It’s Time to Prepare for More Interest-Rate Pain – Australian Property Market Update for the Week Ending 2 July 2017

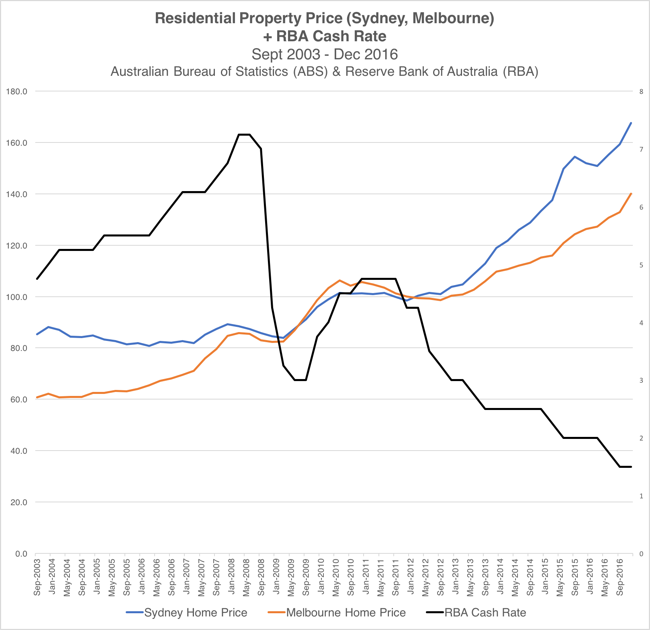

The Reserve Bank of Australia (RBA) met this week and decided to leave the cash rate on hold at a record-low 1.50%. Since the RBA began cutting rates aggressively back in 2012, you can see in the following graph what’s happened to home prices in Sydney and Melbourne.

The RBA’s latest move should be of little consequence to property investors. If anything, rates will only go lower. If the RBA chose to raise the target cash rate now, they would decimate the economy.

The truth is, raising interest rates would only serve to more closely align the cost of borrowing money with supply, demand and risk. If the RBA stopped buying debt altogether, and let the free market decide the cost of money, interest rates would spike, probably up to the historical mean of 8 or 9 percent. The economy would grind to a halt, like a heroin addict without drugs writhing in pain on a bed.

The industry regulator that property investors should really be worried about is APRA – the Australian Prudential Regulation Authority. Their stated role is to hold banks accountable to not taking on too much risk. The truth is, they actually exist to direct the flow of the RBA’s easy money.

Lately, they’ve been trying to stop home prices from rising further by directing the flow of credit away from housing. They’ve done so by forcing banks to make it harder for property investors to borrow money.

First, they put a speed limit on the growth of banks’ investor mortgage portfolios, capping the growth at 10 percent per year. Anyone who can do math would know that is still a very high level of growth and will do very little to slow down home price growth.

APRA’s greatest fear is that they apply the brakes too quickly, and home prices come crashing down. That would annihilate our entire economy, as many homeowners are deeply indebted by their mortgage.

So the next gentle tap on the break has been forcing banks to reduce the percentage of interest-only loans they carry from 40 percent to 30 percent of the total. Aussies, especially investors, love interest only loans. Hyman Minsky is rolling over in his grave.

But 30 percent is still a significant portion of the whole, so APRA’s changes have done very little to stop the RBA’s easy money from flowing into housing.

I’ll pause with the overview here to give an update on recent auction clearance rates and price movements, then pick the topic of APRA back up at the end of this post to wrap things up.

The Latest Preliminary Auction Activity

If you missed the video in last week’s update showing what an Aussie property auction looks like, here it is again:

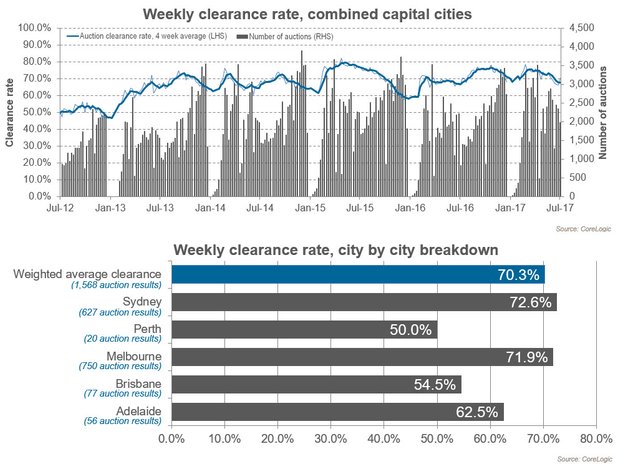

The auction clearance rate is a measure of the percentage of auctions that have found a winning bidder. Because it considers both supply and demand, it’s a helpful snapshot of how the market is moving week-on-week.

Here are the latest preliminary results from CoreLogic for the Australian capital cities:

source

Both Melbourne and Sydney remain above 70 percent, which is usually a result indicative of rising home prices. In the other capital cities, auctions are not proving as successful.

It’s important to note that auction volume is declining as we head into winter. With fewer upcoming auctions, buyers will likely be competing more aggressively.

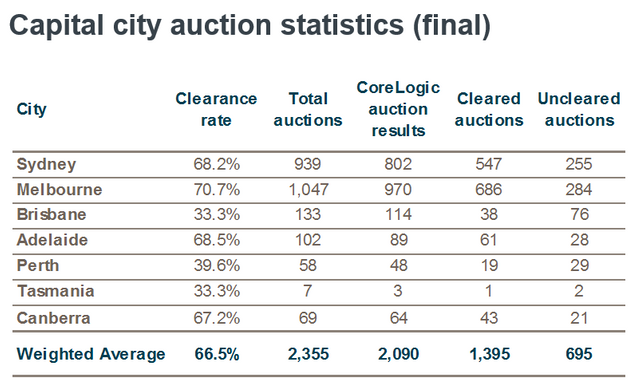

Last Week’s Final Auction Results

Last week’s nationwide clearance rate of 66.5 percent was the lowest since June 2016. Only Melbourne buyers managed to lift the clearance rate above 70 percent.

Here are all the final capital city results for last week:

source

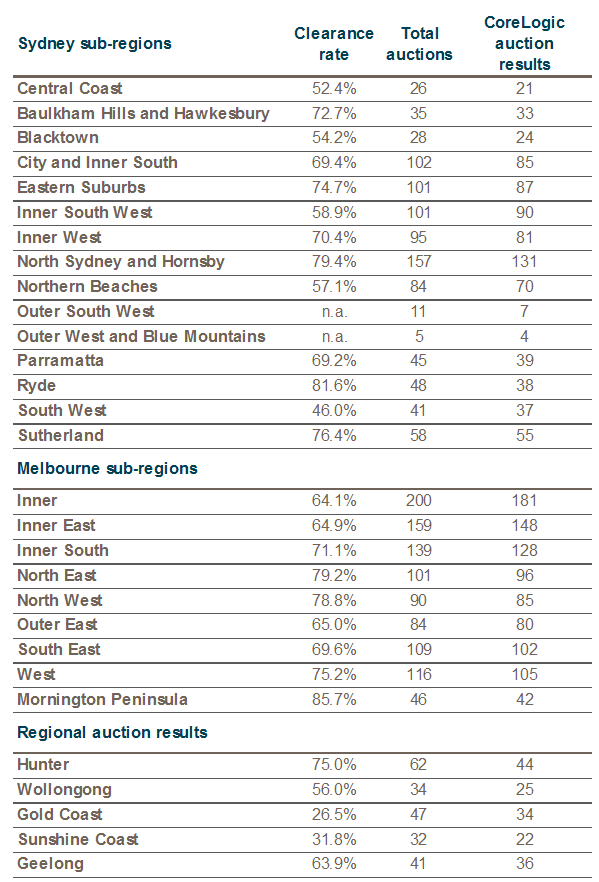

Here are the results for the Sydney and Melbourne sub-regions, plus some key regional areas:

source

Recent Changes in House Prices

Here’s the interesting point…

Last week I reported that Sydney and Melbourne home prices peaked in April and then took a breather for a few months before beginning to climb again. This week, both cities blew past those April highs to record even higher highs. In fact, this week, Sydney continued its climb and Melbourne prices jumped another full 2 percent.

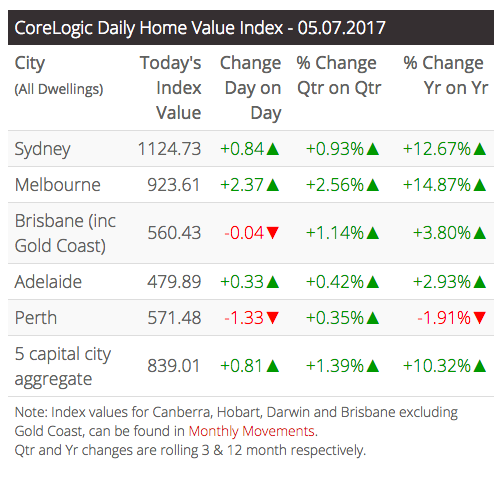

As you can see in the following chart from CoreLogic, home values across the country are up over 10 percent in the last twelve months. All five major capitals are in the green for the quarter. Only Perth remains down on the year.

source

Market Summary

Now back to APRA…

Even as they’ve been tightening the screws on property investors, or at least trying to give that appearance, home prices are still rising. In fact, they’ve never been higher, having just broke through their April peak.

The RBA can’t afford for home prices to go much higher. They know that their only hope in fixing the economy is to continue cutting the cash rate to spur on inflation, and hopefully wage growth, to inflate this housing debt bubble away. The alternative is deflation and a property collapse, which no one wants to even think about the consequences of.

That means the RBA desperately needs APRA to flatten out home prices, and direct more credit away from property investors. That’s why investors should expect their interest-only and even principal plus interest loan interest payments to rise. In short, investors should be preparing now for more interest rate pain.

Within the next few weeks, APRA is expected to announce a fresh round of even tougher bank capital requirements to comply with international banking regulations set in the Basel Accord.

According to Investopedia…

The Basel Accords are three sets of banking regulations (Basel I, II and III) set by the Basel Committee on Bank Supervision (BCBS), which provides recommendations on banking regulations in regards to capital risk, market risk and operational risk. The purpose of the accords is to ensure that financial institutions have enough capital on account to meet obligations and absorb unexpected losses.

You can bet that property investors will bear the brunt of these upcoming changes as they get hit with higher interest rates.

Although home prices are still rising, APRA remains a formidable foe to investors who expect home prices to continue rising. Remember, Australians are already deep in the hole. As @nolnocluap pointed out in this post, household debt as a percentage of disposable income just surpassed 190 percent. There’s a point at which debt growth is no longer sustainable.

The million-dollar question is, where is that point? Whenever we hit it, home prices must at least stop growing, banks stocks will likely fall, and we’ll feel a shockwave of some kind through our entire economy.

What are your thoughts on the Australian property market?

As I mentioned in my last post, my wife is overseas and I’m on daddy duty while also running a business, which explains why my posts have been few and far between lately. I’m hoping to pick up the pace soon. Thanks for bearing with me.

Jason Staggers

It is a bit complicated for me but thank you for your advice. I will follow you because I love finance and your blog is very interesting. Good job.

Thanks for the feedback. I'll try to keep that in mind in the future.

It's a pleasure me that i just read your post on time thank you for such a great info

Interesting article ! Just upvoted you.

If you are interested in Stocks, Cryptos, P2P Lending, Real Estate and investing in Science check out my blog.

Best regards,

Alex

This post has received a 2.56 % upvote from @booster thanks to: @jasonstaggers.