCryptoDivision in 2019 to expand the general understanding of cryptocurrencies and build a toolkit of basic economic principles to aid the budding crypto investor. Logan is an economics graduate from BYU-I. He currently works as a data analyst in the management consulting competency for one of the largest global consulting firms.

The author gets support/income for this website by donations, using affiliate marketing, and google ads. But he has never taken any financial compensation for any research or post. This is not meant as financial advice.

Follow me on:

Website: http://www.thecryptodivision.com/

Twitter: https://twitter.com/CryptoDivision

Facebook: https://www.facebook.com/TheCryptoDivision/notifications/

Steemit: https://steemit.com/@cryptodivision