The fundamental factors of Bitcoin's price for May 2018

We would like to use a new NVT indicator (Network-Value-to-Transaction) for our May analysis.

Let us start with considering the moving average of the standard characteristics. In this case, the analysis eliminates the change of unutilized transaction outputs, UTXO, since last month's analysis showed their consolidation and restructuring of a number of services to work with new technologies for grouping of transactions.

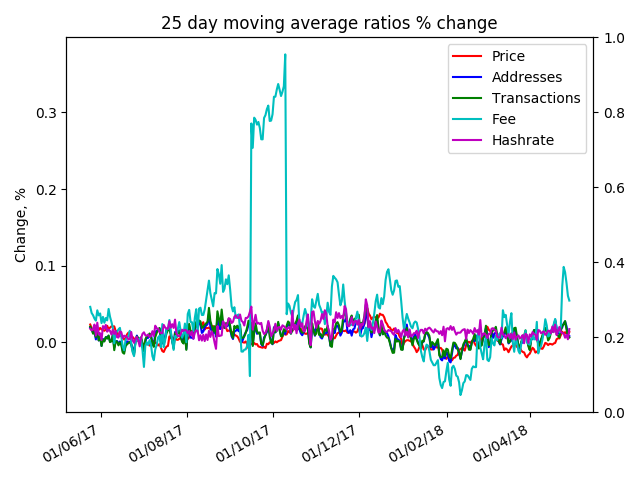

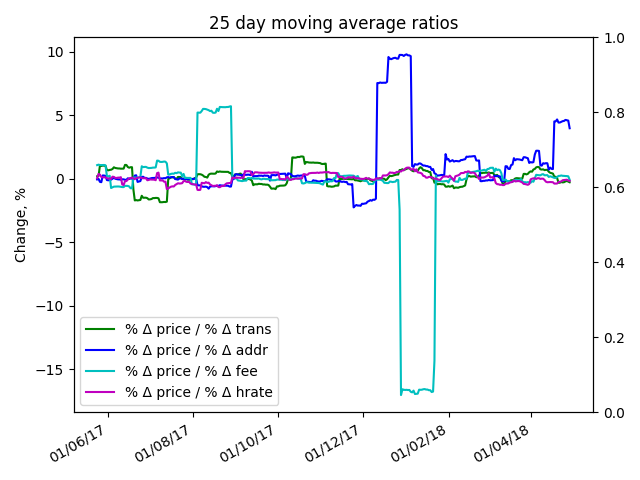

May moving averages by commissions, addresses, transactions, and hash rates

May moving averages by addresses, transactions and hash rates

It is clear from the two graphs that the orders for changing commissions and other characteristics are different. Commissions also show slightly more significant growth by the end of the period, which indicates a further revival of the market. At the moment, new addresses and transactions are also increasing. Miner's mood, both on the monthly change graph and historical data with weekly averaging, do not show signs of optimism.

Derivative characteristics marked a more clear trend in price growth to new addresses. A shorter interval for averaging the graph of unique addresses also shows a small increase, although there is generally no significant increase.

Derivative characteristics of addresses, transactions, commissions and hash rate

Starting in May, we begin to analyze the NVT indicator (additional information on it can be found here). The current NVT values are at the levels of the bubble, which is evidence of weak fundamental characteristics, while network commissions are minimal on a segment of about a year.

Network-Value-to-Transaction и Fee-Value-to-Transaction

Following the increase in volumes in the markets, the volume of trading in Bitcoin futures on CBOE also experienced highs (with not very active daily trades on average). Business publications focused on the fact that in late April, 17 millionth bitcoin was produced.

The price (and trading volume) for Bitcoin futures on the CBOE exchange

MIT Review released a material that describes possible scenarios for the destruction of Bitcoin. The material itself is not worth the analysis if it hasn' t sent by the CBOE. The article shows a relatively low level of possession of the topic, in addition to using unconfirmed data, such as ICO Telegram. The first two options (government attack and replacement by a large social network) are irrelevant to the current state of the network, since a) government pressure on Bitcoin has now been recorded in various forms, and has not had a significant impact on the functioning of the network, b) development Facebook or Telegram of its blockchain projects is still in the field of unconfirmed intentions. The third option says that bitcoin will be replaced by a hundred other specialized tokens. Selected quote:

You are in line at the grocery store. Your phone has a digital wallet in which you can find not only Fedcoin or FacebookCoin, but also AppleCash and ToyotaCash, and a token specifically designed for the store in which you are standing.

It is clear that the author's optimism about the diversity of tokens, in general, is overstated. Most likely, if tokens become the same routine phenomenon as there was a variety of currencies in the 19th century in Europe, then the user will either be burdened by their diversity or face non-illusory transaction costs enriching intermediaries. It's amazing that posts of this level can still be found in MIT Review.

Hardly anyone is using cryptocurrenices to transact, other than trade them on exchanges, thus adoption is VERY low. This tells us cryptocurrencies have peaked (in Dec/Jan) and will remain low for an extended period of time. But it also tells us of other problems brewing....

https://steemit.com/cryptocurrency/@harpooninvestor/the-great-currency-bubble-is-ending-what-will-we-see-from-here-on