Quality Of Life

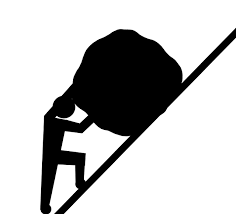

Look closely at this picture. Does it make you feel sometimes that this is actually you struggling with some heavy burden? Or a serious problem? Or an almost impossible task? Does it make you ask, "What's going to happen if the man slips or fall?" Does it also make you ask, "Can I help?"

Here's a hypothetical scenario I would like you to imagine about this picture:

- The person pushing the rock is you;

- The rock being pushed is your family;

- The top of the hill is financial freedom; and,

- The bottom of the hill is financial ruin.

Does death have to mean the end of the family's hopes and dreams? Is there a way that this can be avoided?

Fast forward. Imagine this scene at the wake. Wife and kids are mourning the passing of the father. Adding to this grief and misery is the worry and uncertainty of how they will carry on with their lives now that their only source of income is gone. The wife, amid her sorrow and pain, is thinking of their future.

On the third night of the wake a stranger walks in the room asking for her. When they meet he extends his condolences and heartfelt sympathies. He tells her he knew her husband and that they have talked in the past of exactly this day happening.

The anguish and pain are still too heavy to bear but now the wife doesn't have to carry the extra burden of uncertainty over her family's future. Life must go on. But the quality of life you leave to your family can be predetermined and not left to chance. Do you agree?

Have you prepared for the biggest crisis your family might face? It isn't too late yet if you haven't, provided you are in reasonably good health. Go talk to a life insurance counsellor now.

All photos sourced from Pixabay.

Insurance is a necessity to provide for your family. While you spoke about the major breadwinner having a policy, I believe both parents should have policies. If the one parent stays at home or works part-time to care for the family, the death of that spouse also has an impact on the family.

The surviving spouse may now have to pay someone to care for the children, clean the house, or tend to the other tasks once done by the deceased spouse.

I agree with you a hundred percent. If the funds can support a second insurance coverage it must be for the spouse of the major breadwinner. There are definitely financial considerations involved with the demise of the spouse whose responsibility is as the homemaker. Unfortunately, in our country, it is often the case that available funds for insurance programs within the average household is hardly enough even for the breadwinner resulting to underinsurance or worse, lapsation due to non-payment of premiums.

Thanks for dropping by.

I am a bit at peace if such incident will happen to me because although maybe theres a little adjustment but I am sure my wife can carry on with the financial obligations since she also have a good paying job (thanks God) and we became independent from both sides (parents) since we got married. But I still consider getting a life insurance as a must although I already have medical and memorial life plans.

Can you suggest one good life insurance company?

By the way this is another great article do try to submit it through esteem app next time for possible bigger upvotes. You can give me your link so I can pass it on to @iyanpol12.

The link to this post is https://steemit.com/family/@gems.and.cookies/quality-of-life.

Thanks sa heads up.

I mean the link of your next blog where you will use esteem app or esteem surfer in uploading or submitting your article. If you havent had info regarding the app you can check @g10a's article about this app.

https://steemit.com/esteem/@g10a/these-are-the-reasons-why-i-love-using-esteem-app-595477dba16e5

Ah ok copy bro. Will check on @g10a's link to esteem app. Am using steemph as one of my tags but there seems to be no support from them. I will change it next time. Thanks.

Basically in the Philippines most insurance companies sell only variable life insurance now. Wala na yung traditional plans. A variable life insurance is a unit link insurance and investment plan. It's a 2 in 1 plan where there is coverage if you die too soon and retirement benefits if you live too long. The value of the plan is linked to the units of investment where your excess premiums are allocated to depending on your risk profile. Pwede sa stock market if you can tolerate risk. Pwede naman sa bonds lang if you are not a risk taker.

Dahil pare-pareho lang ang plans na ino-offer ng mga insurance companies, with basically the same benefit structures, the main consideration will then be the price of the plan. The cheapest so far that I know is that of Insular Life which can offer a 1 Million coverage for as low as P1,666.66 a month. That's about USD 31.45 a month. Of course this will also depend on the age. Kung over 40 na baka magtaas ang premium ng konti but not so much. This means for just less than a USD 100 a month (USD 94.35 to be exact) you can be already insured for 3 Million. That's how low Insular Life is compared to others. You can check it out on your next vacation here.

Thanks for reading this post as I requested.

I will start to scout for other good unsurance company now in addition to Insular Life for comparison, my main concern now is the monthly premiums I should get the lowest possible as I will be earning local rates soon...

Thank you very much for the info.

Really? Back to Pins ka na soon? That's good news! You must be excited. Anyway, that's usually the main concern when taking an insurance program - How much is the premium. Yes, be sure to check from the different companies so you will have a basis for comparison.