Philippines Tax Updates: TRAIN LAW and the Minimum Wage Earners

TRAIN LAW and the Minimum Wage Earners

TRAIN Law was signed into law last December 21, 2017 with the hope of unburdening the middle classes of the high taxes to their income. It is the government's tool to bolster its tax collection and increase it revenue to fund major infrastructure projects. Furthermore, TRAIN Law is expected to help alleviate those people in poverty through government services which will be, again, funded by the increased revenue from this new tax package.

In my previous post Philippines Tax Updates: Personal Income Tax (TRAIN LAW) it discussed how the new tax law will affect compensation earners, SEP, and mixed income earners. It was mainly focused on the middle classes. If the new tax law has something to say to the middle income earners, how about to the minimum wage earners? What does these amendments to the Tax Code has to offer to minimum wage earners?

Who are the Minimum Wage Earners?

"(HH) the term 'minimum wage earner' shall refer to a worker in the private sector paid the statutory minimum wage, or to an employee in the public sector with compensation income of not more than the statutory minimum wage in the non-agricultural sector where he/she is assigned." (R.A. 9504 Sec. 1)

Minimum wage earners are people earning within the statutory minimum wage that are fixed by the Regional Tripartite Wage and Productivity Board (RTWPB) of the Department of Labor and Employment (DOLE).

The RTWPB of each each region are the ones who fixed the statutory minimum wage (wage rates) in the different regions based on established criteria. The wage rates that they will fixed in each region will now become the bases for tax exemption from income tax.

"Provided, That minimum wage earners as defined in Section 22 (HH) of this Code shall be exempt from the payment of income tax on their taxable income: Provided, further, That the holiday pay, overtime pay, night shift differential pay and hazard pay received by such minimum wage earners shall likewise be exempt from income tax. (RA 9504 Sec. 2)

A minimum wage earner is exempt from income taxes as long as he/she satisfy the requirement of being a minimum wage earner.

Sample Computation

Mr. Kulangot is a factory woker. He is a minimum wage earner earning 300Php a day in ARMM Region. During the month he receive 7 200 minimum wage, 2 000 hazard pay, 1 000 holiday pay, 500 night shift differential pay and 1 000 overtime pay.

Mr. Kulangot also had a business. During the month he earned from his small business an amount of 300 000.

| Income | Non Taxable | Taxable |

|---|---|---|

| Minimum Wage | 7 200 | - |

| Overtime Pay | 1 000 | - |

| Holiday Pay | 1 000 | - |

| Night Shift Differential | 500 | - |

| Hazard Pay | 2 000 | - |

| Business Income | - | 300 000 |

1Mr. Kulangot is an MWE hence all his income that are exempted by the law are non taxable. If Mr. Kulangot has other income aside from the wages, like business income, such other income will be taxed accordingly but preserving the non taxability of all his minimum wages exempted by the law.

2Supreme Court ruled out RR 10-2008. RR 10-2008 states that MWE earning other income, except income subject to final tax, besides his minimum wage, all of his other income including his minimum wage will be subjected to tax. SC made a new ruling that overruled RR 10-2008 that does not limit an MWE's exemption. Hence, if MWE earns other income aside from his minimum wage, his minimum wage will still be exempted, all other subject to tax.

What does TRAIN Law amended in the Old Tax Code for Minimum Wage Earners?

The answer is : NONE

RA 9504 amended RA 8424 (NIRC) in which minimum wage earners have become tax exempted on their income as minimum wage earners. RA 10963 (TRAIN Law) did not amend anything with respect to minimum wage earners. The provision of minimum wage earners in the Old Tax Code will still apply.

What does TRAIN Law brought for Minimum Wage Earners?

CONS:

1. Train Law give minimum wage earners high commodity prices.

This increase in commodity prices brought by increase in excise taxes will be discussed sooner.

PROS

1. Minimum Wage Earners may now agree to be promoted or have a wage increase

What does this mean?

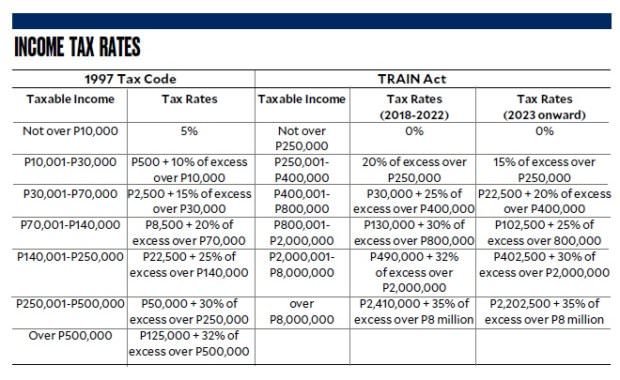

It is a common practice in the past that MWE don't want to be promoted or have a wage increase in order to keep their status as Minimum Wage Earners. Before the TRAIN Law, the bracketing of taxable income for individuals is so small that even low income earners (not MWE) can't escape taxes.

Take a look at the picture below:

It is a dilemma of MWEs when it comes to wage increase. Try to imagine a MWE earning minimum wages, suddenly his employer will increase his wage by just Php5 and because of the increase his MWE status will be forfeited and he will now be subjected to regular income tax, unlike before he was exempted. Let's say a Php 5 increase in daily wages and the result will be a Php 20 Tax Withheld.

Example (Using the Old Tax Table):

Mr. Kulangot (single with no dependents) is a factory woker. He is a minimum wage earner earning 300Php a day which is the Statutory Minimum Wage set by RTWPB in Zamboanga Region. During the year he receive Php 93 600 minimum wage, 10 000 hazard pay, 5 000 holiday pay, 10 000 night shift differential pay and 10 000 overtime pay.

| Income | Non Taxable | Taxable |

|---|---|---|

| Minimum Wage | 93 600 | - |

| Overtime Pay | 10 000 | - |

| Holiday Pay | 10 000 | - |

| Night Shift Differential | 5 000 | - |

| Hazard Pay | 10 000 | - |

| Tax Due and Payable to BIR | -0- |

3Since Mr. Kulangot is a MWE all his earnings in consonance with the law are non-taxable. Hence, he has a zero tax due to the BIR

Let us further assume that the employer of Mr. Kulangot and Mr. Kulangot agreed to a wage increase of Php 5 per day. So he's daily wage now is Php 305. And all others remain constant.

Basic Wage of Mr Kulangot (312 days * 305Php): Php 95 160/ annum

| Income | Non Taxable | Taxable |

|---|---|---|

| Basic Wage | - | 95 160 |

| Overtime Pay | - | 10 000 |

| Holiday Pay | - | 10 000 |

| Night Shift Differential | - | 5 000 |

| Hazard Pay | - | 10 000 |

| Tax Due and Payable to BIR | 10 532a |

aAll income = 130 160; less personal exemption 50 000. Taxable Income = 80 160 .. 10 160* 20% = 2 032 add fixed tax of 8 500 .. Tax Due = 10 532

b10 532/312 = Php 33 pesos of Mr. Kulangont's income goes to taxes.

cStatutory deduction ignored for simplicity.

Since Mr. Kulangot agreed to the wage increase and his wages is above the rate fixed by the RTWPB, which is Php 300, Mr. Kulangot has no choice but is to be subjected to income tax. He received a wage increase of Php 5/day but the sad part is he will be deducted Php 33/day for tax withheld.

Now if you are a MWE do you like a salary increase before the TRAIN Law? Of course NOT!

But what will happen if Mr. Kulangot agreed to the wage increase during the effectivity of the TRAIN Law? Let's compute!

| Income | Non Taxable | Taxable |

|---|---|---|

| Basic Wage | - | 95 160 |

| Overtime Pay | - | 10 000 |

| Holiday Pay | - | 10 000 |

| Night Shift Differential | - | 5 000 |

| Hazard Pay | - | 10 000 |

| Tax Due and Payable to BIR | 0d |

dAll income = 130 160. Based on TRAIN Law new Tax Table Income below 250 000 are 0% rated. Hence, Mr. Kulangot will pay 0 taxes to the BIR.

Now can you see the magic?

Before the TRAIN Law a Php 5 increase to Mr. Kulangot's wages will result to an annual tax of 10 532. But during the TRAIN Law's effectivity, even if Mr. Kulangot cannot be considered a MWE still his income is zero rated in the new tax table. Thus, Mr. Kulangot can now agree to promotion, and wage increase.

2. Minimum wage earners (MWE) will always be minimum wage earners even if their income is high as long as it is the rate fixed by RTWPB.

Even if they lose the MWE status the regular tax table is still favorable for them.

Conclusion

To sum up everything, although TRAIN Law was not so explicit in its provisions about the MWE; TRAIN Law have a silent provision that MWE can take advantage of. An MWE can sacrifice loosing the Minimum Wage Earner status as long as his income is below the zero (0%) rated Php 250 000.

- http://www.lawphil.net/statutes/repacts/ra2008/ra_9504_2008.html

- http://www.bworldonline.com/content.php?id=140690§ion=Economy&title=sc-nullifies-minimum-wage-earners-tax-exemption-limits

- https://www.pwc.com/ph/en/tax-alerts/2017/tax-alert-12.html

PS: I am open for correction. Please comment if you have any questions or voilent reactions. Feel free to comment because it is free. This topic really is exhausting but I love steeming.

Your Lovely Accountant Steemian

This new law will help those minimum wage earners. No more tax for them and they can now bring extra income for their families. It's so beneficial for them.

The new law has nothing to do with the MWE. RA 10963 did not amend anything to what RA 9504 amended to RA 8424.

RA 9504 made MWE exempt from income tax.

Congratulations! This post has been featured in our Daily Featured Posts. Continue putting out high-quality content articles on this platform and you will surely succeed!

Thank you for featuring my post. I will dedicate all my strength in steeming :)

TRAIN Law diay tawag ani nga law sir? hehe

karun pako kabalo. Thanks for this. :)

Yes.. RA 10963.. Section 1 Stating that this law is also called (TRAIN) Tax Reform Acceleration and INclusion Law

ohhhhh. unsaon nlng ug mag Law ko ani hinay kaau ko sa taxation. hahaha