Will the Australian Dream Lead To a Debt Crisis?

I recently asked renowned economist Steve Keen to write an article for PropertyInvesting.com. He was kind enough to do so, and I just posted his article this week. It’s a fairly technical explanation of Australia’s debt situation, but I offer my own summary as a comment, if you care to check it out.

Keen has caught a lot of flack here in Australia. He’s been warning of a debt crisis for years, and the real estate perma-bulls here hate him with a passion. After posting his article, I got the following email from one investor expressing his disgust and intention to unsubscribe from our newsletter:

Steve Keen has been wrong too many times in the past. Cya.

I replied to remind him that there’s a difference between being “wrong” and being early.

In April this year, Keen wrote an article for Forbes, which I summarized in my own article for the PropertyInvesting.com community. I’m sharing those same thoughts in this post for you, my Steemian friends.

In the Forbes article, Keen ranks Australia as number two on the list of seven nations that are most likely to face a debt crisis and recession in the next three years. The only country more likely is China, which also doesn't bode well for Australia’s economic future.

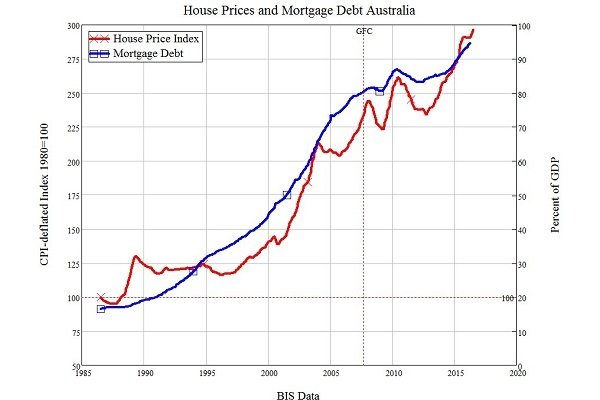

Australia has the highest household debt to income level in the world, and the second highest in history. Our primary motivation for borrowing has been to fulfill the Aussie home ownership dream. As house prices have surged, so has the need to borrow big.

While credit card and personal loan debt has remained relatively stable, mortgage debt has skyrocketed. According to recent data from APRA, Australian owner-occupier home loan liability is now at an all-time high - more than doubling in the last 11 years. In December 2004, the outstanding mortgage debt per Australian adult was $20,802. By December 2015, that figure had ballooned to $49,165. It’s continued to increase since then, as the housing boom has persisted on the back of low interest rates.

Steve Keen has been strongly influenced by the writings of Hyman Minsky, who I’ve written about in this post. They both believe the primary cause of a financial crisis is the accumulation of private debt.

The following is a three-point summary of how Keen sees the next few years playing out.

1. We can’t borrow like this forever.

The foundation of Keen’s prediction is his assumption that our current borrowing trajectory is unsustainable. This should be obvious, but most Keynesian economists reject that assumption.

So what kind of debt growth is sustainable? Keen believes that only a growth rate at or below the growth rate of the overall economy - measured in terms of GDP - is sustainable. A growth rate above that of the overall economy is not sustainable.

Our economy is currently growing at about 3 percent, so Keen sees anything above that as unsustainable. Currently, Australia’s debt is growing at over twice the rate of its economy, and has been nearly doing so for some time.

So what makes debt unsustainable? Think about your household finances. If your personal debt is growing faster than your income, then eventually you’ll be unable to service your loans.

This is exactly what Keen expects to happen on a broader level. We’ll soon reach the point where there’s not enough margin left in our collective budgets to afford loan payments. People will stop borrowing, and credit growth will decline, and likely even go negative.

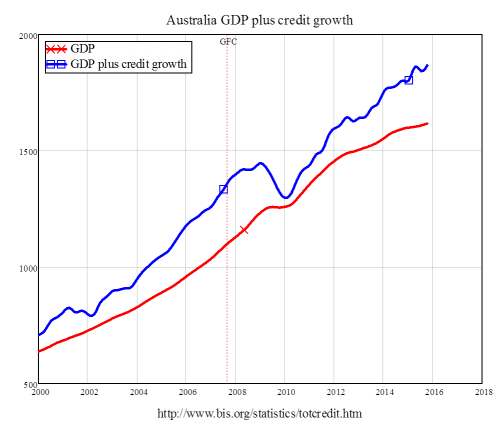

Here’s a graph showing the growth in our economy in relation to the growth of private debt:

Keen expects to soon see the blue line fall near or below the red line. We nearly got there in 2010, but government stimulus and monetary easing bailed us out.

2. When we’re no longer willing or able to borrow, the economy will shrink.

The growth of any debt-based economy will always be dependent upon credit growth. We need people to borrow and spend in order to keep the economy growing at the current pace.

This is exactly why the RBA and virtually every other world central bank has been lowering interest rates. The aim has been to spur people to keep borrowing more and more in the hope of stimulating economic growth.

Central banks need credit growing faster than the overall economy in order to reach stated goals for inflation, GDP and employment. The problem, according to Keen, is that perpetual credit growth is impossible.

If Keen is right, and credit growth soon falls or even worse, goes negative, then there will be less demand for goods and services in the economy because people will have less money available to spend. After all, thanks to our fractional-reserve banking system, it’s the banks that create new money through lending, but when banks take in more money through repayments than they lend out, the money supply shrinks.

A shrinking money supply means that demand is draining out of the economy. Wages and home prices must therefore decline. When demand falls, the economy is contracting, and this is what economists call a recession.

3. When the economy shrinks, asset prices will fall.

The unintended side effect of an economic system that encourages debt through low interest rates is higher asset prices. When you make money cheap and easy to borrow, you encourage people to keep buying and investing, sometimes unwisely, in assets like shares and real estate.

As those assets become more expensive, people will need to borrow more money to pay for them. Eventually, when the borrowing must stop, so does the buying. Demand falls, and then the value of the underlying assets falls, too.

This can be especially painful for those who buy during times of euphoria, when no one believes that asset prices will ever fall. As legendary investor John Templeton said, “Bull markets are born on pessimism, grow on skepticism, peak on optimism and die on euphoria.”

Typically, it’s the last ones who buy just before asset prices fall who are the ones who borrow the most, which means they are also the ones who have the most to lose.

The writing is on the wall...

According to Keen, and Mensky, you’ll know the party’s almost over when people who buy assets can only do so on interest-only loans. They’ve borrowed so much money that they can’t afford to pay down their debt. They justify their repayments on the assumption that asset prices will always increase, or that incomes will be higher in the future. They’re speculating on either asset or wage inflation, or both.

According to ASIC, one in four owner-occupier loans are interest-only. In a recent industry crackdown, the corporate regulator found that demand for interest-only loans has grown by 80 percent in the past three years alone. It seems like the number of people who can afford to pay down their principal is shrinking fast.

Most interest-only loans offer a period, typically up to five years, before they require additional principal repayments. What happens if these loans roll over and borrowers can’t afford the higher monthly payments? The banks don’t seem to care.

ASIC found the following astonishing results after a lending industry review:

• In more than 30 percent of cases, there was no evidence the lender considered whether the applicant could afford their repayments over the long term.

• In 20 percent of cases, the lenders did not consider the actual living expenses of the applicants.

• In 40 percent of cases, the lenders had incorrectly calculated the affordability of the loan.

While Steve Keen believes the end of days for credit growth is soon approaching, he admits the timing of the inevitable is impossible to predict. No one knows exactly when people will stop borrowing or banks will stop lending.

We may even see our government kick the can further down the road, just as they did in 2008, through more hard-core stimulus measures. If recent patterns of central bank intervention are any indication, property may even have a few more years of growth to go. Or, it could all come crashing down within months.

@jasonstaggers

Please follow me if you enjoyed this post. Thanks!

{kind=link}

Yes it's not a question of if but only the when to prepare for. Everything seems to be in bubble territory.

Great piece Jason and thanks for sharing. Happy to upvote and share this on Twitter✔ for my followers to read. Stephen

Thanks Stephen. Always appreciate your feedback.

Are you still around? I think about you sometimes and miss you too!

I pray that all is well with you and yours.

Thank you my friend. I was lost, but know I am found :) Congrats on the newest little pepper. You must be catching up to me now.