2018: The Year of the Mega Cap ICO?

Why Block Chain May Lead to More, Not Less Centralization

In his novel, Snow Crash, Neal Stephenson, paints the picture of a dystopian future in which the line between public and private has been entirely removed giving rise to “Franchises”. Franchises are both privatized nation-states and corporations imbued with governmental powers. These Franchises, like Mr. Lee’s Greater Hong Kong and the CIC (the for-profit organization that evolved from the CIA’s merger with the Library of Congress), rule the land, having supplanted the nation-state as we know it.

We are not far removed from this future. I believe that very soon we will see the complete destruction of the line that once separated public from private. Global corporations like the tech giants Facebook, Amazon, Microsoft, Google and Apple (collectively, FAMGA), have already begun to evolve into Franchises, or supranational economies. Ultimately these Franchises will issue their own currencies, thus increasing their share and control of the global political economy.

Block chain, the technology that many believe will lead us to a golden age of decentralization, will potentially be the tool used to drive further consolidation.

The Blurred Line: What is Private? What is Public?

The privatization of government institutions has been on the rise for decades.

In countries like Russia and China, the elite political class control both major corporations and government institutions. China’s state-owned enterprises, or SEOs, employee 40 million individuals including ten million Chinese Communist Party members. These entities account for over 60% of China’s outbound investment. It is no secret that Russia’s oligarchs control both the government and the economy through their own form of chrony-capitalism, but now they also hold large investments in major US-corporations. On a smaller scale, private city-states like Singapore, operate more like corporations than nations and have done so for decades.

But one need not look overseas to find the trend towards privatization. This has been on the rise in the United States as well. Revolving door policies allow members of key governmental institutions to freely move between the private and public sectors. Supreme Court cases like Citizens United have enabled and exacerbated corporate interference in government affairs.

History is littered with warnings of this trend (see Manufacturing Consent or Eisenhower’s “Military Industrial Complex”), but the trend is accelerating and producing new iterations.

In Saudi Arabia, the Crown Prince Mohammed bin Salman recently unveiled plans to build a new city, NEOM, which will operate independently from the “existing governmental framework”. Here in the US, Bill Gates invested $80 million to build a private smart-city in Arizona. In the wake of Hurricane Maria, Elon Musk is negotiating with Puerto Rican officials for Tesla to rebuild the US territory’s power grid. Finally, a number of cities vying for Amazon’s HQ2 have offered the company decision making power over the spending of its tax revenue.

What was once public domain: the creation and operation of cities and key utilities, now belongs to private individuals and institutions.

Corporate Evolution: Application→Platform→Economy

Over the last decade, the reorganization of the private sector has been defined by the growth of tech giants like FAMGA from applications (ie: Amazon books, Facebook profiles, and Google search) to platforms. The internet was initially hailed as a catalyst for decentralization; however, the last ten years have been defined by the centralization of wealth and power into a handful of these platforms.

Since the mid-2000s, there has been a corporate land grab or “platform war” as Executive Chairman of Alphabet Inc, Eric Schmidt, once described it. Multi-national tech giants have been acquiring as many companies as quickly as possible. Google alone holds investments in 25 unicorns (companies valued over $1 billion), according to a June 2017 CBI Insights report. In the past, creative destruction from new innovations would dethrone incumbent corporate giants, but today the incumbents simply acquire would-be competitors — “If you can’t beat ‘em, buy ‘em.”

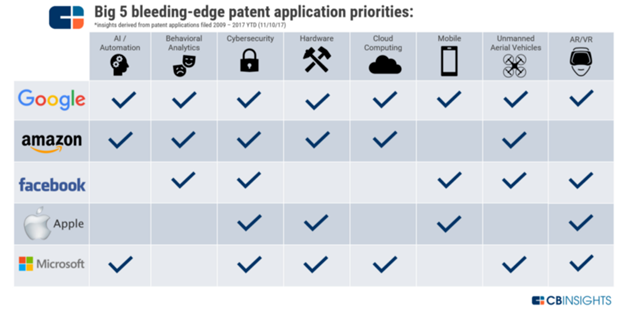

FAMGA owns assets across multiple industries including AI, retail, data storage, autonomous vehicles, original content, and even space exploration. The below chart details FAMGA’s recent patent applications by industry.

These entities have grown so large, diversified, and powerful that “platform” is no longer a suitable term to describe them. They have evolved into something more like Stephenson’s Franchises — supranational economies with little need for the institutions of the host countries within which they operate.

Every economy in its simplest form is a network of exchange and within an economy the medium of exchange is its currency. As it stands, FAMGA and other tech giants, remain dependent upon the currencies of nation-states like the US. As a result, these behemoths are not 100% in control of their own destinies; they each have a stake in the fate of their host country, its institutions, and the value of its currency. Therefore they spend millions annually to affect public policy.

In the near future, these companies will expand well beyond the need for their host countries, ultimately supplanting the power of existing nation-states. The technology that will enable this tectonic shift is the block chain.

Block chain technology will remove these Franchise’s dependence on nation-states as we know them.

Bitcoin, Ethereum, and the Rise of Block Chain Technology

In Snow Crash, hyperinflation has eliminated the viability of the US dollar as a medium for exchange. Now, instead of using the once mighty buck, individuals exchange electronic currency via encrypted online transactions.

Though hyperinflation has not yet hit the USD, Stephenson was correct in predicting the creation and adoption of global, digital, “cryptocurrencies”. In May 2007, using lessons from a number of experimental cryptocurrencies like Digicash, Bitgold, and Hashcash, that had either failed or failed to launch, a developer named Satoshi Nakomoto began programming Bitcoin. He released a white paper on the currency in October 2008.

Though Nakomoto’s identity still remains a mystery, “his” creation, Bitcoin, has emerged as the leading cryptocurrency in the world both by market capitalization (now surpassing $150 billion) and adoption (Coinbase estimated 14 million Bitcoin wallets in 2016). As of the writing of this post, the USD price of one Bitcoin exceeded $10,000, making Bitcoin a top 30 global currency by market capitalization.

One key to Bitcoin’s success lies in its underlying technology: the block chain. The block chain is a decentralized, append-only ledger. This ledger contains all past Bitcoin transactions and can be viewed by all participants in the Bitcoin network. Once a transaction has been confirmed, it cannot be changed. Thousands of individuals or “nodes” monitor this ledger, and if there were ever an attack on the system, these nodes would recognize it as such and act by ignoring & essentially removing any corrupted block from the chain.

CBI Insights describes a simple Bitcoin transaction graphically and in more detail.

Though past transactions cannot be changed, this technology might have already changed everything.

The durability and success of Bitcoin has encouraged the rise of other cryptocurrencies like Litecoin, Dash, & IOTA. But the most important innovation in the cryptocurrency market since Bitcoin has been Ethereum. More than just a currency, Ethereum is a Turing-complete platform on which new decentralized applications, or “Dapps”, can be built. Basically any program can be written on top of the Ethereum network.

According to Linda Xie, former product manager at Coinbase, Ethereum is different than Bitcoin in that it allows for smart contracts. or “highly programmable digital money.”

There are many use cases for Dapps including shared computing power (Filecoin), social media (Akasha), entertainment rights management (SingularDTV), and entirely decentralized exchanges (Airswap).

However, the most prevalent use case for a Dapp to date has been for fundraising via an Initial Coin Offering, (also known as an ICO or token sale).

What is an ICO & What is a Token?

An ICO is essentially a new take on crowdfunding. Rather than raising capital from traditional investors like venture capital funds, companies can go directly to the individuals who will use their product or application. In exchange for major cryptocurrency like Bitcoin or Ethereum, these companies issue their own tokens.

According to Fred Ersham, the co-founder of Coinbase, Tokens have the following characteristics (full post here):

- They are the currency that is used in the app itself.

- Contributors to the app are directly paid for their contributions in tokens.

- The tokens are easily converted to any local currency since they are on the block chain.

These are important points. By issuing a token, a company becomes more than just a business, it becomes an economic system. In each economy, the currency (or token) is the company’s product/application.

The key stakeholders in the economy are the company and the token holders. In a traditional business model, one would think of the token holders as the company’s customers, but now they are essentially “citizens” of the token’s economy. These “citizens” have a vested economic interest in the performance and adoption of their cryptocurrency.

Why ICO?

There are many benefits to raising capital via an ICO versus traditional financing sources.

For starters, companies have been able to raise more capital earlier: in 2017 the average ICO exceeded the average Series A funding round.

Chart from Tomasz Tunguz @ Redpoint

The above chart may even understate the rewards of an ICO versus traditional fundraising. Many ICOs are issued by companies without a proven application with user adoption; thus the better ICO comparison would be to Seed financing rounds, which are an order of magnitude smaller than Series A.

Not only have companies been able to raise more capital, but the capital is non-dilutive. ICO investors will not receive shares in the issuing company, therefore owners retain one hundred percent of future profits.

Finally, there are positive network effects. If a company proves its token to be a useful application, it can generate wide user adoption. As adoption increases, more users enter the network and demand for the token rises. In economic systems, when finite supply meets rising demand, the price increases. Mass adoption leads to price appreciation of the token and all citizens of the economy are rewarded.

The ICO Market — A Useless Boom?

The ICO market has seen tremendous growth in the last year. As of November 6, 130 ICOs have raised over $3 billion — 18 have raised more than $100m. There are now over 1,000 ICOs listed on Tokendata.io.

The problem; however, is that not every business should be its own economic system and not every application its own currency.

To date, most ICOs have successfully raised capital, but have been unsuccessful in proving the utility of the underlying tokens. In fact, only 10% of tokens issued in 2017 are currently being used for their stated application; the rest are used purely for speculative purposes.

Currencies need to exist within a large enough economy to survive. Therefore many tokens will fade away and be replaced by cryptocurrencies with a larger market capitalization. There will be a handful of winners and many losers. Though the application underlying the token may still be useful, transactions will be denominated in a more widely used cryptocurrency.

The only way for a company to survive independently will be to scale its own economy extremely quickly or to join another. Useful token-issuing companies will be absorbed into larger crypto-economies as the current trend towards thousands of smaller decentralized economic systems will reverse towards consolidation within a handful larger networks.

The Mega Cap ICO

It is likely that these larger networks will be created and managed by companies like FAMGA. Unlike most token issuers in 2017, FAMGA have already built the network effects of a successful economy. More than just companies, these are Franchises — the only piece missing is their own currencies.

Just as Snow Crash’s Mr. Lee’s Greater Hong Kong had its own currency, “Kongbucks”, I believe FAMGA will soon issue their own tokens.

Many of the previously described benefits of issuing a token will be even more valuable to companies like FAMGA. These include:

More non-dilutive financial capital — each member of FAMGA has the potential to raise billions of dollars through its own ICO. This capital could be used for further acquisitions and to fund newer, long-term initiatives like Blue Origin @ Amazon.

Improved customer retention — Early currency adopters, now citizens of the economy, will be rewarded for owning and using the currency both through incentives (like free shipping for Amazon Prime members) and the appreciation of the currency itself.

Increased returns from token appreciation — it’s likely that should the members of FAMGA issue their own currencies, these currencies would appreciate against the USD over time. As the largest holders of their own currencies, these entities would reap the financial rewards.

Less costly employee incentives — rather than issuing dilutive stock options, companies can now reward employees by minting new currency, which will ultimately remain in the economy and build further positive network effects.

Diminished risk of onerous cross-border taxes — Tax law related to cryptocurrencies is rapidly evolving. The current landscape is so grey that a company like Apple might be able to convert its “cash mountain” into its own token, AppleCoin, then hold & use those tokens within its own private economy without a tax effect.

Decreased financial dependence on systemically damaged, unstable public institutions — Though they operate globally, many of these companies are based in the US. If US hegemony is on the decline, these entities currently face outsized risk from uncertain public policy decisions.

More control of their own destinies — tokens will create network effects that reward quality decision making, and will limit the effects of public policy decisions made by policymakers outside of a Mega Cap’s token economy.

Just as the mid-2000s were defined by the Mega Cap LBO, the remainder of this decade will be defined by the Mega Cap ICO.

An Interesting Case Study

This fall, a potential case study for the Mega Cap ICO, WAX, was launched by the creators of OPSkins (Disclosure: as of the writing of this post, I own WAX tokens). While OPSkins is nowhere near the size of the aforementioned tech giants, WAX is one of the first tokens issued by a previously existing, large scale enterprise.

OPSkins is self-described as “the largest platform for video game virtual goods.” On exchanges like OPSkins and those of its competitors, gamers can exchange virtual assets like “skins” or customized weapons. According to OPSkins, this is a $50Bn market that already includes over 400 million gamers — OPSkins itself registers around 200,000 new users each month.

The “citizens”in the WAX economy are gamers who have a clear use case for the application that WAX provides — buying virtual goods. They already use similar applications that have not yet been tokenized. If WAX is successful, early adopters will be rewarded via token appreciation as more “citizens” join the WAX economy.

While it is a fascinating case study, I do not believe that the success or failure of the WAX ICO will predict that of an ICO issued by FAMGA. After all, Facebook alone has over 2 billion users worldwide. This is 5x the size of the entire virtual goods market and therefore a FacebookCoin should arguably have stronger network effects than those of WAX.

Where Do We Go From Here?

It seems likely that the first US-based Mega Cap ICO will be issued by Amazon in 2018. In fact, there are already rumors stirring that Amazon will issue its own cryptocurrency. The rest of FAMGA will watch this ICO closely, and if it proves successful, they will follow quickly behind.

The world of Stephenson’s Snow Crash, or some iteration thereof, is upon us. The explosive growth of cryptocurrencies, the massive consolidation of technology into the hands of a few giants, and the blurred line between public & private institutions are all important elements that led us to this moment.

While we are currently experiencing a shift towards decentralization evidenced by the recent wave of ICOs, the market will likely only reward a handful of winners via the adoption of their tokens. If Franchises like FAMGA decide to enter the ICO market, they can consolidate power within their own economies, as they have already done with the Internet.

The effects of this sea change in the structure of our global political economy will be both far reaching and unpredictable. Yet, I believe that the trend will be towards more centralization and not less.

Congratulations @warcmeinstein! You have completed some achievement on Steemit and have been rewarded with new badge(s) :

Click on any badge to view your own Board of Honor on SteemitBoard.

For more information about SteemitBoard, click here

If you no longer want to receive notifications, reply to this comment with the word

STOPCongratulations @warcmeinstein! You received a personal award!

Click here to view your Board

Congratulations @warcmeinstein! You received a personal award!

You can view your badges on your Steem Board and compare to others on the Steem Ranking

Vote for @Steemitboard as a witness to get one more award and increased upvotes!