Payment habits, Dematerialization, Rise of Cryptocurrencies, Usage of Cash: Is the European General Public Ready for the Evolution of Money?

State of the market in the world

Cryptocurrencies are more and more popular. Since a few months, we see more and more subjects about Bitcoin and the blockchain in the mainstream medias. We also see more and more people talking about Ethereum and altcoins on the Internet. However, only a few people use Bitcoin and other cryptocurrencies for payment, saving or speculation. Currently, you can pay in bitcoins on a few websites, and in some bars and restaurants. But for most of the stores, you still need cash or regular credit cards. The reasons are quite obvious: misinformation, a certain lack of interest and mistrust. Why ? It's simple...

- Bitcoin and cryptocurrencies are quite a novelty for the general public and retailers. Virtual coins are not knownn well enough.

- Cryptocurrencies still have a bad reputation for a part of the general public. Cryptocoins are often associated with darknet markets and illegal stuff.

- There are only a few places where you can use Bitcoin or other cryptocurrencies.

- The main cryptocurrencies are not recognized as "real" currencies, so people are reluctant to use it. If people don't trust an alternative payment method, they don't give it a real value. Currently, virtual coins are appreciated and used mostly by enthusiasts. Lots of people think Bitcoin is just for geeks, nerds, drug addicts and dealers.

A "physical" Bitcoin coin - Pixabay

The Euro, the other European currencies, and the cryptocurrencies

Picture of a European flag, by GregMontani - Pixabay

Currently, the European Union counts 28 member states. Amongst them, 19 are part of the Euro zone. These 19 countries use the same currency, the Euro, while the others still have their national currencies. The EU's 28 members are subject to the same European laws and regulations, but they don't have the same monetary system. Though, they have common monetary institutions, such as the European Central Bank (ECB) for the eurozone and the European System of Central Banks (ESCB) for the whole EU.

The European Central Bank in Frankfurt - Picture from Pixabay

A Euro coin

Map of the eurozone. Credits: EU official website.

The 19 countries of the eurozone have a common currency, but different economies.

- Sectors. They don't have the same repartition by sectors. Germany still has a strong industry while Luxembourg is more centered on financial services.

- Different GDP by capita.

- Social regulation. The level of social protection is far different from a country to another. In 2016, social spendings represent(ed) 31.5% of GDP in France, 30.8% in Finland, 29% in Belgium, 28.9% in Italy, but only 16.1% in Ireland and 14.5% in Latvia.

- Taxation levels. We have higher public spendings, you generally have higher taxes. In France and Belgium, the corporate tax rate is around 33-34%. In Ireland, it's 25% for non-trading income. In Latvia, the corporate tax rate is only at 15%.

All these factors make significative differences between the economies of the eurozone. They have different economies, different public spendings level, and different tax rates. The euro is a problem for several countries of the eurozone. It affects their competitiveness. If they are less competitive, they have to find a mean or another to reduce the cost of their products and services to regain competitiveness. If they can have a currency that fits their economies, they must adapt their economies to the currency. They try to reduce the labor cost, welfare, public employment and public investments. In the same time, with growing unemployment, the demand for unemployment benefits is growing too. Thus, these countries are led to the situation where they have to reduce spending while they have increasing needs for welfare. This is a complicated situation, right?

Photo credits: Endriago - Pixabay

From January to April 2016, the Greek tax authorities emptied 428,465 debtors bank accounts. When you are in a classic monetary system, your bank or the state has the possibility to pump money out of your account... and you have no real way to stop if it happens. You could say "just withdraw money from the banks and use cash". That's the first mean you would think about... So do the banks and the tax authorities. That's why they limited the amount you can withdraw each week in some EU countries. With cryptocurrencies, you don't have these restrictions. Thus, you can buy bitcoins and put them into a wallet, the bank won't be able to take them. Your banker will just know you send money to an exchange, no more. Your banker will not know which cryptocurrencies you bought or what is the value of what you have. That's why it's interesting to invest into cryptocurrencies in order to keep money out of the banking system while having an alternative payment method. This money will avoid fund seizure.

So, you have some reasons to use cryptos if you don't trust the banks and your government. But the distrust of banks is not enough for the general public. The European general public is still reluctant with cryptocurrencies because people have a lack of knowledge and are stuck in their habits. Payment habits are more or less an obstacle to mass adoption of cryptocurrencies.

Cultural differences across Europe

Across Europe, people have different currencies, different taxes, different wages, different consumer prices and different payment habits. We can observe these differences across Europe. People don't have the same relation to banks, cash, credit cards and digital payments from a country to another.

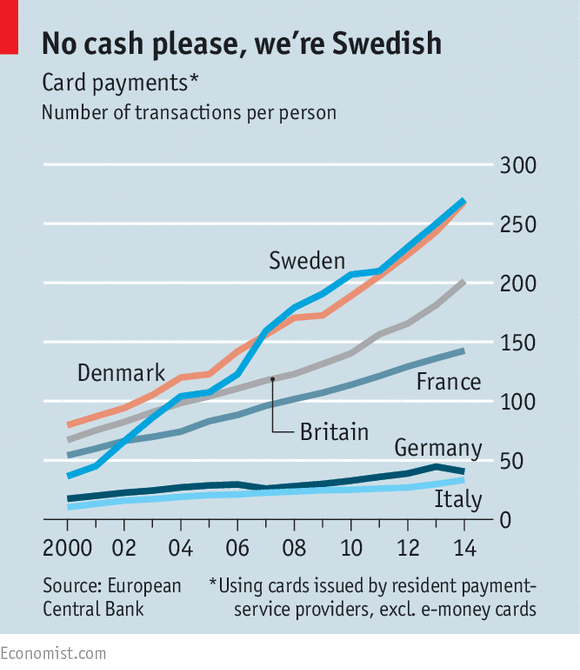

Sweden: soon a cashless country? Are Denmark and Norway going to follow?

Apparently, the Swedes don't use a lot of cash: most of the payments in local are done with credit and debit cards or even mobile devices. Currentyl, cash represents only 20% of the payments. Even with street vendors, you don't need coins or money bills to pay something. Credit cards are accepted almost everywhere. With a great support for non-physical transactions, Sweden could become the first cashless country in Europe in a few years...

Picture of a Swedish flag, by Picudio - Pixabay

According to the European Central Bank, the Swedes and the Danish are the biggest users of credit cards transactions within the EU.

In Norway (which is not an EU member state), Den Norske Bank (DnB NOR), the second largest bank in the country, called in 2016 for a total ban of cash. The Ministry of Finances rejected this proposal. The main argument of DnB NOR was simple: according to its executive vice president, 60 % of the money in Norway is used out of the banks, so this money is "out of control". What does it mean? That means that the Norwegian banks would like to control more than 40 % of the money used in the country. They don't like cash because they can't control it so easily than credit cards and bank accounts.

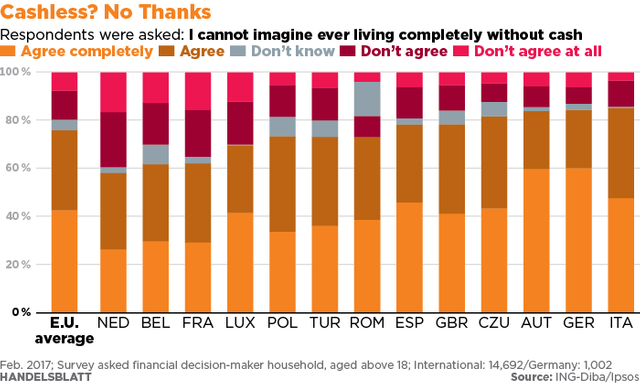

Germany: Bargeld über alles

Sweden is enthusiasts about dematerialized payments. On the contrary, in Germany, people like coins and bills. In several European countries, people use cash for payments of less of €10. In Germany, more people use cash for larger purchases. Almost 80% of all payments are done with cash. Why do they prefer this instead of modern payment methods? There are a few explanations.

Picture from Pixabay.com

Firstly: the fees. Having and using a credit card can be more expensive than in some other European countries. Having a payment terminal is also more expensive for retailers, bars, and restaurants. So, using cash instead of credit cards seems to be less expensive.

Secondly: privacy. When you use a credit card in a store, your bank knows it. When you withdraw money on an ATM, your bank doesn't know what you do with your money. Cash is not so easy to trace.

Thirdly: cultural context. In Germany, having 100 euros in your wallet is a common habit. The 100 and 200 euro bank notes are more common in Germany than in other countries. These banknotes are quite rare in most of the countries within the Eurozone, because they are not available on most of the ATMs. So, in these countries, if you want to pay something expensive with a 100 euro or a 200 euro note, it is often considered as a strange thing. If you want to use a 500 note, people will think you are either a millionaire or a thug. In Germany, people are not so suspicious with big bank notes, because they are more common and more widely accepted.

In Europe, the Germans and their Austrian neighbors are strongly opposed to a disappearance of cash.

So, the Germans and the Swedes have very different habits. The Swedes trust modern payment method, whereas the Germans still rely on cash. The Swedes want something practical, whereas the Germans want privacy and fewer fees as possible.

Picture of a German €1 coin, by moritz320 - Pixabay

The advantages and disadvantages of cryptocurrencies over cash and credit cards

Cryptocurrencies have serious assets to offer.

Quickness. An international bank transfer can take several days. With cryptocurrencies, it takes only a few seconds or a few minutes.

Cost: low fees, especially compared to international bank transfer.

Independence. Cryptocurrencies are not regulated by the states and the central banks. When you have a regular national currency, the national central bank can decide to devaluate it or to produce more money. With Bitcoin, Litecoin, Ethereum and most of the altcoins, no central bank, no central authority, no borders. These are good examples of decentralization.

Security.

Privacy. With cryptocurrencies, when you send money to another person, you only send money from an address to another, there is no name directly associated with your address. You can send money to a friend, and your bank won't know it. Virtual wallets are also a good mean to keep money out of the banking system.

However, there are also some disadvantages.

Low acceptance by retailers. Though there are more and more online and physical stores accepting Bitcoin, they are located mainly in Asia. Moreover, only a few European stores know and use Bitcoin. When the level of acceptance is low, people are less eager to shift their habits.

Slowness. When a network is saturated as this is the case with Bitcoin, transactions take more time to be treated. Sometimes, transactions can take several hours to proceed, whereas it takes only a few minutes in normal time.

Increasing cost. When a network is saturated, it also has an effect on the fees. The big transactions are treated in priority, while the small ones are treated next. With the small transactions, you have longest treatment time and proportionally highest fees.

Not so independent... Most of the cryptocurrencies are theoretically independent from banks and states. Nevertheless, some banks are interested in the blockchain. For instance, UniCredit, UBS, Santander and The Bank of Tokyo-Mitsubishi support Ripple. JPMorgan support Zcash.

Security. The blockchain improves the security of transactions. But what about the services related to cryptocurrencies? They still can be hacked. In 2013, when MtGox was hacked, the Bitcoin price fell from an all time high of $1163 to only $387. In 2016, when The DAO was hacked, 3.6 million Ether (53 millions $ at the time) were stolen. More recently,

Not so confidential. When you want to use a trading platform or to pay legal services with cryptocurrencies, you often have to use a real name on this platforms. So, an anonymous address could be indirectly associated with a name and an amount of money.

Volatility. "Buy low, sell high". If you're trading cryptocurrencies, you probably know this proverb. We are currently in a period of doubt and uncertainty. The prices are going down. It seems we are in a bear market at the moment. Lots of investors and speculators are panicking and selling their coins.

Could the blockchain replace the banks? Could the cryptocurrencies replace cash?

Many cryptocurrency enthusiasts claim that the blockchain will replace the banks. They think that banks are obsolete and will disappear. I don't think so. I think the banks will evolve. They can see the blockchain as a potential threat to the banking system, but they can also see it as an asset. As you know, the blockchain is a decentralized system. It offers a greater security than other systems. It allows faster international transactions. That's why some major banks invested in blockchain systems, such as Ripple. In Japan, tens and tens of banks have joined the Ripple consortium, which they consider better than the SWIFT system. Meanwhile, in the United States, JPMorgan signed a partnership with the Zerocoin Electric Coin Company to integrate Zcash technology in Quorum. Big banks know they have to evolve and they know that the blockchain could be a big asset in order to reduce their costs, increase the security of transactions and deposits and gain rapidity.

Skyscrapers in the financial district of Frankfurt, Germany - Picture by Kallman, Pixabay

What about the use of cash? Some cryptocurrencies user think that cash will disappear in several developed countries in a few years. Some nonusers also think that virtual money could be a threat to cash. Is it realistic? According to the Swedish case, yes, or almost. Nowadays, in developed countries, you can not only pay with credit cards and debit cards, but also with NFC-enabled smartphones, PayPal or some mobile applications such as Google Wallet and Apple Pay, or other applications using QR codes... Even with credit cards and debit cards, we see a growing use of NFC technology for small amounts. For example, in France, if you want to buy a baguette, normal debit cards are generally refused by many bakeries, which demand cash under 5 or 10 euros because of the fees. Henceforth, more and more bakeries and small shops are accepting NFC cards... so more and more people are using contactless payments instead of cash. Contactless payment is also more and more used in public transports. In several major European cities, you can pay your ticket. People are using contactless payment because it's faster and more practical for them.

But there is another major question: is a cashless society a good thing? There are some arguments against cash.

Cash payments are slower than NFC and Bitcoin payments.

Coins and bank notes can be hidden, lost or stolen. Every year, millions of coins are lost (especially the small ones). Moreover, lots of people keep bank notes for years at home without using them. Thus, this money gets out of the economy, and the national central banks have to produce more bank notes.

Euro coins and notes are expensive to produce. In order to prevent counterfeiting, the euro bank notes require special paper, a precise weight, serial numbers, watermarks intaglio printing and security holograms with shifting colors. Producing a euro note with such technologies is more expensive than printing a simple paper note.

Fighting against fake notes is expensive for the authorities. It requires special police units to investigate, track and dismantle the makers of counterfeit euros. It also has a cost for shop owners when they are scammed with these fake notes. Some of them invested in fake money detectors, but it has a cost, and it takes more time when the customers are paying if you have to check every bank note. Furthermore, if you have to check every note, your customers will think you are suspicious of them...

"Big" bank notes are often used by drug dealers and criminal organizations. Cash is also used by tax evaders and money launderers. That is why European and national authorities established legal limits for cash payments. That's also why the ECB decided to stop the production of the 500 euro note.

Some countries in the world are becoming almost cashless. In some other countries, cash remains very usual for payments but is losing ground against dematerialized money.

You saw the common arguments for cash limitation. But there are some solid arguments for defending cash.

Cash is easy to use. Cash is accepted everywhere. If you don't have an NFC-enabled smartphone, if you don't have an NFC card, if you don't want to waste time using QR codes, cash is practical for the small transactions. If you want to give pocket money to your children, if you want to give money to a broke friend for lunch, if you want to give money to a homeless person or if you want to tip the pretty waitress in your favorite bar, cash is the easiest way. You don't need any intermediate between your wallet and the other person.

Cash payments are a good and simple training for using numbers. If you almost never use coins, it's probably because you're lazy with doing the simple math.

Cash is anonymous. When you withdraw cash, your bank knows it but doesn't know how this money is used. If you like privacy when you buy something in a store, cash is better than credit/debit cards and mobile applications. When you use non-anonymous electronic payment methods, you don't know if some of your personal data are sold to third-party companies that will send you personalized marketing.

Cash can be hidden. If you want to keep some money out of your bank account, cash is also the easiest way. If your account is overdrawn, depending on your bank and payment limit, you could be unable to transfer money or to pay with your card. Further to this, you can be charged with additional fees. If you have a low limitation on an overdrawn account, if you have some cash in reserve out of the bank, you're still able to buy things during the time you're waiting for your next salary. If your bank is going default, it will be able to seize money on your account, but it won't be able to seize the coins and notes you have out of your account.

You don't need electricity or a mobile device to use cash. You can give or receive cash from anybody without using any payment terminal or any mobile application.

A cashless society would give more power to the banks, and even to the states too. Banks would be able to charge more fees without good reasons, states would be able to impose more restrictive conditions on their citizens.

There are some disadvantages with cash, but there are some big advantages too, and some of them are common with cryptocurrencies. A cashless society would probably be less democratic and more expensive for everybody, especially for poor people. Keep using cash would mean allowing some illegal practices to continue, but the democratic and privacy stakes are more important. Cryptocurrencies and electronic payment means should not replace cash but should be complementary or alternative payment methods. Cryptocurrencies will gain market shares, but we must not abandon cash. We must promote the diversity of currencies and payment means. Bitcoin, Ethereum, and altcoins represent a huge change in the monetary world, but you should not abandon the simplest payment methods.

Some euro banknotes, by cosmix - Pixabay

Who are the users of cryptocurrencies in Europe? What are the possible short term evolutions of the market?

We observed a significant increase of interest in cryptocurrencies during the first half of 2017. The users are mainly people between 20-40 years who are interested in new technologies and alternative payments methods. They took the time to read about the blockchain, Bitcoin, Ethereum and altcoins, and they regularly read news about the recent developments, the charts and the ICOs (initial coin offerings). Lots of them are investors, and some of them are speculators. With these few points, you can know what are the obstacles for the general public.

Cryptocurrencies are not easy enough to use for uninitiated users. The amount of information to understand and start using Bitcoin is quite big for people who are not really comfortable with learning new technologies and for those who don't easily shift their habits.

You can buy stuff with bitcoins or litecoins, but it's quite difficult for other things. Try to find a place where you can pay your rent with cryptocurrencies, at the moment you won't find a lot of possibilities...

The usual way to buy cryptocurrencies is to create an account on a trading platform. Then, you have to use some money from your bank account to buy coins. Once you have your coins, you'd better to transfer them to a wallet on your computer or on your smartphone. Furthermore, the main platforms in Europe and North America are available only in English, which could be quite problematic for people whose native language is another language. However, the purchase of bitcoins could become easier in some countries. For instance, in the US and in Japan, you have more and more Bitcoin ATMs. On July 18, Bitpanda announced that Bitcoin, Litecoin, Dash, and Ether could be purchased at more than 1,800 post offices. In Switzerland, the Falcon Private Bank is the first bank to offer Bitcoin assets management: for some clients, it could be more convenient than using Coinbase, Kraken or other trading platforms.

The lack of regulation is a problem for skeptical non-users. Given that the Bitcoin and the major other coins are not recognized as real currencies in most of the countries in the world, many people think cryptocurrencies don't have a real value. Put yourself in their mind. If you want to buy something on the Internet with bitcoins, what would you do if you get scammed? Would your insurance offer you a compensation for stolen "virtual" money? If the major cryptocurrencies are not recognized as real currencies, you cannot receive your salary in crypto-coins directly from your employer, you need an intermediate.

There are only a few places in Europe where you can buy with cryptocurrencies. To spread the use of bitcoins, litecoins, and ethers, it requires having more online and physical stores accepting those currencies and some well-known practical services.

The market is evolving on those few points. More and more people are getting aware of the existence of the main interests of having cryptocurrencies, even though most of the general public is still reluctant and mistrust. However, nowadays, many people distrust the bank too, and some of them could be interested in crypto-coins which provide more privacy, faster transactions, and lower fees. Also, it's very important to preserve cash rather than eliminating it. Removing cash is interesting mostly for banks and big governments, not for ordinary citizens and their freedom. We need to keep a diversity of the payment methods. Cash users and cryptocurrency users have common points: they like the privacy of payments, they don't want a total hegemony of banks in the monetary system and they want to protect their money.

So, is the European general public ready for cryptocurrencies? Yes and no. Yes because Europe is ready to start evolving and adopting progressively bitcoins and some altcoins as spread alternative payment means. No, because crypto-coins are still viewed with a lot of suspicions and they are used only by a thin minority of people in Europe. They don't have the same success than in the US and Japan. But the European market is evolving, for sure.

Thanks for reading!

Articles about near-cashless countries

http://www.zerohedge.com/news/2016-12-04/these-countries-have-nearly-eliminated-cash-circulation

https://www.thelocal.no/20160122/norways-largest-bank-calls-for-complete-end-to-cash

http://www.ibtimes.com/norways-biggest-bank-calls-country-stop-using-cash-2276140

https://www.economist.com/news/finance-and-economics/21704807-some-europeans-are-more-attached-notes-and-coins-others-emptying-tills

https://www.ecb.europa.eu/press/pdf/pis/pis2015.pdf

Articles about the intensive use of cash in Germany

https://qz.com/262595/why-germans-pay-cash-for-almost-everything/

http://www.pymnts.com/cash/2016/cash-global-cash-index-germany-payments/

https://global.handelsblatt.com/finance/no-thanks-to-no-cash-759193

https://www.bundesbank.de/Redaktion/EN/Downloads/Bundesbank/Research_Centre/2016_01_research_brief.pdf?__blob=publicationFile

https://www.thelocal.de/20170518/vast-majority-of-germans-never-want-to-give-up-cash-poll-shows

pocketsend:20000@lefactuoscope,

Successful Send of 20000

Sending Account: planetenamek

Receiving Account: lefactuoscope

New sending account balance: 861640

New receiving account balance: 31996

Fee: 1

Steem trxid: 324173a5eee4d47c0c8667dad2fa9b5d074862f7

Thanks for using POCKET! I am a confirmer bot for fun, view my source confirmer code here. Don't know what a POCKET Token is? Here is a link to the official announcement post.