Trading crypto: Do exchanges manipulate volumes?

When liquidity is lacking. - On May 18, 2018, Eitan Galam published a study seeking to demonstrate the existence of a manipulation of the volumes of daily trades taking place within the microcosm of cryptocurrency exchanges.

The full study, of which this article is a review, is available here; while the Author's Summary Medium Post is available here. Both are currently available only in English. The illustrations used are therefore taken from the complete study initially.

In this study, Eitan Galam seeks to demonstrate that both exchanges and crypto-tokens-issuing teams have a common interest in manipulating the data available to the general public regarding daily trading volumes. Not content to demonstrate it, the study also quantifies this manipulation.

Why are the data manipulated?

What's the point in manipulating daily trading volume data taking place on an exchange? Who are the potential winners of such manipulations? The author asks these fundamental questions, before going into the heart of the matter, wondering about the implications of these manipulations. Indeed, one could say that from the moment one manages to exchange his cryptos on these exchanges, what difference can it make to know that the volume figures of trades are rigged?

The volume of trade (trading volume) is important because it is a key indicator: it is for most market participants (as well traders, token issuers, exchanges, curious legislators) a very literal illustration of liquidity potential of a token, that is to say real possibilities of exchange, different depending on whether one is:

- A lambda investor, eager to buy a token in the volume he wants, to keep it if desired but especially to know that he can resell it to lock in gains when he wants, possibly also in times of market panic ;

- An issuer of tokens, who will want to list his token in the wake of his ICO (Initial Coin Offering), will seek priority to appear on an exchange with the effective liquidity, to gain a better exposure and hope for positive spin-offs in terms of valuation. token;

- An exchange, more able to aggressively negotiate the listing prices of a new token if its ranking in terms of volumes traded is high and looks healthy to other market participants.

Thus, manipulation of trades volumes taking place on cryptocurrency exchanges has many consequences: if the figures given are false, a participant can no longer be sure of the liquid or illiquid nature of the market. We were talking about this problem recently here, in another perspective however, to observe that aside cryptocurrencies occupying the top of the ranking in terms of capitalization, very few crypto-tokens were actually really exchanged. So if in reality, an exchange has a low volume, it has by extension a less liquid character than a competitor. However, less liquidity implies that any considerably bearish trade can literally take the market down, or even very quickly create panic movements, and therefore a greatly increased volatility. If the dice are piped, it is ultimately the investors, trader (Sunday or not) as token transmitter, who will drink.

Which actors would be responsible for the manipulation?

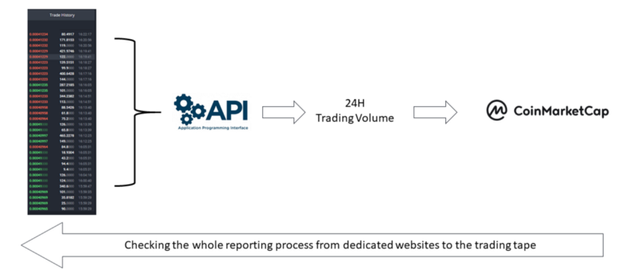

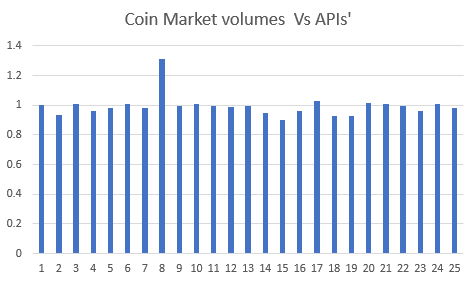

The central question, to identify whether a manipulation really takes place, is for the author to clarify the role of each, and thus to identify the person responsible for the manipulation: the daily trading volumes are indeed provided to the public by specialized sites (such as CoinMarketCap), but the data is provided to these sites through the exchanges themselves. In these conditions, the author looked for the origin of the supposed manipulation: if it specifies that it seems to him very unlikely that the fault returns to the sites type CoinMarketCap, he checked the hypothesis all the same.

In addition to the fact that it would be necessary to envisage a vast global conspiracy requiring, for the sake of coherence, that all the sites of this kind are coordinated in the handling and are all paid and agree to do it, the effective verification of the numbers reported by the CMC type sites are quite consistent with the numbers provided by the exchanges APIs. So ... the manipulation would take place directly on the exchanges.

What is the magnitude of manipulation?

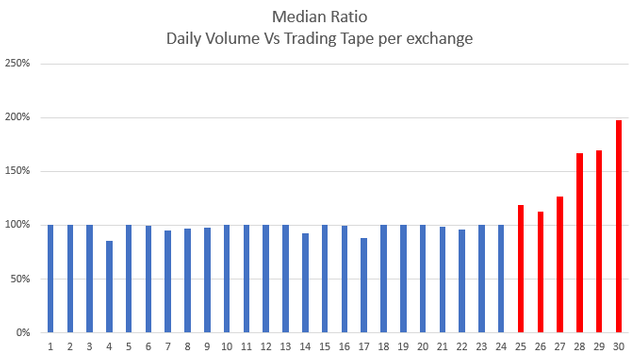

To quantify the importance of this manipulation and its more or less usual character, the author compared the daily trading volumes provided by the exchange APIs with the sum of all the trades directly on the order book of the exchanges.

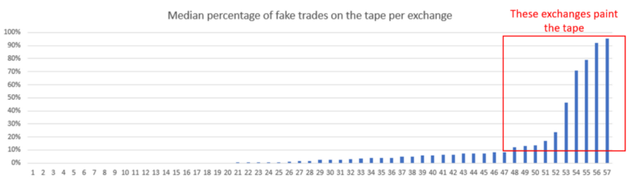

Median ratio of differences between the number of trades provided by the API and trades

effective on the order book, by exchange: the exchanges in red inflate their statistics. Under these conditions, nearly 20% of exchanges inflate their figures before transmitting via their API.

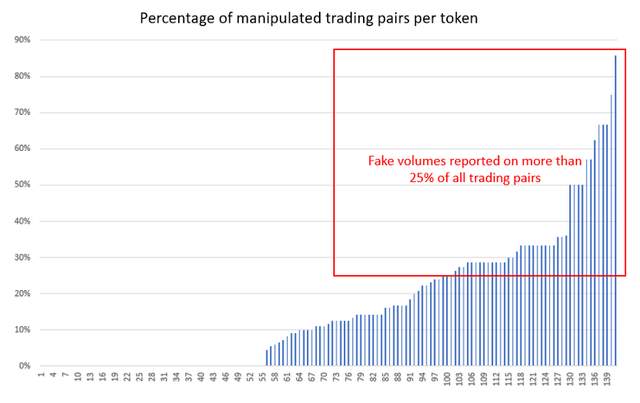

More specifically, it seems that some exchanges preferentially manipulate only part of their tokens, or that some tokens are handled relatively constantly between the exchanges.

Also, some tokens are thus systematically manipulated, in all trade pairs offered and on almost all exchanges, as illustrated below.

This habit of artificially inflating the numbers is raised so regularly on some tokens that the author of the study considers that it is a strategic policy of certain exchanges to pusher certain tokens. This policy could be explained if the exchange had a financial interest in the token in question, or because it is the issuer, or because the issuer has entered into an agreement involving the token.

The author also makes another distinction, verifying that more valued tokens tend to be - paradoxically or otherwise - more manipulated than tokens at the more modest valuation.

The figures provided illustrate that both exchanges and token issuers may have common interests in this scheme, and that the attitude is fairly systematic.

How are the data manipulated?

In order to assess the reality of this market manipulation, the author has identified the questionable trades, which he defines as the trades that have in place or at the extremes of the rational range of trades, that is, or well in the middle of the trade range when they should not be realized, or at prices that are too low (to be rationally submitted by a seller) or too high (to be rationally purchased by a seller). buyer) in relation to the momentary trading context of the exchange in question. Some just issued tokens, according to the author, show one-day price changes of almost 20 basis points (0.02%), which is already equivalent to the volumes traditionally observed for shares of a medium-sized company. listed on the NYSE.

Thus, these trades correspond according to the author to "wash trading", that is to say that trades that did not take place are added in the order book by the exchange itself.

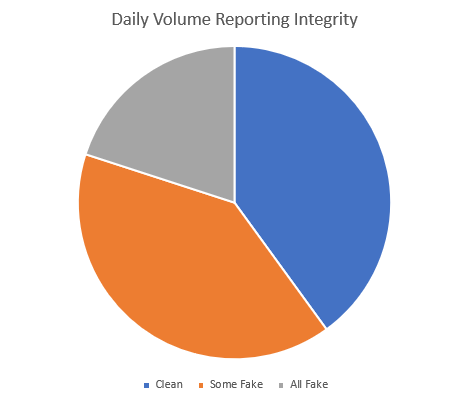

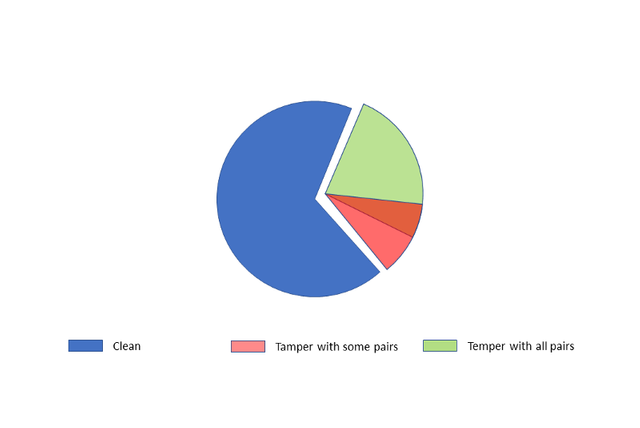

It should be noted that most exchanges act in the proper way and that this is not a generalized attitude, even if it is relatively widespread.

Thus nearly 17% of the exchanges fudge their volumes in a relatively global way, while 28% of the exchanges still use wash trading to a lesser extent by "limiting themselves" to specific tokens.

Conclusion

Our presentation of this study is coming to an end: it is therefore one of the first studies precisely quantifying the manipulation of trading volume data, a previous one to read also from early March 2018 and available here. In the end, and even if it might seem paradoxical, trading volumes are still so heavily manipulated that an exchange classified as a top-tier exchange may actually offer less effective liquidity than a more confidential exchange. This study sheds new light on a phenomenon long suspected and often accepted in the context of the deregulated exchanges of the cryptosphere, but we must be aware before embarking headlong into this great bath, whether we are simple investor, Sunday broker or entrepreneur thinking about going through an ICO to finance his project: the data provided by the exchanges to illustrate their supposed liquidity seem quite falsified, according to the study presented.

Source: Study: Quantifying fake volumes on cryptocurrency exchanges || Image from Shutterstock

Interesting read, but I'm a bit puzzled by the definition of questionable trades

After all, this is trading. How would you even define rationality? Is it rational to buy something which you believe is priced too high, but which you also believe will go even higher? Is it rational to buy something undervalued, even if the trend is going downwards? Do you catch my drift?

My point is that I'm sure a lot of legit trades could be considered questionable by someone more experienced or someone who watches from a different context.

This post has received a 38.5 % upvote from @boomerang.