Transforming Financial Services — A Not So Radical Approach!

Image Credit: Financial Times

Increasing compliance and cybersecurity costs, coupled with rapidly evolving client expectations mean that banks would need to embark on a fundamental transformation that surpasses their prior efforts. This article discusses the challenges facing the banking industry via few examples. The good news is that there is no attempt to entirely replace banks with new technologies killing all intermediaries or third-parties in the value chain. Instead, we are going to explore four ways in which a decentralized “blockless and chainless” computing architecture, the HelixTangle, can usher in a new era of banking.

1. Money Transfer without Banks

In his book, The Fortune at the Bottom of the Pyramid, C.K. Prahalad argues that both sides of the economic equation can prosper if companies revolutionize how they do business in developing countries. The World Bank estimates that almost 1.7 Billion people do not have access to a bank account. However, a study from the Harvard Business School found that banks view serving these people as an ‘unprofitable proposition’. Telecom companies have primarily benefited from banks ceding this space, with their mobile money market and removing barriers of financial inclusion, Telcos have leveraged their peer-to-peer networks to serve millions of people who feel ‘left out’ of the financial system (Banking the Unbanked). As a result, banks are playing catch-up to competitors beyond traditional finance.

Banks have shied away from such consumers because they “cannot” manage their risk profile. Many consumers do not have clear identifying information, making it difficult for banks to implement KYC practices. With new architectures like the HelixTangle, consumers can be issued with a digital identity, thereby putting in place a new reputation system that goes beyond a single score.

In addition, low-income individuals mostly need to make payments that are too small. They have no access to credit or debit cards because transaction fees make such payments impossible. Unlike existing distributed ledgers, the HelixTangle has virtually no transaction fees and makes micropayments possible. Also, existing blockchains are beset by slow transaction processing times and fail to efficiently scale up as adoption increases. The HelixTangle, on the other hand, is infinitely scalable and offers much quicker settlement times as more users perform transactions on the network. Adopting this technology can help banks attract a new consumer base, permeate untapped markets and fight poverty with profitability.

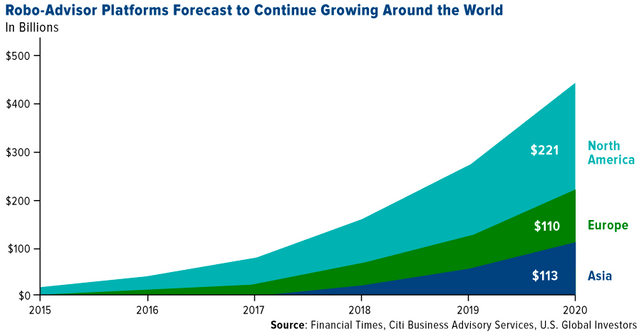

2. Deployment of Robo-Advisors

Ten years on from the financial crisis, banks are talking up the potential of artificial intelligence (AI) to revolutionize an industry dominated by legacy systems. Former Citigroup CEO Vikram Pandit predicts that AI and robotics could cut the number of banking jobs by 30% over the next five years. AI has led to the creation of robo-advisors: automated digital platforms that are capable of making better financial decisions than any human.

Robo-advisors represent a new wave in FinTech and have had a substantial effect on the wealth management industry. Traditionally, investors have depended on financial advisors who charge as much as 3% in fund management fees while raking up to 20% in incentive bonuses. The decade since the economic crash has seen robo-advisors gradually replace human financial advisors, thanks to lower fees, automatic portfolio rebalancing and tax-loss harvesting features. Citi predicts that robo-advisors could control global assets worth $450 billion by 2020.

Source: Frank Holmes

As the fourth industrial revolution unfolds, banks in Germany are showing a healthy appetite for AI, with Comdirect and Quirion already operating robo-advisors to create and effectively manage client portfolios. In the US, Fidelity entered the robo-advisory service with its Fidelity Go offering. Other robo-advisory companies include Betterment and Wealthfront.

DeepMind’s AlphaGo program showcased the inventive capabilities of machine learning when it convincingly defeated Grandmaster Lee Sedol in a five-game Go series. Next-generation distributed ledgers such as the HelixTangle can enable robo-investing upstarts to harness the potential of machine learning for developing accurate prediction models.

For instance, forecasts made by robo-advisors can be stored in the HelixTangle to create a shared, transparent and immutable database. Smart contracts on the HelixTangle can directly and reliably transfer data straight from the robo-advisor, ensuring that the information collected is authentic. The data can be studied to come up with superior models for managing financial risk and unearthing non-intuitive patterns. Some banks tend to differentiate robo-advisors based on their capabilities: the performance of each robo-advisor’s portfolio can be compared by analyzing data stored on the ledger. Additionally, clients can monitor the performance of their portfolio in real-time by accessing the information stored on the HelixTangle.

Since robo-advisors are easy to replicate, banks could find it hard to differentiate their services. Interestingly, October 2018 was bullish for crypto with Fidelity Investments announcing the establishment of Fidelity Digital Asset Services (FDAS), a subsidiary that aims to make the cryptocurrency market more accessible to investors. Banks could potentially differentiate themselves by introducing investment management services for new asset categories such as cryptocurrencies. Distributed ledgers can support banks in creating a niche and solidifying crypto as a new asset class for institutional investors.

3. Lending and Risk Management — A Controversial Potential

In Shakespeare’s Hamlet, Polonius counsels his son Laertes to “Neither a borrower nor a lender be.” While this might be regarded as sound advice, the lending business is here to stay. For years, bank lending was considered a crucial source of capital for small companies and startups. However, regulations introduced after the financial crisis have resulted in banks adopting increasingly conservative tactics towards borrowers. Banks are no longer prepared to take risks, and a gloomy economic environment has not helped small businesses either.

Millennials represent the first all-digital generation. The complex combination of legacy systems and third-party intermediaries has made it difficult for banks to react to customer demand on a real-time basis. Mortgage lending, for instance, takes up to 60 days until sale completion due to many arduous checks such as underwriting, title transfer and borrower credit score verification. To measure one’s risk of default, banks mainly value the credit score of a loan applicant. A short financial history implies that millennials struggle with their credit score, and as a result look for alternate sources of finance.

Smart contracts serve as a far more robust means for issuing credit and analyzing risk. With decentralized, cryptographically secure financial statements available at the click-of-a-button, the HelixTangle provides unprecedented levels of transaction transparency to banks and consumers. Thus, banks can encourage individuals and businesses to create an immutable digital identity on a distributed ledger such as the HelixTangle.

In addition to eliminating intermediaries, driving down costs and saving time, the HelixTangle can automatically disburse principal and interest payments, thereby reducing operational risk. These benefits could translate into more banks entering the $4 billion syndicated loan market, an otherwise labor-intensive and time-consuming process.

A host of fees associated with loans resulted in the lending business growing out of the purview of the banking domain. This transition was hastened by the increasing involvement of private market players who benefitted from a lack of regulatory scrutiny. The global peer-to-peer lending market is estimated to reach a valuation of approximately $900 billion by 2024, growing at a CAGR of 48.2% over the next six years.

While peer-to-peer lenders such as LendingClub, Funding Circle and Upstart serve as the market’s answer to a traditional problem, it is not without its side effects. Findings from the Yale School of Management show that regulators are unable to keep up with the rate at which FinTech firms are proliferating the market with offerings that meet customer needs. This has resulted in FinTechs operating in a regulatory void with substantially higher consumer risks.

Enter the HelixTangle, a panacea for a challenging and risky lending environment. Smart contracts running on the HelixTangle can significantly improve lending processes by automating loan agreement terms and increasing transparency for regulators through verifiable, immutable data. Parties can encode predetermined conditions such as loan amount, interest rate, payment installments, maturity date, etc. in a smart contract on the HelixTangle. Doing so can automatically trigger the disbursement of funds between parties in a timely manner as per terms of the contract.

4. (Self-)Auditing systems

An in-depth study conducted by McLagan and Accenture indicates that distributed ledgers can help banks achieve 30–50% cost savings on compliance. The HelixTangle can streamline the auditing process by eliminating manual activities and storing accessible financial data that cannot be manipulated. Banks need no longer assign staff to manually collect data nor deal with errors associated with this process. By recording all transactions on the HelixTangle, banks can generate error-free, up-to-the-minute financial statements at the click of a button. Information on the HelixTangle can be accessed by auditors to carry out the auditing process.

After the process is complete, auditors can store their report on the distributed ledger for regulators and bank officials to review. Once the regulators have considered the report, smart contracts on the HelixTangle can transfer this information to appropriate financial reporting instruments, streamlining an otherwise labor-intensive process. Distributed ledgers bring in a new wave of accounting practices that will facilitate fully transparent financial reporting in real time. By slashing time, costs and resources associated with vetting transactions, the HelixTangle can serve as a powerful RegTech innovation for banking compliance.

Ushering in a New Era of Global Banking

For years, banks have served as the foundation of global capitalism. However, a lack of trust and a growing sense of complacency has set the industry aback.

Rising compliance costs and dwindling revenues have seen banks battling a storm of diminishing returns. Adopting emerging technologies such as the HelixTangle can help banks optimize processes, lower compliance costs, mitigate cyber-risks and reimagine their workforce. By moving beyond traditional restructuring, banks can enable profound transformation that effectively addresses emerging challenges and opportunities.

Follow Helix Foundation on Medium, Twitter, Reddit, Discord, and Telegram.

An article by Rajeev Hegde - Research Analyst, Helix Cognitive Computing GmbH, originally posted on Medium