Help remote communities get clean water - Introducing Fluence Corporation!

Let me introduce you to what I believe is one of the most exciting investment opportunities on the Australian Stock Exchange: Fluence Corporation.

Before I get started: this is NOT financial advise, this is my view of the world only. DYOR! Disclaimer: I am invested in the company.

Now, for those of you actively involved in the markets, you might say: Fluence? Never heard of them. And I wouldn’t be surprised, given that the company officially only commenced trading this week. However the two companies that merged into Fluence you might have heard of: Emefcy and RWL Water.

In this post I would like to provide you with my rationale for investing in this industry, why I think Fluence Corporation is the right company at the right time and lastly why I believe that this is undervalued at the moment.

For those of you that have a short attention span and don’t want to read through the whole post… these are the reasons:

- Water is the new gold. If you could invest your money making the world a better place for people, and make money doing that, wouldn’t you?

- Fluence’s technology is innovative and its products are truly global, scalable and targeting a large niche market.

- The Leadership team is top-notch with an impressive and proven track record and is backed by billionaire Ron Lauder with significant skin in the game.

- The share price is undervalued at the moment making it an excellent longer term investment opportunity.

Let’s dive in. I’ll be using some material from Fluence’s investor presentation, you can find this presentation on the new website: https://www.fluencecorp.com.

Why is WATER the new gold?

So let’s start by discussing the size of the opportunity here. Everyone knows the story of Dr. Michael Burry from The Big Short directing all his investments to water now. But why is this? I can see what you’re thinking. Water has been around for a while…and you’re right. However as clean water in most part of the world is considered to be “normal”, in increasingly larger parts of the world, it isn’t. With a fast growing population there are communities that struggle to manage all their waste water and provide clean and safe water for its constituents. Most rural wastewater in China for instance is untreated and most rural surface water is now polluted!

If you look at the size of the global water market you can almost divide them into three categories:

- The top end, which is made up of large multinationals with large centralised desalination plants and infrastructure, that can treat entire cities.

- The bottom end, which is made up by SMEs that provide limited products and services that are generally lower quality in terms of technology.

- And then in the middle we have the pre-packaged water treatment market, which is the market that Fluence will be targeting.

Countries have been actively dealing with this “middle market” in recent times, one of the biggest examples being China. After years and years of a booming industrial economy, in February 2016 China has adopted a five year plan, mandating to provide wastewater treatment for an estimated 440 million rural people throughout China. It includes Central Government funding to increase the proportion of remote Chinese villages with wastewater treatment from 10% to 70%. Under the five year plan, more than 100,000 "off-grid" communities are currently seeking innovative, cost effective and decentralised wastewater treatment solutions

Large centralised solutions are often not able to service the rural communities due to the high cost of distribution of water. They also lack the funds to engage the big boys and these solutions take out a lot of energy from the grid as well, which in these rural areas can be a challenge.

So really what we’re seeing at the moment is that the “big boys” at the top end of the market focus on the big projects servicing the large cities in the world but there is an increasing need for someone to step into the “middle market”. According to the company: “there is no other company that has the global footprint that we do in that market, and we will hopefully play the number one role in decentralised water, wastewater, and waste-to-energy. We strive to make the world our backyard”. Isn’t everything decentralised better, Steemians…;).

But what about the $s? Well, if we just zoom in on the size of the packaged water and wastewater treatment market, it’s currently valued at ~US$13.3bn and it is forecasted to expand at a compounded annual growth rate of 10.4% to 2021, resulting in a US$21.8bn industry. That ain’t peanuts. The China five year plan alone is considered to be a $15bn opportunity over the five years!

So how does Fluence help?

You can read up on both Emefcy and RWL Water’s history in the investor presentation on the website, what’s most interesting is what they have to offer. Enter Fluence’s MABRE solution!

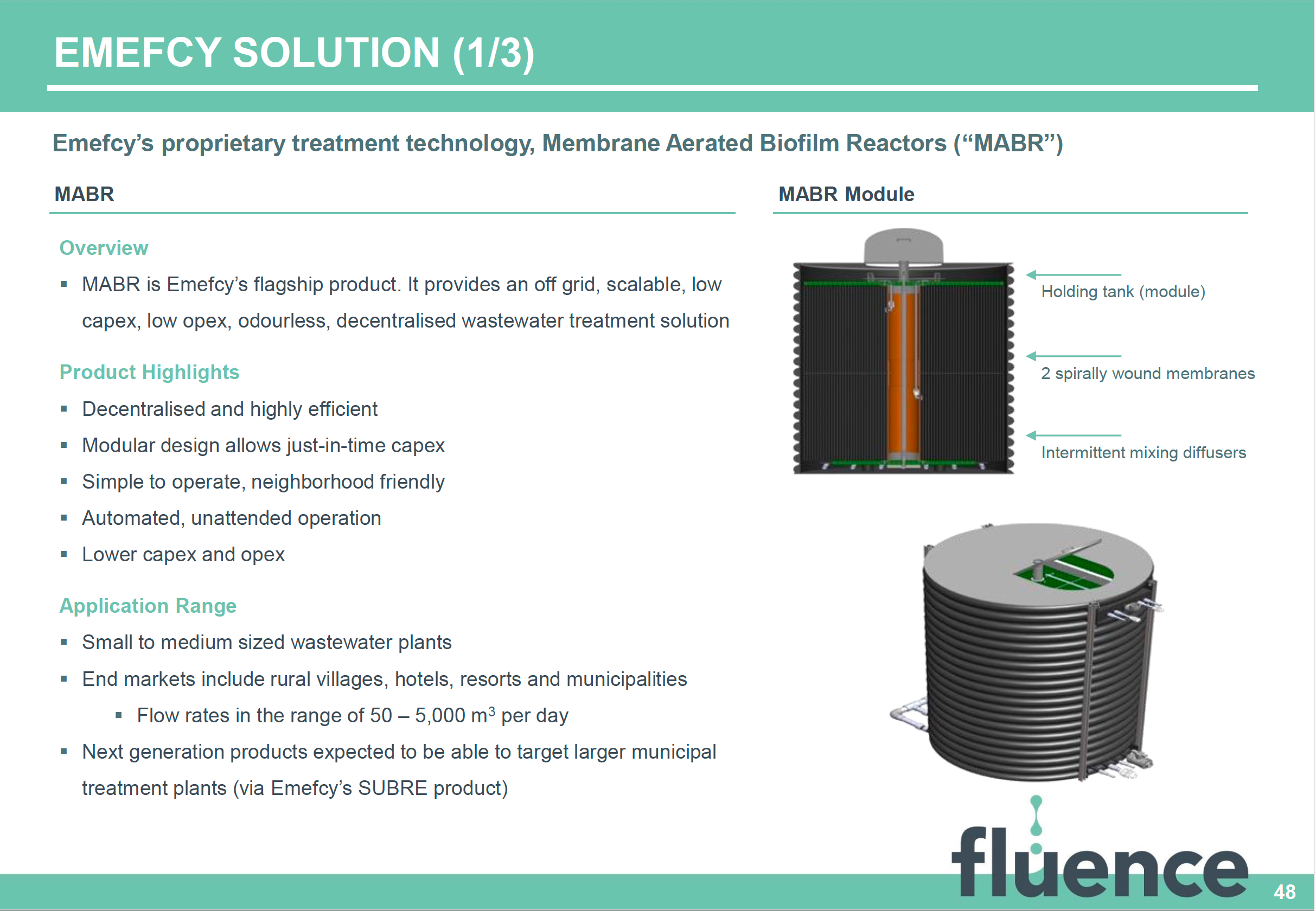

I won’t go into the specific technical details here but the key thing to note is that Fluence has developed their proprietary treatment technology, Membrane Aerated Biofilm Reactors (“MABR”), which provides “an off grid, scalable, low capex, low opex, odourless, decentralised wastewater treatment solution”. It uses 90% less energy than previous state-of-the-art treatment solutions!

With the MABR solution Fluence offers a solution to can be deployed quickly, with significantly lower capex since there is much less water pipeline infrastructure required compared to centralised plants. Perfect for smaller communities!

And they are tracking really well to date. Just focusing on the MABRE solution alone, Fluence has a fully-functional manufacturing facility in Israel that has been in operation since 2015 and is due to commission its China manufacturing facility in H2 2017. It has reference sites in Israel, the US, Ethiopia and various sites in China. It has already signed agreements with eight distribution partners in China and has several demo plants set up and/or underway. It is gearing up BIG time for the China opportunity!

What’s the catch here?

I know what you’re thinking. This sounds too good to be true. And yes, this sounds amazing but if China is such a large part of our strategy, what prevents them from engaging Fluence, copying the IP and pushing them out? Excellent question! The way the plants work is that they are controlled using technology in the cloud, which means they can be controlled from anywhere and this technology is protected and hard to copy. In other words, knowing how to build the MABRE product alone isn’t enough.

And if you have done a bit more research you would say, but Jeroen, MABR is not providing communities clean drinking water, it’s providing them with irrigation water out of waster water. And again, you would be right. However this is first step. the company is working on innovative products already (like SUBRE) to take that next step. The business model behind this is extremely interesting as well, Water as a Service (WaaS). But first the focus is on the first step.

But “hang on” you might say, this technology is what Emefcy has developed. You mentioned a merger between Emefcy and RWL Water, what are these guys bringing to the table? Well, RWL Water is a company that is already achieving high revenue growth (30/40% annually) by delivering solutions on a wider scale across the water treatment spectrum to customers globally. It has operations in over 70 countries already and employs more than 250 people worldwide. It effectively gives Emefcy the footprint and established sales relationships to accelerate the rollout of its MABRE (and subsequent) products.

As they state on their website:

Fluence provides local and sustainable treatment and reuse solutions, empowering businesses and communities to maximize their water resources. Fluence offers an integrated range of services across the complete water cycle, from early stage evaluation, through design and delivery, to ongoing support and optimization of water-related assets.

And have a look at pages 24, 25 and 26 of the investor presentation for a break down of the different services offered across the water management value chain.

Who is running this show?

Having learned the hard way (this is a story for another time…), the product can be the best in the world and it’s the right opportunity at the right time, but if the management behind it is just in it for their own benefits (think, pump and dump) there will be no capitalisation on this opportunity.

Fluence is nothing like I have seen on the ASX spec world before. It is led by a highly experienced and credentialed management team and board with extensive experience in the industry and growing companies. Have a look:

Furthermore, when you’re trading at the speculative end of the market, stocks that get backed by millionaires (or in this case, billionaires) always attract the attention. Why? Well, it’s easier to imagine that situations that require cashflow are a little bit easier resolved but more importantly, what made most of these people rich beyond measure is that they hate to lose money. Would they back something that would lose them money? Unlikely. And in the case of Fluence being true global players, being backed by Ron Lauder (look him up…) who has connections in the highest places in this world can only be beneficiary. And here’s the kicker: he’s committed US$ 20M of his own money to back Fluence. He’s been given 31.8M shares at a price of $0.85.

I need to get involved!

Slow down slow down...Obviously the investment opportunity is only as good as the price you have to pay at the moment to get involved. And looking at the price, it seems to be in a short term downtrend since the merger was officiated, why is this?

That is a very good question, I would be asking the same. I believe that - since market emotion leads to market decisions - investors are being a bit more cautious after the merger hype given that profitability won’t happen until CY 2019. Futhermore, I believe that many expected more news to be released in terms of contract wins as part of the EGM to decide on the merger, which has not happened (yet). Lastly, given the issue of the additional 130M shares the same price will obviously give a higher market cap. With a merged company it is hard to assess what the true value is of the combined entity.

Which takes me to the next point. Determining the market cap of a company that is established usually happens by looking at earnings and applying an industry multiple to these based on forecasts and expected growth figures. Now, since we’re talking about a company that is established but still young, this gets a bit trickier. At the same time, this is where the art meets the science and this is the cool stuff! Am I right??

So this where it gets a bit technical but I’ll try to keep it simple. Fluence has reported that it is expecting a revenue of US$ 90M (AUD approximately $120M) this year. We know that RWL Water has been growing at a 30/40% rate annually. In the last reports it was mentioned that 83% of 2017 forecast revenue of US$90M has already been secured under backlog and revenue, a little over 50% into 2017. It is not hard to imagine that they would exceed expectations there.

Its market cap is (at the time of writing this) $313M AUD at a share price of $0.805. We know that Ron Lauder has accepted shares at a price of $0.85 which would signal he values the combined entity at a market cap of $330M AUD (excl. options and milestone shares).

But no need to run all the math yourself. The company has engaged an independent company to do that for us. The Henslow report provides us with a with bear, base and bull case scenario: http://www.emefcy.com/wp-content/uploads/2017/06/Henslow-EMC-090617.pdf. Indicative share prices for each of the cases range from $1.06 to $4. Some say Fluence needs a “hyper bull case”, but I’ll leave that up to you to decide.

So it comes down to what you believe is the expected case for Fluence. For me, I’m very bullish (I’m sure this is no surprise at this point) and so I think the share price can be multiples of what it is right now. It won’t happen overnight and the share price of EMC in the past has behaved irrational at best so you have to be comfortable stomaching a dip before contracts are being announced and more detailed overviews of revenues etcetera come in. But if we look back 2-3 years from now I think we won’t believe the price we are buying it at today. I believe if we can hold the 80/81c mark right now we can see a slow and steady rise.

As always, investing takes time and patience, I’m NOT A FINANCIAL ADVISOR, this is NOT financial advise, all IMO so DYOR! DYOR! DYOR!

With these posts I am trying to give you an insight into my world as a retail trader, trading speculative stocks on the ASX as well as crypto currencies. I hope this is useful and any comments or questions, I would love to hear them!

Take care,

Jeroen (aka The Transparent Trader)