Part 1: The Blockchain

Before I begin explaining what the Blockchain is, imagine we lived in a world where we could send money to anyone worldwide using a low fee digital payment system that removed the need for a financial institution mediating the transaction. Where you could store your hard earned money via a secure digital wallet, which is linked to a decentralized open ledger. A secure open ledger that is distributed peer-to-peer all over the world and internally resistant to regulation from a central power, i.e. a bank or a government.

Consider the impact of this in places such as Venezuela where the inflation rate has reached 6500%+, leaving citizens of Venezuela with a valueless currency. How do families get basic needs to ensure the wellness of their families under these conditions? Especially when the Venezuelan dictator continues to deprive his people of basic resources.

In the year 2014, 80% of the population with cell phones in Kenya used their devices for payments and banking services via a microfinance loan payment system called M-Pesa. The system allows Kenyans to transfer money for low-interest rates, which has made basic banking services more accessible to a significantly higher percentage of the population in Kenya.

South American countries such as Venezuela and many African countries such as Kenya have been subjected to poor economic conditions due to, let’s be real, crappy government policies. These are the places most ripe for an economic revolution.

I’m sure you’ve heard of “the Bitcoin”. In actuality, Bitcoin is that distributed peer-to-peer network I told you to imagine! I’m sure you knew that already though. I’m sure you’ve also thought about how revolutionary the implications of this technology could be. I’m sure you’ve researched coins that even surpass Bitcoin in achieving these, and even more complicated goals. If not, follow me.

What is a Blockchain?

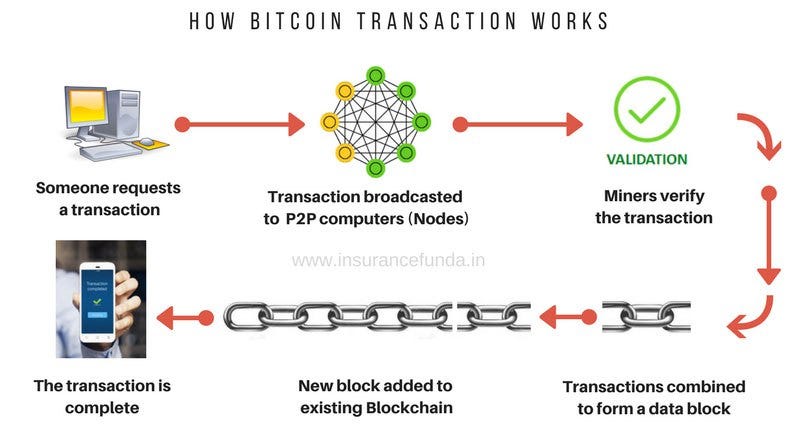

Think of the Blockchain as a set of records, called Blocks. Each of these blocks are connected to one another, hence the name, Blockchain. Each of these blocks contain a list of transactions completed by users worldwide.

A user purchases Bitcoin through an exchange such as Coinbase. The transaction is then broadcasted to nodes (miners) on the Bitcoin network worldwide. Miners compete with one another to secure the transaction onto the next block. They do this by solving hashes of the next block or, in simple terms, solving the cryptographic puzzle which allows them to secure the transaction onto the block. In order for miners to secure the network, they need the right computational and energy resources.

Once a miner verifies a transaction onto the next block, the user who purchased the Bitcoin on Coinbase receives the Bitcoin they purchased while the miner receives a reward of newly mined coins for securing the transaction onto the block. (Example shown below)

Blockchains were designed to be resistant to modifications of data. Once a transaction is recorded onto the blockchain, the data within the block cannot be altered without first altering all of the other blocks in existence. This is considered to be borderline impossible, since it would require the majority of the network to collude and attack its own network. This distributed ledger technology has allowed us to achieve complete decentralized consensus, meaning that we can share value among one another without a central authority or mediator.

Blockchains are suitable for more than simple financial transactions. They are suitable for many other applications that require secure databases, such as maintaining medical records, identity management, food traceability, and even voting systems. We are in the midst of something greater than many can imagine. The internet has allowed us to communicate knowledge among one another, blockchain has allowed us to share hard earned value between one another in a completely decentralized manner. If you don’t think that’s some revolutionary stuff, I must be crazy.

Note: The intention of this series is to simplify Blockchain technology for those who are new to this market. I will do my best to avoid lengthy and super technical details that create confusion. I hope that I am able to help, so feel free to chat me up. I also want to encourage blockchain enthusiasts or lovers of any kind who have suggestions on my descriptions to help me edit this post. I can only hope these posts will encourage others to do their own research before investing into this space.

In the next post, I will describe the need for tokens to create a decentralized network, staking as a means to secure the network, and how it works in more detail. Until next time!

damn very detailed post!! Will help alot of people out. Goodluck on Steemit friend!!

That's the goal! thank you!

;)

Clear and concise. Followed. Looking forward to more. Best of luck with it, man.

Thank you!

Excellent post Thomas - you are the first person I have followed! Clear and informative material like this is what makes SteemIt awesome (and what drew me to making an account today!).

I am looking forward to your posts to come!

My man! I appreciate the kind words!

You should do some airdrops: https://crypto-airdrops.de

so good

It was really good to understand. Thank you. I’ll read on the next post.

Orian Research published a new in-depth research report on Global Blockchain Technology Market 2018. This report gives you statistical analysis of the Market size, share, trends, demand, growth, manufacturers, current and future scenario of the market and forecast 2025. Get Sample copy of this Report @ https://goo.gl/muubvw

Orian Research published a new in-depth research report on Global Blockchain Technology Market 2018. This report gives you statistical analysis of the Market size, share, trends, demand, growth, manufacturers, current and future scenario of the market and forecast 2025. Get Sample copy of this Report @ https://goo.gl/muubvw

Thanks for sharing your thoughts and ideas with us about blockchain. Can't get enough of information and ideas that i am getting right now. Just wanted to share this blog about blockchain.

https://blog.kucoin.com/what-are-the-applications-of-blockchain-sk-st