A Shariah Analysis of the Adab ICO, Adab Token and the FICE

What is an ICO?

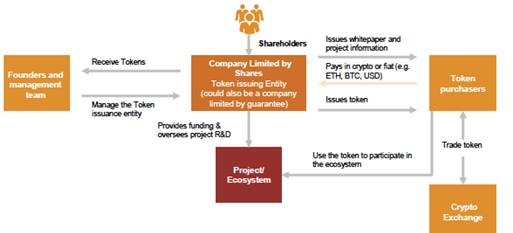

Initial Coin Offerings (ICOs) are a relatively new way to fund start-ups and projects. Similar to an IPO, an ICO is a way for a start-up or an established company to raise capital, and a vehicle of investment for potential investors. Usually, capital and “shares” in cryptocurrency start-ups and projects are represented by tokens. In an ICO, the companies seeking funding sell their cryptocurrency tokens in exchange for financial investment or other contributions; the funding is executed using Bitcoin or other cryptocurrencies. Like in IPOs, ICO investors are generally motivated by the potential future success of the start-up and an increase in value of the tokens issued[1].

Source: PwC (2017), Introduction to Token Sales

Most ICOs are currently based on Ethereum and use the ERC20 standard, which has emerged as the de-facto industry standard for issuing tokens. The ERC20 standard makes the assets more easily interchangeable and ensures they can work with DApps adhering to the same standard. Moreover, the introduction of this standard allows for the tokenization of other features, including voting rights.

Shariah Analysis of an ICO

Similar to an IPO, an ICO is a vehicle to raise funds and capital for a project. Hence, the raising of funds in and of itself is not problematic or questionable. Rather, for Shariah compliance purposes, what needs to be considered is the project for which funds are being raised for. For Shariah compliance, an ICO must be screened like an IPO to ensure it conforms with Shariah norms.

The current industry practice is to filter out as non-compliant any project or company whose core business activity or idea revolves around the following:

- Riba-based conventional financial services (conventional banking and conventional investments)

In Islam, a loan (qard) is considered a gratuitous contract, and it is commendable for a lender to provide a loan to a borrower who is in need of money. Both the Qur’an and Sunnah promise reward to a lender who provides a loan to a person in need. The fact that the Shariah prohibits the lender to derive any conditional benefit from the loan further emphasises its gratuitous nature. It also implies that the loan contract should not be used for profiteering purposes. Thus, any profit or additional return in lieu of the loan is impermissible and non-Shariah compliant. Both the Qur’an and the Sunnah have prohibited the lender from charging the borrower any additional amount. The Qur’an emphasises that the lender is entitled to receive the principal amount. It states:

“O you who believe! Fear Allah, and give up what remains of your demand for usury, if you are indeed believers. If you do it not, take notice of war from Allah and His Messenger. But if you turn back, you shall have your capital sums: Deal not unjustly, and you shall not be dealt with unjustly” (al-Qur’an 2:278–279).

A famous juristic maxim states: “Any loan which draws an increment is Riba” (Ibn Abi Shaybah).

Riba is more than just simple interest and compound interest; Riba is an unjustified excess in a bilateral contract which is stipulated for one of the two transacting parties and is without consideration. To elaborate, there are two types of Riba:

Riba al-Nasi’ah is the advantage and excess gained without consideration by deferring delivery of any homogenous counter exchanges. This excess manifests upon default or delay in payment where time is factored as a consideration.

Riba al-Fadhl is a contractually agreed excess in units without any consideration in an exchange of homogeneous goods.

Shariah has not considered money to be a commodity but a medium of exchange. When money of the same genus is exchanged, it must be on spot and in equal quantity. Exchanging different amounts at different times brings into effect both forms of Riba: Riba al-Nasi`ah and Riba al-Fadhl.

Jabir stated that God’s Messenger cursed the accepter of interest and its payer, and also one who records it and the two witnesses, and he said, “They are all equal.” (Abu Dawud)

Unequal payments in homogenous currencies is tantamount to Riba al-Fadhl. Riba al-Fadhl (known as Riba due to surplus and excess) originates when a Riba item is exchanged for the same item in an unequal amount. These bonds are prone to Riba al-Fadhl.

The exchange of cash payments at different periods results in another type of Riba known as Riba al-Nasi’ah. This refers to the deferral in an exchange of two homogenous Riba items.

The Prophet Muhammad (peace be upon him) said:

“(When) gold is exchanged in lieu of gold, silver is exchanged for silver, wheat is exchanged for wheat, barley is exchanged for barley, dates are exchanged for dates and salt is exchanged for salt; it must be exchanged in equal measure and settled immediately; and if the counter exchanges differ, sell (whichever quantity) as you wish as long as settlement is immediate.” (Sahih Muslim)

Riba is categorically prohibited in the Qur’an. The Quran says,

O you who believe! Remain conscious of Allah, and give up all outstanding gains from usury, if you are [truly] believers; for if you do it not, then know that you are at war with Allah and His Messenger. But if you repent, then you shall be entitled to [the return of] your principal. You will do no wrong, and neither will you be wronged. [Surat Al-Baqarah, 278–279]

Prophet Muhammad (peace be upon him) said:

“Cursed is the one who takes interest, and the one who pays it, the one who records it, and the two who (accept to be the) witnesses for signing it.” (Muslim)

- Trading in Gharar (uncertain/contingent) -laden subject matters (uncertainty)

The Prophet Muhammad (peace be upon him) prohibited bay’ al-gharar (uncertainty) (Sahih Muslim). The scholars of Islam state that this narration refers to trades harnessing major uncertainty as well as the actual trading and transfer of risk[2]. Risk is not a tradable commodity. Thus, the Prophet Muhammad clearly prohibited trading and exchanging risk. In prohibiting Gharar, the Shariah has also prohibited the trading of risks, and thereby, prohibiting derivative instruments designed to transfer risk from one party to another.

- Gambling, Qimar and Maysir activities

The Qur’an states:

“They ask thee concerning wine and gambling. Say in them there is great sin and some benefit for men. The sin is greater than the benefit.” (Qur’an 2:219)

“O believers! Intoxicants and gambling, worshipping stones and divination by arrows are impure, of Saytan’s handiwork: refrain from such abomination that ye may prosper. “

(Qur’an 5:90)

Abu Hurayrah narrates that the Prophet Muhammad forbade transaction determined by Hasah and Gharar. (Muslim)

Hasah is a transaction contracted on chance. Hasah linguistically means pebble or small stone. An example of hasah is when a person says to a customer “I will sell you the items on which your pebbles fall”. It is clear that the transaction is based on an unknown outcome and therefore has uncertainty in the subject matter of the contract. Thus, it is non-compliant with Shariah.

- Alcohol and prohibited beverages

The Qur’an states:

“O you who believe! Alcohol (khamr), gambling, dedication of stones, and divination by arrows are an abomination (impure) of Satan’s handiwork. So abstain from such (abomination) that you may prosper.” (al-An’am, 90).

Satan wants only to excite enmity and hatred between you with intoxicants (alcoholic drinks) and gambling, and hinder you from the remembrance of God and from The Prayer. So, will you not then abstain?” [Qur’an 5:90–91]

Abdullah Ibn Umar narrates that Prophet Muhammad said: “Every intoxicant is Khamr and every intoxicant is Unlawful (haram)…” (Sahih Muslim)

- Pork related products and non-halal food production, packaging, processing or any direct activity linked to unlawful consumables

Pork is expressly forbidden in the Qur’an:

“He has forbidden you Maytah (dead animals), and blood, and the flesh of swine…” [Qur’an 2:173]

- Tobacco-related products

It is a factual reality that smoking harms one’s health. We have been instructed by God to not destroy ourselves with our own hands and actions:

“And make not your own hands contribute to (your) destruction.” (Qur’an 2:195)

Some scholars have argued that tobacco qualifies as al-Khaba’ith (filthy substances) which was prohibited in the following verse:

“He allows At-Tayyibaat (i.e. all good and lawful as regards things, deeds, beliefs, persons and foods), and prohibits Al Khabaa’ith (i.e. all evil and unlawful as regards things, deeds, beliefs, persons and foods) [Qur’an 7:157]

“Eat and drink but do not waste by extravagance, certainly He does not like those who waste by extravagance.” (Qur’an 7:31)

- Illicit adult industry (pornography)

Pornography and illicit relationships have been deemed shameful and indecent in Islamic teachings. The following verses in the Qur’an explicitly prohibit such activities:

“Surely God enjoins justice, kindness and the doing of good, to kith and kin; and He forbids all that is shameful, indecent, evil, rebellious and oppressive.” (Quran 16:90)

“And do not come near to adultery, for it is a shameful deed and an evil, opening the road (to other evils)” (Qur’an 17:32).

“Verily those who love that indecency should spread among the believers deserve a painful chastisement in the world and in the Hereafter. Allah knows, but you do not know.” (Quran 24:19)

- Unlawful entertainment

The AAOIFI Standards have excluded the music and cinema industry from their screening criteria. A number of scholars view this industry as non-compliant.

An ICO which does not raise funds for a project centred on the above has potential to be Shariah compliant.

The Adab ICO

The objective of the ICO by Adab Solutions is to raise funds to develop and scale the First Islamic Crypto Exchange (FICE). The idea of a Shariah compliant Crypto Exchange is a permissible venture based on the opinion of permissibility of cryptocurrencies, therefore, such an ICO is Shariah compliant.

The Adab Token

The Adab token is a crypto-asset. Crypto-assets are digital assets recorded on a distributed ledger. They derive their name from the cryptographic security mechanisms used within public, permission-less distributed ledgers[3].

There are different types of crypto-assets, which can be classified as the following:

- Cryptocurrencies:

Although cryptocurrencies are used as a blanket term for all crypto-assets, however, for the sake of clarity, we use the term cryptocurrencies for a subset and type of a crypto-asset. Cryptocurrencies are meant to constitute a peer-to-peer alternative to fiat currency, with a general purpose of being a medium of exchange.

- Tokens

As opposed to cryptocurrencies which are designed to function as a general-purpose medium of exchange across applications, tokens are designed to support a more narrowly-defined, specific use case. Tokens are categorised in the following manner:

- utility tokens

The utility tokens are rights to services or units of services that can be purchased. These tokens can be compared to API keys, used to access the service[4].

- Commodity token

These tokens are digitasation of commodities to be exchanged and traded on a trading platform.

- Equity token

Equity tokens are said to represent equity in the issuing company, giving token holders votes as shareholders, participation in future dividends, and a beneficial interest in the company. These tokens are similar to purchasing shares in a company.

Shariah Analysis of Crypto-Assets

In order to trade lawfully in Islam, the commodity must qualify with the following:

Mal (wealth)

Taqawwum (lawful)

The primary component for any counter value or consideration is Mal. An accepted definition of a transaction among Muslim jurists is ‘an exchange of Mal in consideration of Mal’ (al-Hidayah).

Some of the common definitions of Mal are:

Mal is what human instinct inclines too and which is capable of being stored for the time of necessity (Hashiya ibn Abidin).

Mal is that which has been created for the goodness of human beings. Mal brings with it scarcity and stinginess (Fiqh al-Buyu’).

Mal is that which is normally desired and can be stored up for the time of need. (Majallah, 2012)

Any consideration in a commutative contract must be Mal. If the consideration is not Mal, the contract is void (batil). Therefore, the first fundamental requirement for the permissibility of a crypto-asset and token is for it to be Mal.

In order to profit and lawfully trade in crypto-assets, they must have Taqawwum. Taqawwum refers to the lawfulness of the commodity or entity from a Shariah perspective.

We learn from the above that for Adab token to be a compliant tradeable token, it must be desirable and storable to qualify as Mal. Adab tokens are clearly desirable as they have beneficial use cases on the FICE and there are a number of investors interested in purchasing these tokens. Furthermore, the Adab token is storable and retrievable through one’s digital wallet. Hence, it can be concluded that the Adab token is Mal.

Another factor to consider is Taqawwum. According to Islamic law, all items and transactions are deemed lawful (‘Ibahah) unless there is clear evidence to assume otherwise. Considering this principle and that the Adab token is a digital asset not representing any unlawful asset or utility, it has nothing inherently unlawful about it. The Adab token is a means of paying commission charges on the FICE and a key to access the services on the platform. Hence, the Adab token has Taqawwum also.

Thus, from a Shariah compliance perspective, it can be concluded that the Adab token is Mal and is Mutaqawwim. This makes the Adab token a Shariah compliant crypto-asset.

Smart Contracts

The Adab token uses smart contracts. Ethereum allows developers to program their own smart contracts, or ‘autonomous agents’, as the Ethereum white paper calls them. The language supports a broader set of computational instructions.

Smart contracts can:

· Function as ‘multi-signature’ accounts, so that funds are spent only when a required percentage of people agree

· Manage agreements between users, say, if one buys insurance from the other

· Provide utility to other contracts (similar to how a software library works)

· Store information about an application, such as domain registration information or membership records.

Smart contracts help you exchange money, property, shares, or anything of value in a transparent, conflict-free way while avoiding the services of a middleman[5]. Smart Contracts[6] are executable code contained within transactions on a blockchain that execute predefined rules based on a set of conditions (i.e. “contracts”). SCs, therefore, are transaction protocols by definition; they move assets between parties reliably based on programmed instructions[7]. Considering this, the use of smart contracts are permissible on condition that the actual protocols do not violate any Shariah principle.

Shariah Principles for the Exchange

The FICE will be governed by two fundamental principles:

- Barring of all non-Shariah compliant securities

The Adab FICE will not permit any non-Shariah compliant securities to be traded such bonds, derivatives, conventional ETFs, warrants, optiond etc.

- Barring of all non-Shariah compliant trades, contracts and investment strategies

The Adab FICE will not permit trading options, leveraging, margin, rollovers or short-selling.

Every facility on the Adab FICE platform will be reviewed from a Shariah compliance perspective to ensure Shariah compliance. There will be an ongoing review and audit of Adab by the Shariah Supervisory Board in conjunction with the Internal Shariah Compliance Officer, Mufti Faraz Adam.

[1] Deloitte (2017), ICOs — The New IPOs, Available from: https://www2.deloitte.com/content/dam/Deloitte/de/Documents/Innovation/ICOs-the-new-IPOs.pdf

[2] Al-Maghribi (1119 AH), al-Badr al-Tamam Sharh Bulugh al-Maram, Dar Hijr

[3] EY (2018) ‘IFRS: Accounting for Crypto-Assets’, Available online: https://www.ey.com/Publication/vwLUAssets/EY-IFRS-Accounting-for-crypto-assets/$File/EY-IFRS-Accounting-for-crypto-assets.pdf

[4] Benoliel, M. (2017), Understanding the difference between coins, utility tokens and tokenised securities [online], Available from: https://medium.com/startup-grind/understanding-the-difference-between-coins-utility-tokens-and-tokenized-securities-a6522655fb91

[5] Joshi, D. (2017), As financial institutions invest in blockchain tech, how secure is your information?, Business Insider UK [online], Available from: http://uk.businessinsider.com/secure-cryptocurrency-blockchain-technology-2017-10

[6] A smart contract, also known as a cryptocontract, is a computer program that directly controls the transfer of digital currencies or assets between parties under certain conditions. A smart contract not only defines the rules and penalties around an agreement in the same way that a traditional contract does, but it can also automatically enforce those obligations. It does this by taking in information as input, assigning value to that input through the rules set out in the contract, and executing the actions required by those contractual clauses — for example, determining whether an asset should go to one person or returned to the other person from whom the asset originated. These contracts are stored on blockchain technology, a decentralized ledger that also underpins bitcoin and other cryptocurrencies. Blockchain is ideal for storing smart contracts because of the technology’s security and immutability.

[7] Little, W. (2017), A Primer on Blockchains, Protocols, and Token Sales, Available from: https://hackernoon.com/a-primer-on-blockchains-protocols-and-token-sales-9ebe117b5759

Facebook — Twitter — Reddit — Steemit — Telegram group — Telegram channel

#Adab #Muslims #investments #cryptoeconomy #Islamic #finance #cryptocurrency #exchange#FICE#Shariah#trading#cryptocurrencies#Muslim #community

The Adab team has done a great job, which resulted in success in raising funds during the IEO. This is an important event that can spur the development of the project, strengthening its pace!