Has anyone ever thought of a new type of payment system 2

I have received a lot of feedback after my post "Has anyone ever thought of a new type of payment system?". Thanks to all of those who tried to analyse and set out their vision. Thanks to all of those who tried to analyse and set out their vision. Special thanks to those who doubted my competence and brought out their own understanding of the processes and entered into a dispute. And very special thanks to those few who used only accusations in scam and profanity as arguments - they made me understand that it is impossible to explain to everyone, no matter how hard you try. Nevertheless, thanks to the first two categories It became clear to me that the information presented in the article is incomplete and needs to be described in more detail, but of course, only to the first two categories.

I’ll say at once to everyone that the project does not raise money, no one campaigns for the purchase of tokens, the project does not conduct ICO. I deliberately published a post in order to understand the quality of the presentation of information and to what extent it is clear to those who do not run the project and who are not entirely in the subject.

Disclaimer

The chain of relationships listed below has been greatly simplified to facilitate understanding. Consciously omitted many things, the description of which would take a huge amount of space.

Introduction.

Majority who oppose technology do not look up to the future and, most importantly, have no idea about the past. Technologies are similar to science, innovation, they can frighten with their ideas and cause rejection in the beginning. After adoption, adherents become ardent followers and hardly recognise something new that goes against already established convictions. Bethink of Christianity - some tried to eradicate it, destroy it, burn Christians on fires, feed them to lions, killed unarmed people in gladiatorial battles. Later, Christianity itself has struggled with dissent - Galileo, Copernicus, Bruno. Examples that are closer to us in time are cars with internal combustion engines, telephone, radio, airplanes ... all these inventions met resistance at the stage of their appearance and caused a storm of ridicule and aversion and misunderstanding of the “use cases”. Not such a distant example with the advent of the Internet, when the web pages were so simple and uninformative that the majority of the population of the Earth simply did not take it seriously and, moreover, did not see its use. There are many such examples. And even the temporary absence of the “use cases” does not indicate the uselessness or irrelevance of the technology, it indicates that the world is not ready yet to apply the technology at the moment due to habits, beliefs, interests, and sometimes, incompetence. The topic of the blockchain and cryptocurrency in particular is susceptible to reproaches in the absence of its practical use, which is understandable due to the youth of the technology and its initial stage of formation and development. In addition, in some cases, the line should be drawn between the cryptocurrency and the blockchain technology itself, since the majority of people do not see the technology itself, but only its derivative in the form of a mass of coins, most of which are dummies and really have no application. But, nevertheless, even at the present stage of development of the blockchain technology, the talk about the lack of “use cases” indicates not owning information, well, or not wanting to see the obvious - merchants, Jaguar, Facebook...

All this applies to today's financial sector conditions. And that is obvious, because the technology of making payment via plastic cards comes from the 1950s. Several generations of people grew up on the existing system and have a long-established habit of using it. Several generations of banks earn huge amounts of money on commissions that customers pay. Several generations of companies providing these payments have changed leadership. Some have gone, and those who remain hold such strong positions and their profits are so huge that they have no reason to rejoice in large numbers for the technology - after all, they can shake their incomes, and the scale of these companies does not allow them to respond quickly to changing time. But even with this in mind, the interest of these companies in technology is obvious. Such pillars like VISA, MC, WU, Barklays, BBVA and many others either look for ways to introduce the blockchain technology or already use it. But, nevertheless, attempts to introduce the technology are still being applied to the existing payment system, credit, and financial relations. Now, I will introduce my own arguments and briefly describe essentially new approach to making payments.

Part One - "What are the existing payment systems and how do they work."

In today's payment system relations, there are six subjects:

- Client - buyer of the goods;

- Bank-Issuer, where the client keeps his money;

- Seller of the goods (Merchant), which accepts the client's card for payment;

- Bank Acquirer, where the Merchant keeps his account;

- Switch - payment system (PS) that connects the Issuer and Acquirer (for ease of understanding - VISA, Master Card, AMEX, Union Pay, etc);

- Processing center - an enterprise certified by the PS, which processes payments of the Bank-Acquire and Bank-Issuer.

There are still various clearing and settlement centers authorized by payment systems and local securities in different countries to carry out payment operations and perform clearing processes, i.e., reducing settlements between banks' balances, but we will omit them for simplicity of explanation and understanding, since these functions can be performed by Bank-Acquirer and, in our example, to simplify the description.

Suppose that an American client, whose account is held in a certain American bank, came to Australia to buy coffee. He pays with his plastic card, putting it to the merchant's terminal (POS-terminal). Money from a client is in the account of an American bank, how does the Merchant receive it? POS-terminal Merchant belongs to the bank in which the Merchant holds its account in Bank Acquirer.

- The terminal reads the client card and sends information about it to Bank-Acquirer;

- Bank-Acquirer is not connected in any way with the Bank-Issuer, therefore, it cannot request directly the payment, and the transfer directly from America to Australia will not allow the client to enjoy hot coffee. Therefore, Bank-Acquirer asks the Processing Center about the availability of the required balance on the client's card;

- The processing center requests Switch for the availability of the required balance on the client card;

- Switch contacts the Bank-Issuer and requests the availability of the necessary balance on the client's account;

- Bank-Issuer confirms to Switch the existence of the required balance (or does not confirm, then the refusal of the transaction occurs);

- Switch confirms to the Processing Center the presence of the required balance on the client’s card (account) and gives a signal to the terminal to confirm the payment;

- The processing center confirms to the Bank-Acquirer the existence of the necessary balance on the client’s card (account) and gives a signal to the terminal to confirm the payment;

- The client has paid and he leaves satisfied;

- Bank-Acquirer transfers the sum of purchase to the merchant's account;

- The Bank-Acquirer transfers information about the payment made to the Processing Center and issues a claim for compensation of the payment amount;

- The processing center transfers information about the payment the Bank-Acquirer made to Switch, since, in fact, the Bank-Acquire has transferred the money to its merchant;

- Switch pays from its funds to the Bank-Acquire (for simplicity of explanation, we omit here the clearing system of settlements through authorized clearing centers (in fact, the process is much more complicated);

- Switch bills the Bank-Issuer (for simplicity of explanation, we omit here the clearing system of settlements through authorized clearing centers (in fact, the process is much more complicated);

- Bank Issuer paid to Switch (for simplicity of explanation, we omit here the clearing system of settlements through authorized clearing centers (in fact, the process is much more complicated)

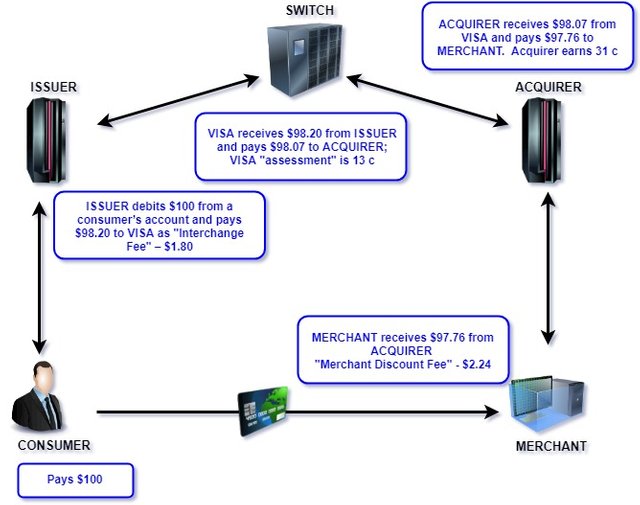

We can introduce schemes:

Switch is an intermediary between all the parties of the entire system and receives a commission for all transactions. Who can even imagine the infrastructure setting expenses to operate the processes of settlement analysis, comply with the requirements of KYC / AML, match modern safety requirements for the launching of data centers around the world. Of course, commission is the source to operate.

For ease of explanation, we imagine that the Switch is the processing center.

Conceptually, costs can be divided into Organizational and Technical

- Organizational:

creating jobs for staff of specialists, most of which are expensive: system administrators, engineers, 24 hrs. support services and an authorization center;

making decisions of the placement of software and hardware systems. Organization of your own premise(s) or placement of your software and hardware systems in the premises of a third-party company (outsourcer);

development of a system for controlling access to the premise(s) of the processing center, including such procedures as: organizing access monitoring, employees to the processing center premises, developing work procedures in high-security areas, etc .;

making a decision on the choice of the supplier of software necessary for building a processing center certified by an appropriate payment system;

deciding on the choice of suppliers of related services (for example, courier services and / or gateways for sending SMS or PUSH messages, and the subsequent construction of contractual and working relations with it;

development, coordination and implementation of procedures for correct work with cryptographic equipment and quantities, and issuance of domestic regulations governing the work of security officers (security officers); - Technical:

The purchase of hardware (system units, hard drives, RAM (random access memory, Does RAM), uninterruptible and backup power supplies, racks, etc.),

the purchase of the server software (operating systems, database systems, etc.), including license fees vendors of such software,

the purchase of cryptographic equipment necessary for the generation and correct processing of operations on cryptographic values, such as CVV or CVC;

information security solutions (ensuring compliance with the requirements of PCI DSS, federal laws, protection document management systems);

And such (all of the above) costs must be borne constantly, if we are talking about expanding your presence. Switch (processing centers) can cover these costs only with a part of the commission for the implementation of monetary transactions, which is borne by the other participants in payment relations.

Since the recipient of the client’s money is ultimately the merchant (seller / trader), it is logical that the entire amount of the commission is charged to him. This commission is called Interchange Fee (hereinafter - IF), it can be from 0.7% to 5% depending on the riskiness of operations. For example, an ordinary store, on average, pays 1.5% of IF, while, for example, an online store can pay 5%.

It is noteworthy that for the client this commission is not visible and in 90% of cases he does not even know about it. Such a commission is included in the price of the goods. That is, by selling you a product for $ 100, the Merchant will receive (if he pays IF = 2.24%) $ 97.76.

The Switch distributes these $ 2.24 between the participants as follows:

| Traditional Processing (TP) | Sum |

|---|---|

| Consumer pays | $ 100.00 |

| Overall Fee | $ 2.24 |

| Issuer Receives | $ 1.80 |

| Acquirer Receives | $ 0.31 |

| Visa Receive | $ 0.13 |

| Merchant Receives | $ 97.76 |

So we pulled how the current payment system functions. Now, in detail about how this can function using blockchain technology.

Part 2 - “New payment system and how it works.”

One of the main significant achievements of blockchain technology is excluding of intermediaries. In the field of finance, this gives special advantages — cost savings.

A new type of payment systems based on blockchain can successfully use this advantage. Naturally, there are necessary assumptions for the use of this technology in the financial sphere:

- It is necessary that the two contractors and the Merchant are in the same blockchain;

- Merchant must have a POS terminal transmitting information to the blockchain;

- Banks must open clients wallets and implement data exchange between blockchain and ABS (automated banking system) of the bank;

- In order to comply with the requirements of KYC / AML, private keys are kept by the bank;

- Must be a blockchain base Switch to physically conduct clearing of payments between the Merchant and the Issuing Bank.

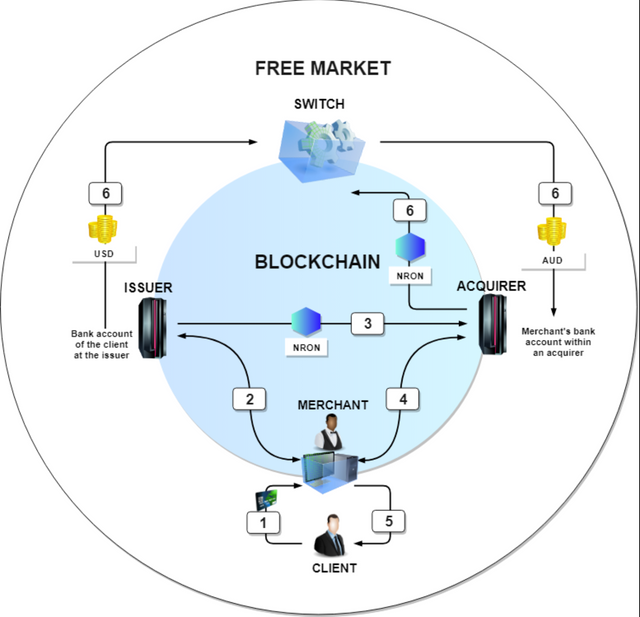

Just as in the situation above with our American customer buying coffee in Australia: the same American and Australian banks, but they are in the same blockchain. It is convenient to send just cryptocurrency, of course, but the question immediately arises - “Why does the Merchant need it and what will it do with it? How will he solve the issue of currency fluctuations? ”Immediately make a reservation that I will not describe the technology here thoroughly, since this is a commercial secret, but briefly, I will describe the principle of operation.

So, two banks are in the same blockchain. In the blockchain, there is a special protocol implemented that allows to “mirror” the client fiat accounts to the blockchain, thus, the exchange of information between the client’s account and the blockchain takes place on an ongoing basis.

- The client brings the card to the merchant's terminal; the terminal requests the availability of the required amount in the blockchain. If the required amount is available (if not - decline), the protocol starts the transaction, which the client confirms (fingerprint);

- The Fiat amount on the client’s account of the Bank-Issuer is held by the Bank (thus collaterising the amount of cryptocurrency to be transferred);

- The required, “mirror” amount in cryptocurrency is transferred to the Merchant's wallet;

- Merchant's wallet, having received the transaction, sends information to the Merchant Terminal, payment is accepted;

- The American enjoys coffee. Now, the Merchant has a cryptocurrency on the wallet, Bank-Issuer hold amount in fiat currency;

- Switch (the very same payment system), “buys” the cryptocurrency for the Australian dollar from the Merchant in Australia, in America, the Bank-Issuer transfers Switch a collaterised amount of USD.

Again, for ease of explanation, I omit some points that accompany the clearing process.

The scheme of the work of the new payment system can be represented as follows:

What is the advantage?

Switch can set the price for its services significantly lower than existing today, because it saves on the entire infrastructure - hardware, data centers, personnel.

The Bank-Acquirer does not lend, in fact, the Merchant’s account, so its remuneration can be significantly reduced. In addition, in this chain of relations Bank-Acquirer is not needed at all, because the Merchant can hold an account immediately in the Switch;

There is no need to create processing centers, which means that you do not need to bear the costs of creating infrastructure;

The cost of the transaction in the blockchain network is from $ 0.01- $ 0,05;

Transaction time - from 1 to 5 seconds;

In numbers, everything looks like this:

| Decentralized Processing (DP) | Sum | Saving |

|---|---|---|

| Consumer pays | $ 100.00 | |

| Overall Fee | $ 0.650 | -70.98% |

| Issuer Receives | $ 0.35 | |

| Acquirer Receives | $ 0.30 | |

| Switch | $ 0.13 | |

| Merchant Receives | $ 99.22 | -65.18% |

The savings in the process are obvious! The merchant receives 65.18% more money on his account. Bank-Acquirer receives almost as much as in the scheme with traditional processing. The Bank-Issuer receives less remuneration, but under a scheme with decentralized processing, it bears much less expenses on security of payments, payment verification, customer verification, respectively, personnel costs, which always constitute the bulk of costs, decrease.

Conclusion.

In addition to the above economic factors, a new type of payment system has another, perhaps one of the most important advantages compared to traditional PS - to provide an infrastructure for the issuing of plastic cards for issuing banks is much cheaper than traditional PS.

The main problem that the new PS will face is the speed of processing payments. VISA today can handle 150 million transactions per day or 1,700 transactions per second with the possibility of securing up to 24,000 transactions per second. Until a certain time, no public blockchain could solve this problem. Now, compared to the published data on the speed of other blockchains on main net, NeuronChain can confidently claim 2nd place at its speed of 100,000 tps, so this issue is no longer a deterrent.

Of course, to implement the payment relations described above, it is necessary to do a great deal of work, not only on the IT part, but also on technical and legal issues, to spend tremendous efforts on marketing and explaining the processes of the participants in the relationship. But impossible is nothing. In any case, the blockchain technology gives us this opportunity.

Join us -

https://t.me/neuronchain

https://twitter.com/neuronchain

https://medium.com/@neuronchain

https://www.facebook.com/NeuronChain /

https://www.instagram.com/neuronchain/