My Role in the Revolution-The Story of How I Made Bitcoin An Investable Asset - Part 2

In Part One of my Bitcoin Investment Journey (https://steemit.com/bitcoin/@twaddo/my-role-in-the-revolution-the-story-of-how-i-made-bitcoin-an-investable-asset-part-1), I discussed how I believed that an investment in Bitcoin could be considered part of an investor's portfolio as an alternative investment. As a journalist and author in the area of finance and specifically, retirement, I decided to find a way to place a Bitcoin based investment into a retirement account. I viewed both as long term investments and this part of my story is about the search for just such an investment. A reminder is that this part of the tale was written in 2014 and many things have changed.

PART TWO - HOW TO GET BITCOINS INTO YOUR RETIREMENT ACCOUNT June, 2014

By placing a bitcoin investment into my retirement account, I’m adhering to an asset allocation "rule" that suggests I should have some small portion of my overall portfolio in “alternative investments.” Alternative investments include hedge funds, private equity, real estate, commodities such as gold and silver — and I would think that bitcoins fall into that category.

My search to find a bitcoin investment for a retirement account hasn't been easy.

There is no way that I've found to place individual bitcoins into an IRA or any retirement account. Although you can buy and sell bitcoins on exchanges, my research shows that this can't be done in a qualified retirement account. Many of you may say, “that's a good thing,” — and you would probably be right.

Let's be honest, bitcoins are a risky investment vehicle. In fact, most investments considered "alternative" are risky.

Alternative investments are used in asset allocation models as a way to provide diversity, and in many cases, to limit volatility caused by market swings and events. Most alternative investments have low to no correlation to market securities such as stocks and bonds. This provides some cushion for your portfolio should events create wide swings in the returns of these securities.

“Alternative Investing and Your Retirement,” an article that I found on the Nasdaq website, reminds us that alternative investing isn't for everyone — and certainly not a novice:

" ... alternative investing is no safe bet, and requires both a deep knowledge and experience to master, thus making professional financial advice key. Furthermore, even the best advice may not be enough and the general rule of thumb with alternative investing, according to Investopedia, is no more than 10% of your portfolio should go toward these investments."

Many advisers and investment firms saw wisdom in alternative investments after the crisis in 2008 and more than likely, if you don't have alternative investments in your portfolio, your adviser probably discussed them with you.

In fact, if you don't think that "alternative investing" is for you, ask your current adviser if you have any alternative investments in your portfolio (retirement included) or if any of your existing holdings in funds have them. You might be surprised by the response.

The difficulty that I’m having in finding an appropriate bitcoin investment vehicle as an "alternative investment" for a retirement account proves that investing in bitcoins, regardless of what you may believe about them, is a risky business at this point.

There are plans in the works for an exchange-traded fund for bitcoins. Most talked about is an investment that has been associated with the Winklevoss twins. But until this is created, the average investor won't be able to avail themselves of an investment that can be placed in a qualified retirement account.

An accredited investor , though, isn't the average investor.

A favorite author, and a fellow RetireMentor on Marketwatch.com, Mitch Tuchman, wrote about accredited investors and their ability to invest in alternative investments for Forbes:

"It's why hedge fund investors are 'accredited,' that is, they attest to their personal wealth and willingness to lose money in the markets. Accredited is a fancy way of saying you can afford to take a hit.

"Retirement investors can't. No retirement investor should be rolling the dice with the gunslinger managers of Wall Street. The problem with gunslingers is that, eventually, they come face-to-face with a faster gun. Somebody ends up face down in the dust."

So the bottom line at this point is that for the average investor, bitcoins aren't accessible for their retirement account — yet.

My research has shown, though, that the Winklevoss twins aren't the only managers "gunning" to make bitcoin investments available to the average investor through ETFs and other vehicles.

One such investment is the Bitcoin Investment Trust, which is a private, open-ended trust that is invested exclusively in bitcoin and modeled on the popular SPDR Gold Trust ETF GLD, +0.12% There are plans to make the trust available to average investors, but for now, it's only available to accredited investors, who as Mitch says, can "take a hit."

HOW MUCH SHOULD I INVEST?

Most investors have little trouble making an "alternative investment" in their retirement account. The current "rule" of asset allocation calls for having about 5% -10% of your overall investment portfolio to be in "alternative investments" as a compliment to other assets such as stocks and bonds.

Before 2008, alternative investments were discussed strictly as an investment option with “accredited investors,” or those who have over $1 million of assets (exclusive of their home) and an income requirement (has made at least $200,000 for each of the last two years). This was to define the investor who was willing to accept the lack of transparency inherent in most of these investments, and (perhaps more important) could absorb a potential full loss of their investment in these highly risky investments.

Much of this changed after 2008, when investors were searching for investments that had little to no correlation to market swings. Advisors were also anxious to find investment vehicles for investors, who were now no longer enamored with stocks and bonds.

Currently, the "average" investor can add "alternative investments" as a small part of their investment portfolio through investments in exchange-traded funds (notice how many ETFs have been created since 2008?) that invest in REITs and commodities. These "liquid" alternatives gives the average investor the ability to gain more access to "hedge fund type" managers and investment styles then they had in the past, when it was primarily reserved for the wealthy investor.

A method for directly buying bitcoins in a qualified investment account doesn't currently exist. Sure, you can "designate" a non-retirement, investment account for this purpose and buy individual bitcoins but you can't do this in a qualified retirement account.

Bitcoin investment vehicles for the "average investor" such as an ETF investing in bitcoins, which is being touted by the Winklevoss twins, aren't currently available and will require approval by the SEC, which could be a lengthy process.

The only current method for making a bitcoin investment in your retirement account is to have a "self-directed" retirement account and be an accredited investor. The options for the investments to be made in this type of account are limited.

I've researched the few available investment options and have gone through the process of setting up the "self-directed" retirement account. I've also filled out the necessary, and lengthy, paperwork that acknowledges that I'm an accredited investor and have decided that I'll be making the minimum investment into something called the Bitcoin Investment Trust (BIT) and placing that into my retirement account.

The Bitcoin Investment Trust is a private, open-ended trust that invests solely in bitcoins. What that means is that it's an investment that is not currently available through an open market or traded on an exchange, but must be subscribed to through a private placement memorandum and exclusively by accredited investors. The disclaimer information for the investment should be enough to frighten away the most prudent investor: "The BIT is a private, unregistered investment vehicle and NOT subject to the same regulatory requirements as exchange-traded funds or mutual funds, including the requirement to provide certain periodic and standardized pricing and valuation information to investors. There are substantial risks in investing in the BIT."

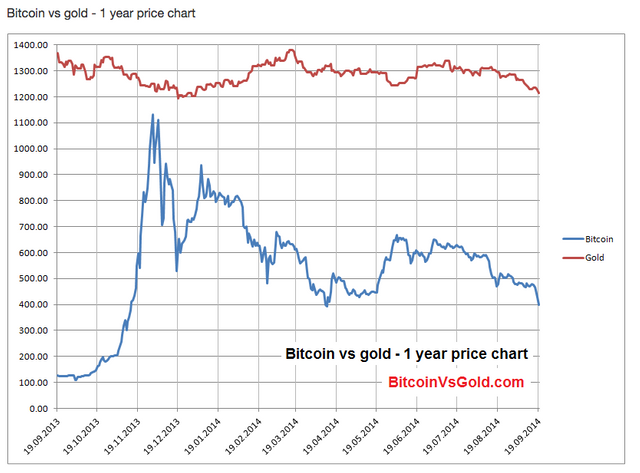

The investment simply buys bitcoins and places them into this "trust.” It's modeled on the SPDR Gold Fund, which takes a similar approach with their gold portfolio, which is available to any investor, in any type of account and is traded through the NYSE.

As an accredited investor in BIT, your investment in this trust gains you a "slice" of this portfolio of bitcoins. If the price of bitcoins increase, your holding increases. If they drop, your investment drops.

Along with investments of this type come rules that you agree to. One rule is that you can't sell your investment for at least one year. After that time, you will actually be able to sell your shares in the OTCQX market, where theoretically, any investor could then buy these shares being offered for sale.

Barry Silbert of SecondMarket, which runs the BIT, describes this sale to the general public, "The people who have already invested, when they decide to sell, they can do so to the public market. So, the amount of shares available to the public market will be dependent on the existing shareholders' desire to sell shares."

What this all means is that although the "average investor" can't currently gain access to an investment such as the BIT, in the future, all investors will potentially be able to buy a bitcoin investment vehicle, even in their retirement account. By that time, the Winklevoss Bitcoin ETF may also be available, providing another bitcoin investment option to the general public.

I guess at this point in time, I'd have to conclude that by having a bitcoin investment vehicle (BIT) in my retirement account, I'm not your “average investor.” It'll be interesting to see what the future holds in terms of making other bitcoin related investment vehicles available for all investors. Until then, I'm stuck with this investment — at least for one year.

The investment that I've made into the BIT is equal to less than 5% of my overall retirement account. Although I admit that I'm nervous about this investment because of its risky nature, I feel that by using effective asset allocation in one's portfolio, it adds diversification and risk (with potential for higher reward, as well as significant loss) without "betting the ranch" and potentially destroying the retirement "nest egg" that I've worked hard to create over the years.

In the next episode, I'll update my holdings after six months, and I'll include some of the "supportive" comments I received from readers,

Remember, you can access Part One of this series here - https://steemit.com/bitcoin/@twaddo/my-role-in-the-revolution-the-story-of-how-i-made-bitcoin-an-investable-asset-part-1

Upvoted

Nice @twaddo

Shot you an Upvote :)

Nice @twaddo

Shot you an Upvote :)

Nice @twaddo

Shot you an Upvote :)

Hi! This post has a Flesch-Kincaid grade level of 13.1 and reading ease of 47%. This puts the writing level on par with academic journals.