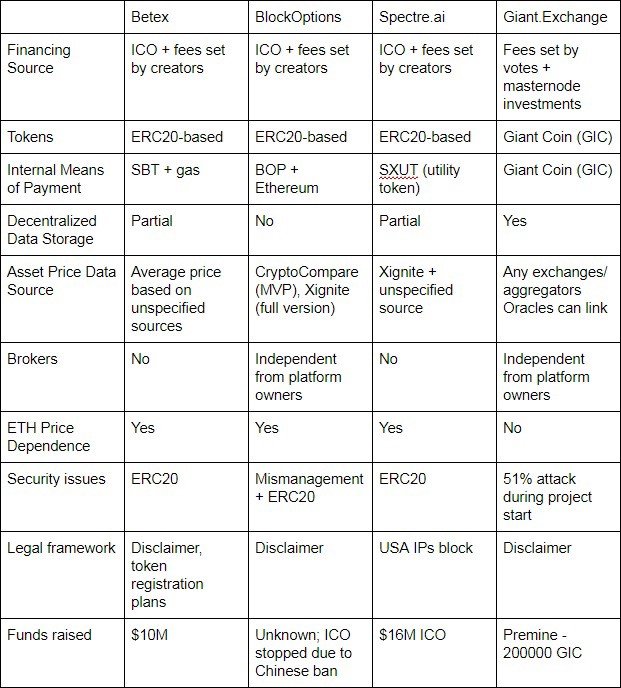

Blockchain Binary Options Platforms: Comparative Analysis

The binary options sphere is suffering from various fraud schemes connected with false identities, tampering with the process of option purchases and Web client manipulation techniques. Naturally, the idea to use blockchain as a foundation a new options platform was bound to emerge - and we can already see several offerings on this prospective market.

In this material, we are going to review several platforms that resemble the upcoming Giant.Exchange in goals and features, see the main differences, pros and cons of each one from the list:

- Betex (active MVP launched Q4 2017, token sale launched in 1 March 2018)

- BlockOptions.io (inactive, token sale launched 25 August 2017)

- Spectre.ai (active, token sale first announced 28 September 2017)

- Giant.Exchange (blockchain launched 8th May 2018)

Let’s look at the main review criteria.

- Financing source

- Tokens

- Internal means of payment

- Decentralized data storage

- Asset price data source

- Brokers

- ETH price dependance

- Security issues

- Legal framework

- Funds raised

Financing Source

The project team motivation can depend on the primary means of financing. Initial coin offerings (ICOs) are held before the product is made. Internal operational commissions, on the other hand, are not possible to implement without the project itself. In ICOs, the audience reaction can be based on announcements only. Fees are less dependent on hype.

Let’s start with fees - amount of money charged for various operations.

Betex. There are various types of commissions which can potentially discourage customers. The first mentioned in the White Paper is the fee imposed for the purchase of SBT token for other digital currencies - 40,000 gas or around $1. The same amount will be charged for a reverse operation - changing SBT to BTC, ETH or other cryptocurrencies. The betting fee will range from 20,000 to 240,000 gas ($0.32-$0.64). The ‘bet basket’ closure will be around 45,000 gas or $0.12. SBT tokens income payouts are to be charged with 80,000 gas or $0.21 in case of one winner. Amusingly, there is also a ‘referral rewards payout’ fee the size of which has been described as ‘still unknown’ - if the developers don’t know the amount of imposed fees, who else will? The project has held its own ICO.

BlockOptions. The planned charge is 0.005-0.01 ETH per opened trade, and the developers do not hide the fact that this is going to be the main source of the platform income. The project has also started its own ICO but ultimately failed due to Chinese ICO ban (see more in the Funds Raised section).

Spectre.ai. fees are not paid for the opening of trade positions, although each trading process will have a fee of 4%, of which 2% goes to the platform and 2% — to SXDT holders. And, again, this project has, too, held its own ICO.

Giant.Exchange. Fees will be imposed in GIC for opening smart contracts. The default marketplace fee is 1%. The same amount is taken from brokers in ‘traders vs. traders’ options and oracles for the creation of their smart contracts. This initial ‘1+1+1’ scheme makes 3% of total finance going to the platform budget stored on the ‘Giant.Exchange’ smart contract.The fees of Giant.Exchange will be defined on a separate vote held simultaneously with the release of the platform. Masternode owners will have vote multiplicators, yet common users will be able to participate as well. If the community decides so, the fees may either become big or small. The decisive factor is the further well-being of the platform all parties are interested to keep. As the project stakeholders, masternode owners are interested in keeping a reasonable fee size.

Another way to attract financing is also worth mentioning. Cryptocurrency-related projects sometimes hold promotional campaigns with the help of affiliates - in exchange for promotion, they get rewards. Let’s see how the reviewed platforms have implemented this idea.

When it comes to Betex, it seems that they have decided not to use this ad scheme at all. The White Paper of Block.Options mentions affiliates who “send new traders to BlockOptions.io's Platform and get paid with ETH from affiliate smart contract”, although they don’t show any examples of this smart contract. On Spectre, the reward depends on the quantity of trades which happened thanks to the effort of the affiliate — ‘50% of Spectre's 2% fee per trade, and additional bonuses based on active promotions’.

Judging by the current state of the projects (see the token stats above), Spectre has managed to establish a good affiliate program, while Block.Options has only described this possibility. If implemented at all, it was unpopular.

Giant has held several bounty campaigns but we never viewed this process as a main tool to attract more customers. In our view, the actual work on Giant.Exchange is much more important. After release, the market will adequately assess the results of this work without the help of paid promotion.

Tokens

The overwhelming majority of the platform tokens are based on the popular ERC20 standard. This led us to use Etherscan as a reliable source of information regarding the current state of these projects.

Betex tokens (SBT) have only 436 holders at the moment of writing and a small transfer count - 1072. BlockOptions has a similar picture - 429 addresses and 1049 transfers. This dramatically differs with Spectre.ai. The platform has two separate tokens for rewards (SXDT, 5574 holders and 36731 transfers) and utility purposes (SXUT, 3733 holders and 20408 transfers). Note that several addresses may belong to the same person and in reality the numbers can be a bit lower. When it comes to transfers and holders, Spectre.ai looks like an obvious leader.

Listing on Coinmarketcap may not be the most deciding factor of the binary options platform evolution, yet this platform has become quite a respected price source. Neither Betex nor BlockOptions can be found there, and again, Spectre outplays them: SXDT and SXUT are both present on this site. Interestingly, they both have not left the first thousand of most capitalized coins even though the days of initial launch hype are clearly in the past.

It is also interesting to look at how the three platforms view their own tokens. According to Betex White Paper, the dev team doesn’t consider their token a security. Later in the text, the potential investors are described as long-term holders aiming to share profits (40% to brokers, 50% to the platform) gained from third parties. This fully corresponds with the classic Howey test which originated in 1946 long before any digital tokens were even made. Note that just like you, we don’t know where the remaining 10% of profits goes - the information on profits comes from Page 11 of their White Paper.

BlockOptions see their ERC20 token quite similarly to how we see Giant Coin - the main tool of dividends and a digital means of payment. Despite this, BlockOptions still gains fees in Ethereum (ETH) which is mentioned in the same material. Meanwhile, on Betex the fees are made in gas - Ethereum operation execution fee units. On Giant.Exchange, Giant Coin (GIC) will be the main commission unit, just like SXUT on Spectre.ai. One thousand Giant Coins which create a masternode share some properties with the SXDT token, for example, the exchange budget distribution participation. This aside, every masternode receives a block validation reward.

Internal Means of Payment

The important component of any crypto trading platform is its internal means of payment. Developers can choose to use a cryptocurrency or a token and thus greatly increase its liquidity. But, as we have just seen from the token stats above, introducing the digital payment tool itself does not guarantee that the project will be widely popular. Regardless, let’s see how the reviewed projects implemented this.

Betex. Founders claim it uses SBT as the main tool of rewards for traders who made the right move.

BlockOptions. Has an ERC20-based tool called BOP used on par with Ethereum.

Spectre.ai and Giant.Exchange. As mentioned at the end of the last paragraph, there are fee tools made by the creators of both platforms. GIC and SXUT can also act as a means of payment between the participants of binary options trading.

Decentralized Data Storage

If the platform is overly-centralized, the funds can easily be snatched by the hackers or even the rogue managers. The reviewed marketplaces have a different approach towards how to store the money of the customers.

Betex. Developers claim that in comparison to usual binary options platforms, its smart contract system has made the automatic withdrawal of funds possible at any time. The customer uses his/her Ethereum ERC20 compliant wallet to hold operations. While the problem of classic binary options payments delays is seemingly solved with the automatic withdrawal, there is no adequate description of where the platform budget is stored and if it’s divided in several parts or not.

BlockOptions tells that ‘all funds will be held in cold storage’ without any further clarifications. If it is not just a marketing trick, the cold storage is actually one of the most secure ways to keep funds intact. The problem is that it seriously depends on the actions of the owner - and this cannot be called decentralization. In other words, cold storage might come in handy for individual traders, but keeping all the funds of the marketplace on a physical hard drive is too risky.

Spectre.ai offers customers to trade by connecting an independent crypto wallet, yet there is an option to open the ‘onsite trading account’. The use of external wallets may solve the funds problem partly. However, there are once again no mentions of how the platform budget is stored.

Giant.Exchange will have its own smart contract to store the marketplace budget coming from fees. The principle of the smart contract is distributing funds according to the voting results on each initiative announced through the Giant.Proposals system. The user funds are stored on their own wallets in the Giant blockchain and, at the time of the purchase of the binary option contract, these funds are placed on the wallet of the smart contract that makes this possible. After this choice is made, they are either transferred to the broker's account or returned to the trader with a profit.

This eponymous ‘Giant.Exchange’ contract will have an explicit prohibition to simply withdraw all funds to a cryptocurrency wallet.

Asset Price Data Source

Betex. It uses the average weighted price or a ‘composite rate’ made of the data provided by several unspecified digital currency exchanges. This aggregation resembles the work of Coinmarketcap, although on a much smaller scale. The average weighted price is calculated by, as it seems, a single Oracle - an automatic component stored separately from all other parts of the system.

BlockOptions claims it used CryptoCompare in its MVP stage and will use Xignite in the full version. This is a relatively known cloud platform independent from BlockOptions, it provides the market information to fintech companies on a regular basis.

Spectre. It gets the prices info from two sources, including Xignite which we just saw mentioned in the BlockOptions materials. We can see its wide popularity. Another source is unspecified. The data coming from these two sources is ‘monitored and audited’, Spectre vows.

Giant.Exchange. The data can be provided by individual Oracles who use eponymous smart contracts to link the exchange/price aggregator API with the binary options marketplace. The reputation system will make it possible to swiftly detect rogue Oracles. The traders will always see where the data is coming from and can check the source reputation by searching the related information on the Web. The amount of data sources can potentially become much bigger than on Spectre, BlockOptions and Betex.

Brokers

Betex and Spectre.ai claim that traders will only bet against other traders. The latter platform also offers an opportunity to bet against the decentralized crowdsourced ‘liquidity pool’. Due to the extremely bad reputation of classic binary options brokers, some of the reviewed platforms have decided to abandon this concept completely.

BlockOptions. It’s interesting how the authors of the White Paper go through a lot of effort to persuade the reader about the nefarious nature of regular brokers, instead offering Bankrollers - they ‘send ETH or BOP to create an asset contract or back existing contracts and make profit from bankrolling’.

Giant.Exchange. As in the previous case, there is also a category of people who create new binary options contracts independently from the platform owners or creators, but they are simply called Brokers.

Interesting to see how very different platforms are united in the idea that traditional binary options brokers must either be redefined or excluded from trading completely. The user-generated content (USG) principle is executed in different forms on all of the reviewed platforms.

ETH Price Dependence

Betex and BlockOptions. The big disadvantage of all Ethereum-based decentralized applications is the volatile price of Ethereum which may affect the reputation and the user interest towards them. In this regard, Betex looks most dependent, as its fees are made in gas. The situation with BlockOptions is quite similar: Ethereum is used to charge for trades opening which can prove demanding in case this cryptocurrency becomes higher than it is right now.

Spectre.ai actively uses its tokens to replace Ethereum, yet the indirect influence of Ethereum news and price motion can still harm the project. The dividends to SXDT token holders are paid in Ethereum which recently lost in value.

Giant.Exchange and other decentralized apps (DApps) will not depend on Ethereum because they were never linked with this cryptocurrency blockchain environment to begin with. The common downside of all three platforms is ERC20 - the token standard which has been described as insecure by the press. Giant.Exchange will not be connected to the Ethereum blockchain and will use its own payment and fee tool - Giant Coin that has the best features of Dash and Ethereum combined. The wide use of Giant Coin (GIC) will compensate a high emission level There was, however, a problem connected with the well-being of Giant.Exchange DApps - mining whales started to simply mine and sell Giant Coin which was very harmful to the price stability. This undermined the viability of GIC as a main Giant DApps payment tool. The move to the Proof-of-Stake consensus algorithm has dramatically improved the situation.

Security Issues

Trading is always risky. Even the classic stock trading is regulated for decades and it has serious financial scandals, big losses, crises and fraud schemes. In the young crypto sphere, the risks multiply even higher. However, some platforms may be less riskier than others, and this can be said about Spectre.ai in comparison to Betex and BlockOptions.

Betex. If anything, it warns the potential customers of possible Ethereum blockchain vulnerabilities which can serve as an adverse effect on the work of the binary options platform. In this case, Betex categorically states in caps lock that it would not be held liable for any loss of tokens happened due to the attack on the user Ethereum wallet.

BlockOptions has another indirect hint of the poorer management state in comparison to Betex and Spectre: it’s the grammatical errors in the White Paper. Betex and BlockOptions remain largely unnoticed by the common crypto and binary options traders.

Spectre. As you can clearly witness from the site materials, it does not repeat the awkward mathematical mistakes of its rivals, has a better representation online and its tokens transfer volume is higher. The approach of three platforms towards financial laws is another reason why binary options may be more secure on Spectre. Despite this, the standard problems of Ethereum originating from its blockchain can directly influence the platform future. Such problems include: numerous sharding technology implementation delays, decentralization deficiency and other problems previously described in the article dedicated to the elements of Ethereum in the Giant blockchain.

Giant.Exchange. By far, the biggest security problem was a 51% attack attempt detected during the first steps of the project. The high GIC emission level has led to a quick rise of masternode and the subsequent decentralization acceleration which renders such attacks impossible.

Legal Framework

Betex, as already mentioned before, strongly recommends everyone not to view their tokens as securities although the investment process fully corresponds to the main points of the Howey test. They have also mentioned the registration of their token in the SEC in Q3 2018 at the site roadmap - this easily might be just a marketing claim.

BlockOptions. In this enterprise White Paper, a similar disclaimer can be found at the very end. Both platforms have only rejected the security nature of their tokens.

Spectre.ai took stricter measures: its founders have blocked its website for American clients and implied that the bypass of this block will be a direct violation of the website terms of use. The U.S. regulators will not have complaints about the citizens participating in the unregistered securities trade.

Giant.Exchange. This ‘token as a security’ principle is irrelevant when it comes to Giant.Exchange: Giant Coin is a cryptocurrency used as a method of payments and fees. Contrary to the Howey test conditions, nobody will invest in Giant coin in hopes to gain profits off of others’ work. Those who would like to receive a passive income may consider establishing a network masternode.

This recent statement of William Hinman, director of the United States Securities and Exchange Commission division of corporation finance, can be fully applied to Giant Coin:

“Putting aside the fundraising that accompanied the creation of Ether, based on my understanding of the present state of Ether, the Ethereum network and its decentralized structure, current offers and sales of Ether are not securities transactions.”

Another critical factor that separates Giant Coin from tokens: it doesn’t have a single emission center — thus it doesn’t fall under the definition of a token. Apart from this, Giant.Exchange does not require the KYC measures implementation, as its KYC-level security is backed by its blockchain. You can read more about this advantage in a separate material.

As you are about to see below, the lack of political and economic expertise has proved to be the ultimate undoing of BlockOptions ICO. The Chinese-based project clearly didn’t expect the prohibition although the press indicated it might happen several weeks before it was imposed.

Funds Raised

Betex has sold ~$10,233,480 of tokens during its ICO, according to ICOBench. It was held from 1st Mar 2018 to 15th Apr 2018. This ICO can be called successful considering all the inconsistencies we have previously seen.

BlockOptions. ICO started 25th August 2017 and ended 25th September 2017, 18,000,000 BOP (sometimes dubbed BOPT) tokens were to be sold. According to BitcoinTalk, the Chinese ICO ban has abruptly ended the whole enterprise. As a result, we cannot find the exact numbers of the funds raised by the developers, but we can state with certainty that BlockOptions ICO had failed. The amount of current token transactions leads to believe that the project will not raise the adequate amount of funds in any foreseeable future.

Spectre.ai. ICO was held at the days of the peak values of Bitcoin which, as you might already know, serves as a locomotive for many other cryptocurrencies. Can we expect a big number of funds raised from 17 Nov 2017 to 10 Dec 2017, then? No, says ICOBench. The total amount is shown as ~$16,600,000 which is only 6 million more than the ICO of Betex.

Giant will remain popular and the blockchain environment will be maintained by masternode owners’ decision taken after votes. The masternode owners are the main project investors, in a way, the decentralized digital board of directors. They are interested to keep the system in a healthy shape, initiate community proposals and vote on the changes and improvements financing. The system receives a potential to outlive its original creators. No payment tool on any other reviewed binary options platform has this opportunity. You can learn more about the masternode governance aspects and Giant blockchain maintenance in a dedicated article.

It is yet to be seen how the crypto community will receive Giant.Exchange, but it is already clear that we don’t need millions of dollars raised even before the project is ready.

Comparative Table

Let’s sum up what we have just researched. We can clearly see an outsider - BlockOptions. This was the only project which has failed to raise funds as it planned to do initially. The style of its White Paper leads to believe that the team did not manage itself very well, as it contains numerous mistakes. This management could eventually result in security breaches.

Interestingly enough, the overwhelming majority of reviewed projects were launched in autumn 2017. Those who follow the cryptocurrency news can remember the sudden boom of Bitcoin during that time. In Q4 2017, Bitcoin, blockchain and digital currencies have become the number one topic in the media which made the whole market more attractive. The initial coin offering (ICO) boom has also happened in the same quarter.

We may even suspect that the main intention of BlockOptions was to raise the money off of the ICO which explains the haste with which they have composed their materials and formulated their ideas. Betex suffers from the same problem.On the other hand, Spectre.ai has proven to be an adequate rival to Giant.Exchange with an obvious disadvantage: the data sources have been chosen by the platform founders and cannot be changed by the customers via any voting - and this is exactly what we are offering. Even though the project is better than some others, it still suffers from the chronic dependency on the Ethereum environment.

Note that both Betex and Blockoptions do not use their tokens as both payment and fees tool, while Spectre.ai has a separate utility token. In the non-digital world, money can be used both in fees and payments, this is why one can say that Giant Coin is closer to being money than all other tokens from the table.

The most notable con of Giant.Exchange is that it’s still not released, but soon you will see the first working prototype. All basic components will be present there — including user-generated price data smart contracts, the main advantage of Giant.Exchange over all other reviewed platforms.