Decentralized Blockchain Technology and the Rise of Concierge Coin

Decentralized Blockchain Technology and the Rise of Concierge Coin

1 Abstract

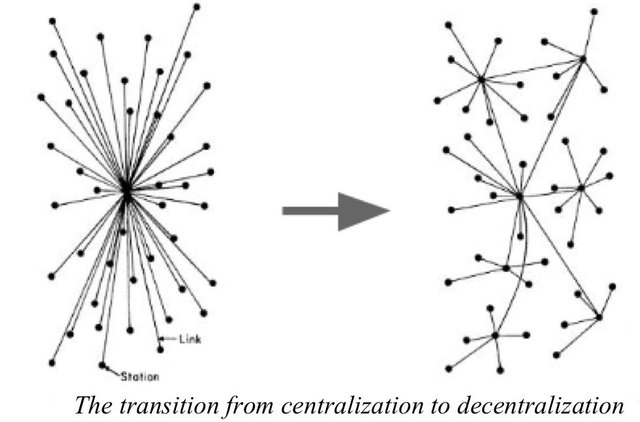

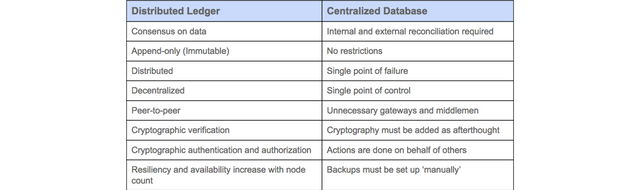

Just as decentralization communication systems lead to the creation of the Internet, today a new technology — the blockchain — has the potential to decentralize the way we store data and manage information, potentially leading to a reduced role for one of the most important regulatory actors in our society: the middleman.

Blockchain technology enables the creation of decentralized currencies, self-executing digital contracts (smart contracts) and intelligent assets that can be controlled over the Internet (smart property). The blockchain also enables the development of new governance systems with more democratic or participatory decision-making, and decentralized (autonomous) organizations that can operate over a network of computers without any human intervention. These applications have led many to compare the blockchain to the Internet, with accompanying predictions that this technology will shift the balance of power away from centralized authorities in the field of communications, business, and even politics or law.

In this Article, we explore the basics of blockchain technology and how it benefits the decentralized technology as applied by ConciergeCoin and to argue that its widespread deployment will lead to expansion of a new level of trust in the travel world. As blockchain technology becomes widely adopted, centralized authorities, such as monopolizing Online Travel-, governmental agencies and large multinational corporations, could lose the ability to control and shape the activities of disparate people through existing means. As a result, there will be an increasing need to focus on how to regulate blockchain technology and how to shape the creation and deployment of these emerging decentralized organizations in ways that have yet to be explored under current legal theory.

I. OVERVIEW OF BLOCKCHAIN TECHNOLOGY

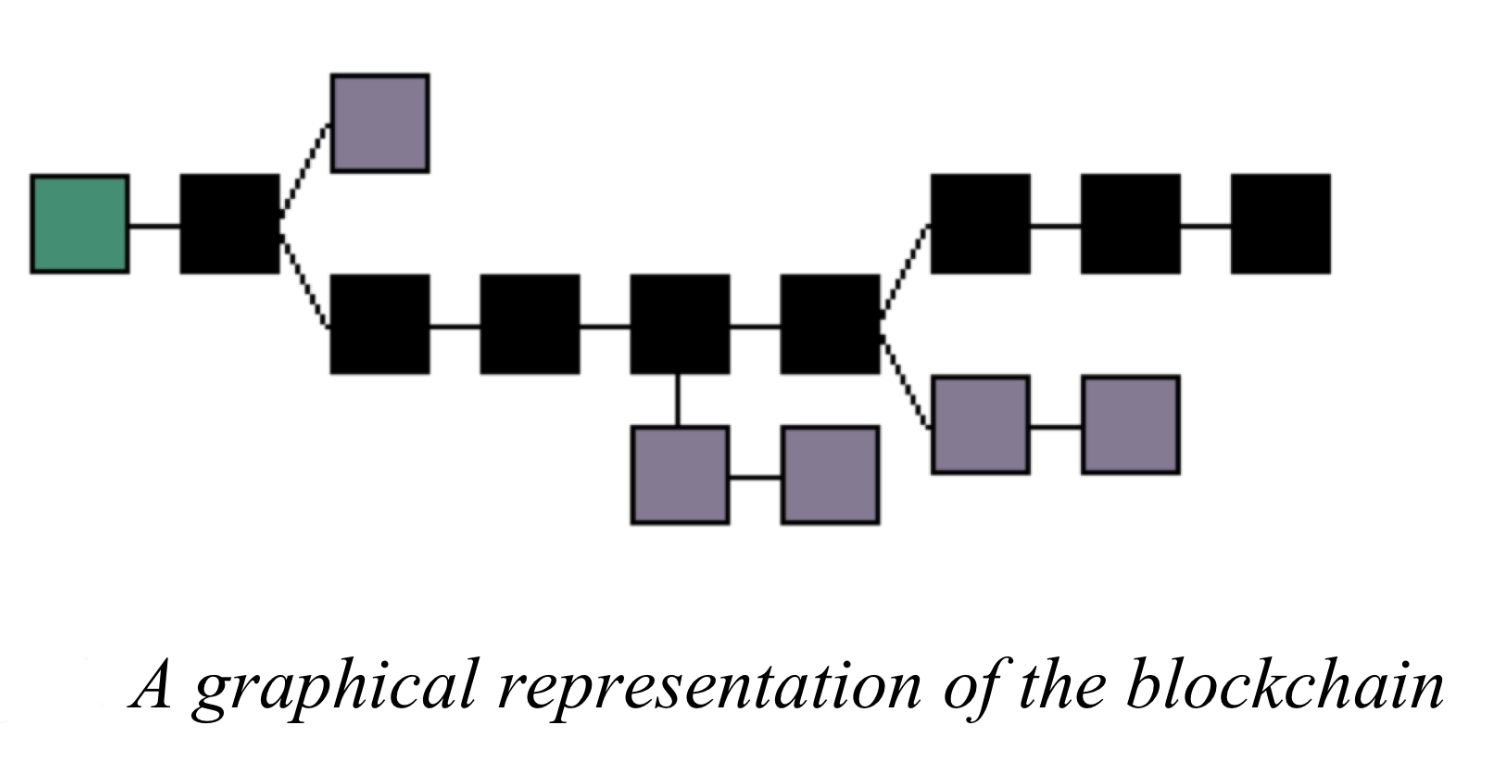

Blockchain technology represents the next step in the peer-to-peer economy. By combining peer-to-peer networks, cryptographic algorithms, distributed data storage, and a decentralized consensus mechanisms, it provides a way for people to agree on a particular state of affairs and record that agreement in a secure and verifiable manner. Prior to the invention of the blockchain, it simply was not possible to coordinate individual activities over the Internet without a centralized body ensuring that no one has tampered with the data. A group of unrelated individuals could not confirm that an event had occurred without relying on a central authority to verify that this particular transaction was not fraudulent or invalid. In fact, many computer scientists did not believe that distributed group of people could reach consensus without a common clearinghouse. This notion is encapsulated in a well-known computer science problem from the early 1980s, commonly referred to as the “Byzantine Generals Problem.”This problem questioned how distributed computer systems could reach consensus without relying on a central authority, in such a way that the network of computers could resist an attack from ill-intentioned actors. It posits that three divisions of the Byzantine army are camped outside an enemy city in hopes of conquering it. An independent general commands each division and, in order to plan an attack, they need to decide upon a common course of action. Yet, the generals can only communicate with one another through a messenger, and there is a traitor in the group who is actively trying to prevent the generals from reaching an agreement by either tricking them into attacking prematurely or concealing some relevant information so that the generals cannot plan a coordinated attack. A blockchain solves this problem through a probabilistic approach. It forces information traveling over a network of computers to become more transparent and verifiable using mathematical problems that require significant computational power to solve. This makes it harder for potential attackers to corrupt a shared database with false information, unless the attacker owns a majority of the computational power of the entire network. Blockchain protocols thus ensure that transactions on a blockchain are valid and never recorded to the shared repository more than once, enabling people to coordinate individual transactions in a decentralized manner without the need to rely on a trusted authority to verify and clear all transactions. A blockchain is simply a chronological database of transactions recorded by a network of computers. Each blockchain is encrypted and organized into smaller datasets referred to as “blocks.”Every block contains information about a certain number of transactions, a reference to the preceding block in the blockchain, as well as an answer to a complex mathematical puzzle, which is used to validate the data associated with that block. A copy of the blockchain is stored on every computer in the network and these computers periodically synchronize to make sure that all of them have the same shared database. To ensure that only legitimate transactions are recorded into a blockchain, the network confirms that new transactions are valid and do not invalidate former transactions. A new block of data will be appended to the end of the blockchain only after the computers on the network reach consensus as to the validity of the transaction. Consensus within the network is achieved through different voting mechanisms, the most common of which is Proof of Work, which depends on the amount of processing power donated to the network. After a block has been added to the blockchain, it can no longer be deleted and the transactions it contains can be accessed and verified by everyone on the network. It becomes a permanent record that all of the computers on the network can use to coordinate an action or verify an event.

II. EMERGING USES OF BLOCKCHAIN TECHNOLOGY

Software developers have quickly realized the potential for blockchain technology and have started to use it to create digital currencies, self-executing smart contracts, as well as cryptographic tokens that can represent property or ownership interest in emerging services. It is also being used to create: censorship-resistant communications and file sharing systems; decentralized domain name management systems (DNS); and fraud-resistant digital voting platforms. Because the blockchain is a powerful decentralized database, the technology is increasingly recognized as a way to support machine-to-machine communications that will soon emerge from Internet enabled devices that constitute the Internet of Things. By combining digital currencies, smart contracts, and distributed data storage, the blockchain further is ushering in entirely new decentralized organizations (including decentralized autonomous organizations) that use source code to define an organization’s governance structure.

III. Digital Currencies and Global Payment Systems

One of the earliest applications for blockchain technology has been digital currencies such as Bitcoin. Released in 2009 by Satoshi Nakamoto (a pseudonymous individual or group), Bitcoin relies on a decentralized blockchain to establish a digital currency that, unlike the US dollar, does not depend on any bank or government. As explained by Nakamoto, the system is “completely decentralized, with no central server or trusted parties, because everything is based on crypto proof instead of trust.”Since its launch, Bitcoin has captured the world’s attention. Yet, Bitcoin is being used for more than just speculation. It is powering an entirely new payments system that allows for the seamless transfer of funds around the globe. Unlike existing payments systems, which generally take days to transfer funds, Bitcoin can be sent across the world in a little over seven minutes at fees that are drastically lower than those imposed by existing money transmitters, such as Western Union. All that is needed is an Internet connection and a computer or a simple mobile device. Adoption of Bitcoin has spread rapidly, and the currency—as well as its many imitators—have the potential to be the first breakthrough application that relies on blockchain technology. As noted by Stanford economist, Susan Athey, these digital currencies “can potentially expand international commerce, support financial inclusion, and transform how we shop, save and do business in ways we probably cannot even yet fully understand.”It can lead to faster, cheaper bank transfers, unleash banking and e-commerce functions to third world countries, expand global remittances, and drastically reduce merchant fraud.

IV. Smart Contracts and Automated Transactions

Blockchains are not just powering digital currencies. They are also enabling the creation smart contracts, one of the first truly disruptive technological advancements to the practice of law since the invention of the printing press. Using a distributed database, like the blockchain, parties can confirm that an event or condition has in fact occurred without the need for a third party. As a result, the technology has breathed life into a theoretical concept first formulated in 1997: digital, computable contracts where the performance and enforcement of contractual conditions occur automatically, without the need for human intervention. In some cases, smart contracts represent the implementation of a contractual agreement, whose legal provisions have been formalized into source code. Contracting parties can thus structure their relationships more efficiently, in a self-executing manner and without the ambiguity of words.Reliance on source code enables willing parties to model contractual performance and simulate the agreement’s performance before execution. In other cases, smart contracts introduce new codified relationships that are both defined and automatically enforced by code, but which are not linked to any underlying contractual rights or obligations. To the extent that a blockchain allows for the implementation of self-executing transactions, parties can freely transact with one another, without the technical need to enter into a standard contractual arrangement. To date, smart contracts have mostly been created to automatically execute derivatives, futures, swaps, and options. Yet, they are also being used to facilitate the sale of goods between unrelated people on the Internet without the need for a centralized organization. The development of smart contracts is expanding rapidly. Over the past several months, a number of open source projects—such as Ethereum, Counterparty, and Mastercoin—have been developed to create programming languages that enable the creation of increasingly sophisticated smart contracts. Using these programming languages, smart contracts could be used to enable employees to be paid on an hourly or daily basis with taxes remitted to a governmental body in real time. The technology could be employed to create smart contracts that automatically check state death registries and allocate assets from a testator’s estate, send applicable taxes to governmental agencies without the need of administering the will through probate. Music royalties could be administered instantaneously, with distributions provided to both composers and performers in real time. Complicated securitization could, similarly, be transformed into a smart contract, eliminating the technical need for trustees and servicers.

V. Distributed and Secure Data Stores

Because it is an encrypted and decentralized database, blockchains are also beginning to impact how we communicate and share data online. Not only are they changing the way the Internet is managed, they are also increasingly seen as a way to facilitate machine-to-machine communications of Internet-enabled devices. Thanks to the blockchain, it is no longer necessary to route communications or files through a centralized system or online platform (like Gmail for e-mails or Dropbox for the exchange of digital files). Using decentralized, encrypted communication protocols and a blockchain, parties can store and retrieve messages without the risk of government intervention. This same technology also allows for the exchange of data in a way that is both decentralized and secure. Information can be published (in encrypted format, if necessary) and distributed across hundreds of thousands of computers, making it virtually impossible for any single entity to censor. Early examples include anonymous decentralized cloud storage systems that use blockchain technology and other peer-to-peer technology to encourage people to use excess capacity on their hard drives. From the user’s perspective, these powerful platforms look similar to popular centralized cloud computing platforms. However, on a technological level, they operate completely differently. In these systems, users are awarded a digital currency for storing other people’s data, which users in turn can use to pay for storage of their own data on other users computers. Because of this incentive system, people who use these services are encouraged to rent out their own hard-drives, so they can gain access to the collective hard- drive of the network. By design, the decentralized, encrypted nature of these platforms makes them seemingly censor proof—no centralized organization is technically able to view the content of any file on the network or stop its transmission.Beyond managing data, software developers are exploring the blockchain’s potential to enable unrelated people to securely vote over the Internet or on a mobile device. A blockchain can serve as a distributed, irreversible, and encrypted public paper trail that can be easily audited. Voters could verify that their own votes were counted, and—due to encryption—any blockchain-based voting system would be resistant to hacking. Elections and proxy fights would no longer need to rely on the fallibility of paper and hanging chads. They could be safely waged on mobile devices. Decentralizing data stores, like the blockchain, are further seen as a technical replacement for the domain name registry system that underpins the entire Internet. Currently, domain names—such as Google.com and Facebook.com—are managed through the Internet Corporation for Assigned Names and Numbers (ICANN), an international organization charged with maintaining how people access Internet sites. New blockchain based applications seeks to upend this order, by creating a distributed domain name registry system that would store lists of domain names on a distributed blockchain database, without having to go through governments and large corporations to route traffic. With just a single digital currency transaction, worth several pennies, a blockchain can extend our existing DNS system in a way that is censor-resistant and more secure. A blockchain’s ability to manage data from a variety of untrusted source may further make it a foundational tool for the mainstream deployment of the Internet of Things. The Internet of Things will consist of billions of networked Internet-enabled devices, not all of which can be trusted and some of which may even be malicious. These devices need a central reference point that can help facilitate private, secure, and trustless machine-to-machine coordination. For this problem, the blockchain offers an elegant solution. Devices and other tangible property can be registered onto a blockchain and turned into smart property, using smart contracts described above, allowing tangible property to be controlled over the Internet and even controlled by other machines. A blockchain can store the relationship between Internet-enabled machines at any given moment, and smart contracts can allocate corresponding rights and obligations of connected devices. What’s more, different relationships and credential could be encoded into the blockchain with regard to certain cryptographically activated assets (such as key locks or smartphones) so as to ensure that only certain people have access to the property’s features at any given time.

VI. Decentralized (Autonomous) Organisation

A blockchain’s coordinative power is not solely limited to facilitating the action of machines. It also allows for the execution and interconnection of a variety of smart contracts that interact with one another in a decentralized and distributed manner. Multiple smart contracts can be bound together to form decentralized organizations that operate according to specific rules and procedures defined by smart contracts and code — thereby transforming Michael Jensen’s and William Meckling’s theory that entities are nothing more than a collection of contracts and relationships into reality. Using a blockchain-based decentralized organization, people and machines (or a combination of both) can coordinate through a set of codified smart contracts, without the need to incorporate into traditional business entities. Governance can be achieved by recording transactions directly to a blockchain, reducing operational costs, while providing a more transparent and audit-able trails of every decision. Corporate governance models can be replicated by distributing decision-making power to multiple parties using multiple signature (multi-sig) technology, which prevents the execution of an action until multiple parties agree to a transaction. As opposed to traditional organizations, where decision-making is concentrated at the top (i.e., at the executive level), the decision-making process of a decentralized organization can be encoded directly into source code. Shareholders can participate in decision-making through decentralized voting, distributing authority throughout the organization without the need for any trusted centralized party. By facilitating coordination and trust, a blockchain enables new forms of collective action that have the potential to bypass existing governance failures. It can thus potentially resolve many of the common problems related to the opacity and corruption inherent in the decision- making of many organizations. Large hierarchical organizations are both imperfect and inefficient. Their imperfections are, for the most part, due to excessive centralization, delegated decision-making, regulatory capture, and sometimes even corruption. With the blockchain, most of these imperfections could evaporate. Interactions and organizations can be predefined by smart contract, and people or machines can interact without having to trust the other party. Trust does not rest with the organization, but rather within the security and audit-ability of the underlying code, whose operations can be scrutinized by millions of eyes. In that sense, decentralized organizations can be thought of as open-sourced organizations. Over time, as Internet-enabled devices become more autonomous, these machines can use decentralized organizations and the blockchain to coordinate their interactions with the outside world. We could thus witness the emergence of decentralized autonomous organizations that enter into contractual relationships with individuals or other machines in order to create a complex ecosystem of autonomous agents interacting with one another according to a set of pre-determined, hard-wired, and self-enforcing rules. Decentralized autonomous organizations are a specific kind of decentralized organization that are both autonomous (in the sense that, after they have been deployed on the blockchain, they no longer need nor heed their creators) and self-sufficient (in the sense that they can accumulate capital, such as digital currencies or physical assets). Decentralized autonomous organizations can charge users for the services they provide, in order to pay others for the resources they need. As long as they receive sufficient funds to operate on their own, they can thus subsist independently of any third party. If a decentralized organization is truly autonomous, no one (including its original creator) can control it after it has been deployed on the blockchain. An ill-intentioned decentralized autonomous organization thus could be akin to a biological virus or an uncontrollable force of nature.

2 The Rise Of Concierge Coin - Decentralized Ledger Technology

The CGE decentralized ledger is the system that regulates all transactions and relationships between the consumers and vendors. The rules and operations are governed by smart contracts which will be deployed with EVM (Ethereum Virtual Machine). The ledger will be open sources and free to use and will regulate and store all the transaction execution data via smart contract triggers. We will endorse developers to further advance upon the ledger in aid of strengthening the new world standard for booking anything within travel based on the native CGE token. By incorporating more travel platforms to the CGE engine it will in turn increase use of the CGE token increasing its value.

The CGE ledger will run in accordance and native to the CGE token and any application which wants to connect, they will have freedom to bring added value services via support of additional payment methods which they can convert into CGE at the time of booking. This could be achieved through either converting currencies themselves with an internal algorithm or integration to external exchanges.

Operations of the decentralized CGE ledger will be as followed (This shows some however is not limited to):

Booking placement

Booking confirmation policy

Check-in requirements & upgrade possibilities

Deposit holding

Deposit withholding

Deposit release/refunding upon check-out

Dispute trigger & dispute terms

Optional history/reputation requirement for consumer

User review (Both consumer & vendor)

The CGE ledger will provide a completely new backend booking system, that we believe is essential in development into the fully integrated and operational decentralized application and web platform.

This way the decentralized CGE Ledger in amalgamation with the user-friendly application/web platform will create an ecosystem that will be self-sufficient. Not relying on any external factors is of supreme importance for the success of the project and the token distribution event.

For this purpose, we are planning to build the CGE ledger together with the Concierge web-based platform, integrating both the app and web-platform together working coherently as the go to marketplace.

The app and web-platform will serve as a proof of concept, for anyone who takes part in the token distribution events being able to spend their CGE. However, upon coin release all token holders

will receive a % on each transaction of coin trades. The Coin will also then become currency accepted across the Concierge platforms.

Source: DECENTRALIZED BLOCKCHAIN TECHNOLOGY AND THE RISE OF LEX CRYPTOGRAPHIA Aaron Wright & Primavera De Filippi