The Bitcoin Crash Pokes Holes in the Tether Conspiracy Theory

“For Griffin and Shams to directly link this movement to Tether is bold, and unfounded, given that is how Bitcoin acted even before Tether was introduced to the market.”

The last year had the looming presence of a large conspiracy surrounding Tether. The seeds were planted by various bloggers and Twitter personalities. Suspiciously, the ideas continued to thrive once seemingly reputable individuals, such as John Griffin and Amin Shams of the University of Texas, graced the front pages of major news outlets proclaiming vast half-truths about the cryptocurrency.

The Griffin and Shams paper claims to do its best to analyze the available information on Tether. Using their statistics we see there were connections made where no evidence was present. The Tether conspiracy leaves a lot to the imagination, and it seems some individuals use their credentials and interpretation to make unfounded conclusions.

Tether is a pegged asset cryptocurrency. It is pegged to the price of one USD. Tethers are purchased through their parent company Bitfinex — a cryptocurrency exchange. When someone deposits money into Bitfinex, the individual is given Tethers in return to use on Bitfinex or any of the other cryptocurrency exchanges that accept Tether.

The reluctancies many have surrounding Tether are based on a conspiracy theory that gets recycled around the internet. The Tether conspiracy assumes Tethers are issued arbitrarily without key people having to deposit money into Bitfinex. It is believed Bitfinex issues Tethers to insiders for themselves to buy Bitcoins for free, then sell those Bitcoins at a profit to even their bank account. This Tether conspiracy theory is believed by some to be the reason for Bitcoin’s bull run during 2017.

One main argument for the Tether conspiracy is the idea that once Bitcoin’s price stopped increasing, Tether would collapse into itself. According to Griffin and Shams, “If cryptocurrency prices crash, Tether creators essentially have a put option to default on redeeming Tether, or to potentially experience a ‘hack’ where Tether or related dollars disappear.”

Tethers Issued March 17th, 2017 through June 25th, 2018 (Graphic by CoinStudi on TradingView)

The current market trends test Griffin and Shams hypothesis. The cryptocurrency market is in the middle of a major crash. Bitcoin lost 70% of its market value, and conjunctly the entire cryptocurrency market fell from its 836 billion dollars all-time high in December 2017. Many Altcoins (cryptocurrencies other than Bitcoin) have lost 90% or more of their value to-date.

In the downturn, Tether is used now more than ever. Over double, the number of Tethers were issued on the way down from Bitcoin’s all-time high on December 17, 2017, than on the way up. 820,048,400 Tethers were issued pre-December 17, 2017, and 2,080,000,000 were issued since. The Tethers issued since December 17, 2017, have not stopped the market from its continued bearish direction.

Using the chart above, it is difficult to make the argument that Tether props up the price of Bitcoin. The to-date bear market of the last six months is direct evidence of this argument. For proof of Tether manipulation, Griffin and Shams stated, “From March 1, 2017 to March 31, 2018, the actual Bitcoin price rises from around $1,190 to $7,000 for a 488% return. In contrast, the price series without the 87 Tether-related hours ends at around $4,100, a 245% rise.”

The qualifications for the 87 largest Tether issuing events required a price dip followed by a price increase. They continued, “In line with the evidence of purchases following Tether issuances and negative returns, we condition on Tether issuance in the prior three days, negative returns in the prior hour, and flows above 200 coins on both the Tether and Bitcoin blockchains in the prior hour.” These qualifications negate many of the large Tether issuances in which there was a price increase followed by a fall. Especially in 2018, where large issues of Tether were followed by massive drops in Bitcoin’s price. Not to mention, Griffin and Shams never stated which 87 they were using in their sample.

The Griffin and Shams criteria purposefully sought to correlate days where there was heavy Bitcoin buying after a retracement. These days have been historically positive for Bitcoin. Griffin and Shams failed to test this against other historical Bitcoin bull runs to see if Tether was the cause of the additional increase, or if they chose to sample heavy Bitcoin buying days.

Below, are images of other historical Bitcoin runs well before Tether’s existence. Griffin and Shams chose to ignore previous historic Bitcoin behavior as a control measurement. Bitcoin acted with violent upswings many times in its short history. For Griffin and Shams to directly link this movement to Tether is bold, and unfounded, given that is how Bitcoin acted even before Tether was introduced to the market.

Griffin and Shams are right to question Tether because Bitfinex opened itself up to conspiracy. The company is shrouded in mystery. The Tether website makes claims of regular audits that have never been upheld. One of the great promises of blockchain technology is its transparency, but the centralized Tether is far from transparent. It is obvious when Tethers are issued, but not from where they originate. Tether has been unable to be audited by an accredited auditing company. However, they released audit-like documents from different agencies including the Freeh, Sporkin & Sullivan LLP law firm summer 2018. The documents showed that the amount of Tethers in circulation is equal to the number of Tethers in Bitfinex’s Tether bank account.

It is safe to say that Tether was not the cause of Bitcoin’s historic rise in late 2017. Also, there is still no verification of secure backing of Tether’s assets by deposits from individuals and exchanges who have purchased Tether tokens with US Dollars. While Griffin and Shams may have jumped to conclusions in their paper, the jury is still out on the Tether conspiracy.

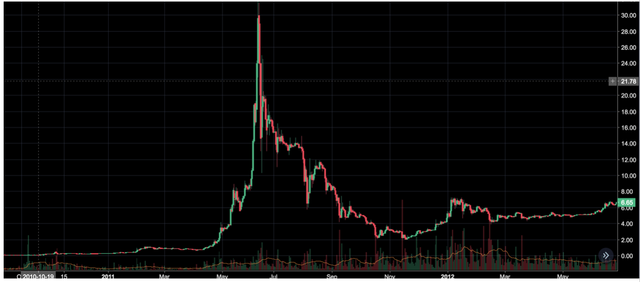

Bitcoin 2011 (Graphic by CoinStudi on TradingView)

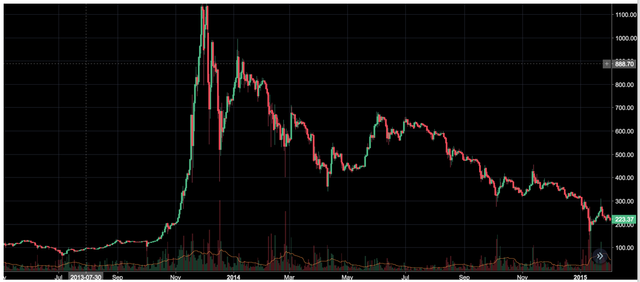

Bitcoin Early 2013 (Graphic by CoinStudi on TradingView)

Bitcoin Late 2013 (Graphic by CoinStudi on TradingView)

Griffin, John M. and Shams, Amin, Is Bitcoin Really Un-Tethered? (June 13, 2018). Available at SSRN: https://ssrn.com/abstract=3195066 or http://dx.doi.org/10.2139/ssrn.3195066