Review: Ether (ETH) Bearish Thesis: The “Flippening” of Market Irrationality

Below is my summary of the 41-page Ethereum market analysis by Tetras Capital entitled Ether (ETH) Bearish Thesis: The “Flippening” of Market Irrationality .

I recommend this deeply through-through article to anyone who is either holding a substantial position in altcoins or generally aims to better understand the inner makings of the crypto markets.

All the points below have been copy/pasted directly from the above article:

We believe that ETH’s current price is still significantly overvalued; still significantly decoupled from the Ethereum network’s current and near-term technological state. Our research has led us to believe that the market and technology is still far too immature to justify current valuations.

While Ethereum’s current “brand name” edge may continue for some time, it has yet to solidify any functional competitive advantages.

Tokens are money, not equity – and thus will accrue value in an entirely different manner.

A blockchain’s architectural decentralization stems from the ease of running a full node3.

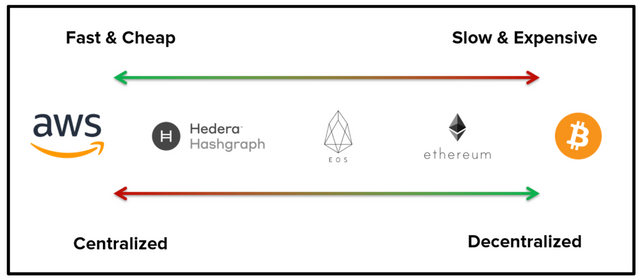

Ethereum is now stuck in a middle ground, where it cannot be as decentralized as Bitcoin and it cannot be as seamless and low cost as AWS (or even the other more centralized blockchain-based alternatives).

EOS threw out the entire Bitcoin ethos that Ethereum attempted to preserve by (1) removing transaction fees entirely, (2) paying block producers with a potentially infinite token supply schedule, and (3) limiting the validating nodes to 21 supercomputers. This dramatically increases the transaction throughput. We do not think this is a long-term winning strategy, but in the near-term it can deplete significant market share from Ethereum.

Additionally, if Ethereum becomes effectively architecturally centralized, it is no longer just competing with Bitcoin and other crypto-assets, but also AWS and Azure which are cheap to use, scalable, more secure, better developed, etc., and already have a robust competitive moat.

We believe that Bitcoin is the paragon of maximizing political decentralization for a cryptocurrency.

The DAO hard fork was two years ago and not a lot has changed. Vitalik and the Ethereum Foundation are still driving large updates in the network, and they have proposed substantial changes to the infrastructure and consensus rules (i.e. Sharding and Casper/PoS) with virtually zero pushback. It is clear that Vitalik is the de facto CEO of Ethereum.

It is now indisputable that if a public ICO occurs “pre-product” then there is a required “effort of others” – which makes it a security under the Howey Test.

Ethereum is simply unnecessarily complicated for ICO purposes and Ethereum’s richly stateful Turing-Complete contracts have led to a myriad of bugs and other security failures (recall The DAO and the roughly $300 million Parity multi-sig exploit).

It is clear that Ethereum’s highest and arguably only real source of demand right now is as a capital raising platform. This demand continuing is strongly predicated on regulatory agencies ignoring the mania and investors remaining very risk-on.

Comparing AWS to Filecoin illustrates an important difference between money and equity. […] Pretending that stock in AWS exists, investors are incentivized to hold AWS stock if (a) AWS is profitable and/or (b) they expect an increase in AWS use and subsequently revenue/profit to grow.

There is no direct mechanism that links Filecoin network use to FIL price like AWS use is linked to its share price (through cash flow).

Usage alone will not be enough to support a trillion-dollar valuation because it will be possible to use a protocol without holding the asset across time.

To justify valuations north of $100 billion, crypto-assets need to be on a path to become a store of value. Definitionally, this is the case. If the bet is that (an unpegged) crypto-asset becomes worth $10 trillion, you are betting that $10 trillion in wealth will be held in it eventually.

ETH Cannot Outcompete BTC Directly as Digital Gold. Bitcoin not only has stronger SoV properties, but it also has a six-year head start, greater security, and more liquidity13.

Even if ETH economic activity doubled each year for 10 years – ultimately yielding a 1000-fold increase at a velocity of 7 (roughly M2’s) – ETH would be worth $52 billion in 10 years. That’s only about 15% more than its current market cap of $45 billion, even with very conservative velocity assumptions. It should be clear, if not alarming, why ETH needs to become a SoV.

We are at the precipice of veteran institutional capital entering the market, and this capital will see through the mania. They may not shun platforms like Ethereum entirely, but given their understanding of currencies within macroeconomic systems and the robustness of the BTC investment ecosystem (futures, increased liquidity, etc), we believe they will be overweight BTC relative to ETH.

Bitcoin Will Lead the Next Sustained Crypto-Asset Bull Market

Well detailed and explained 👍