Housing Affordability Survey Shows Australian Families are Struggling and Feel Entitled to Government Help

The Australian National University (ANU) recently released findings from a poll on housing affordability that reveals some troubling facts.

The poll was quite extensive, so I've pulled out the responses that I believe are most relevant to both property investors and anyone concerned about the future of the Australian economy. These results may also shed some light on the policy decisions we can expect from the RBA and APRA in the not-too-distant future.

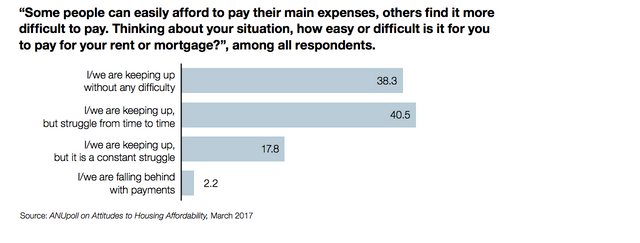

Many people are already having a hard time keeping up with their housing costs based on their current income.

Nearly 1 in 4 mortgage holders would experience “quite a bit” or “a lot” of financial hardship if interest rates went up by as little as two percentage points. Half of the respondents would face at least “some” hardship.

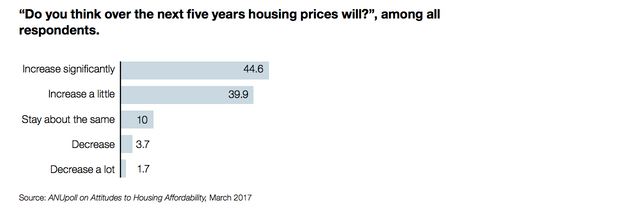

Most Australians believe that home prices will keep going up. Hardly anyone expects a correction or downturn in the market.

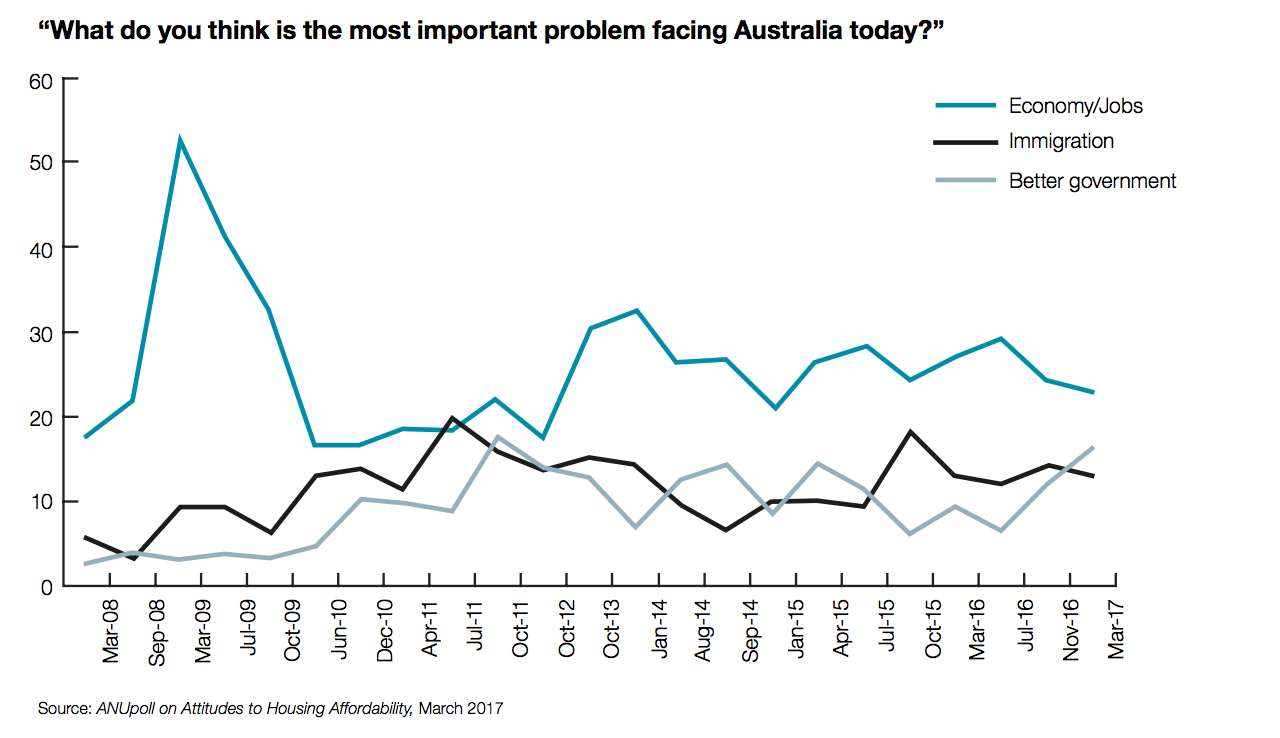

An increasing number of people are blaming the Government for Australia's problems.

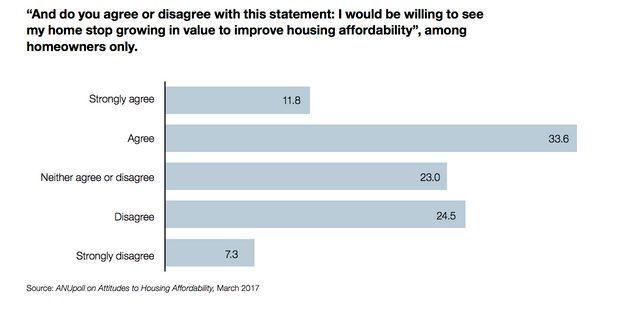

Nearly half of homeowners would be happy to see the Government or regulators step in to stop home prices from going higher.

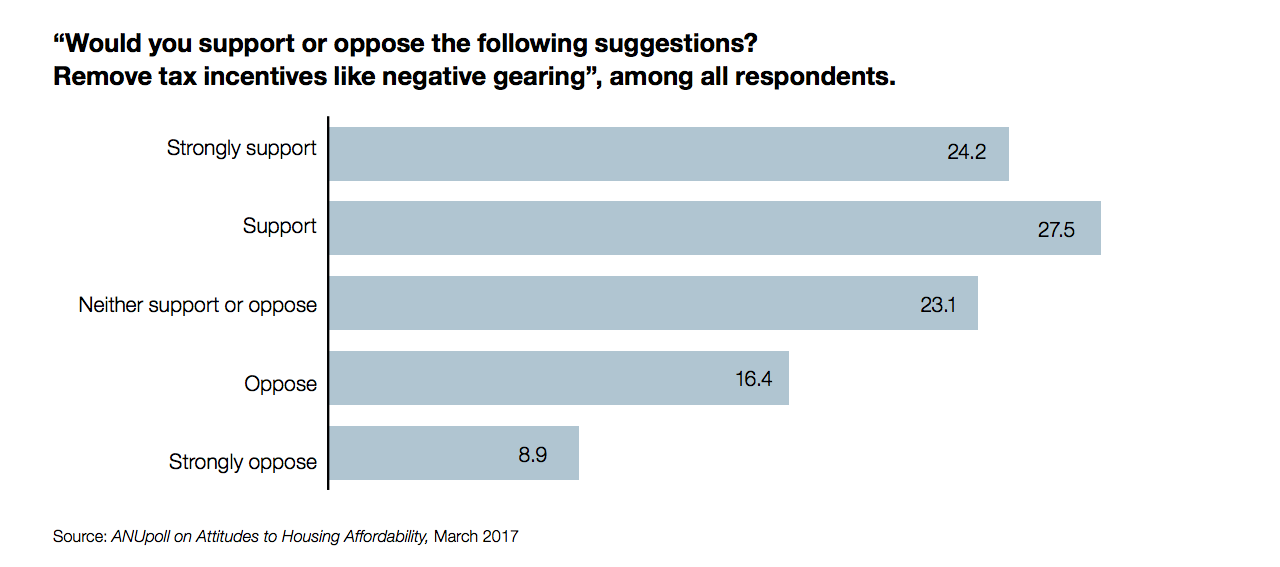

The majority of Australians would be happy for the Government to scrap the negative gearing tax benefit for property investors, and only 1 in 4 would fight to keep it.

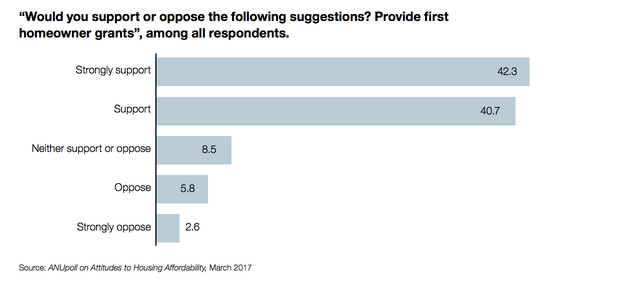

An overwhelming majority believe that the answer to Australia's economic problems is found in the Government throwing more money at first homebuyers who are struggling to get into the market.

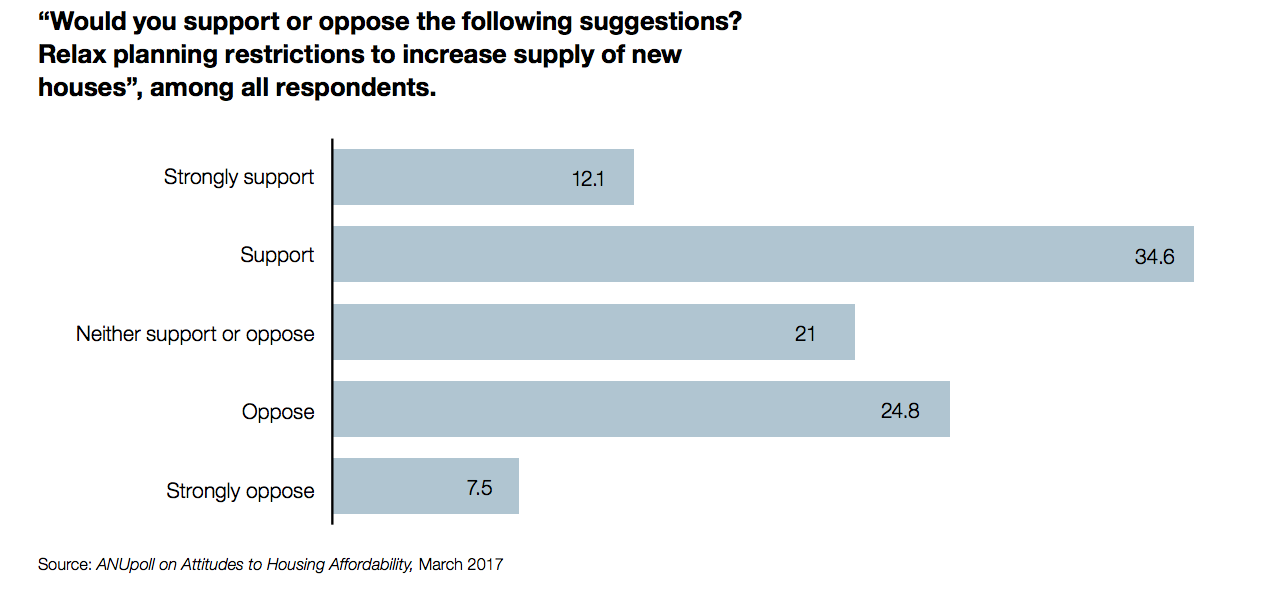

Most Australians either don’t see how local government planning restrictions are contributing to higher housing costs or they highly value the livability benefits of not increasing density of housing nearest to jobs.

Here are some of my summary thoughts on the significance of these responses:

The RBA has been aggressively suppressing interest rates for the last five years. This has encouraged homeowners to borrow more than they can afford and motivated investors to speculate on ever-increasing home prices. This has, in turn, inflated home prices to the point where any moves upward in borrowing costs would bring tremendous financial hardship on the majority of families. This makes future interest rate increases by the RBA highly unlikely, at least until wages rise considerably and consumer price inflation catches up with home price growth.

Because so many people think that the Australian property market is resilient and home prices will only continue to rise, people will continue buying, at least until policy makers step in to cut off demand, or other economic woes shift sentiment. Although APRA has recently made minimal attempts to raise borrowing costs for investors and diminish demand, prices have continued to rise. This means investors can expect interest rates to rise further. Owner-occupier interest rates will likely remain low.

Most Australians see the Government as the answer to all their problems. This means people will most likely remain supportive of measures by both politicians and APRA to slow down investor demand. Politicians know this, so expect them to try to woo voters with promises to take action on improving housing affordability.

The left-wing Labor party has been the most vocal about curbing investor demand. They have proposed significant changes to tax concessions for property investors, namely excluding existing home purchases from the negative gearing tax benefit and reducing the capital gains tax discount from 50% to 25%. We shouldn't be surprised to see Labor back in power, handing out more money to the have-nots, and bringing big disruptions to the housing market.

Because Australians love to be given free money from the Government, at the expense of the most productive people in the nation, nearly everyone supports measures to help first homebuyers be able to afford very expensive properties. What many fail to recognise is that every time the Government dishes out grants, more money flows into the market, which increases demand and causes prices to rise further.

The answer to all of Australia's housing affordability problems is to get both politicians and regulators out of the way and leave home prices to the forces of supply and demand in the free market. This would ideally mean abolishing the RBA and dramatically reducing the size of the Australian government. This is highly unlikely given the entitlement mindset and shirking of personal responsibility that's rampant in Australian culture.

What are your thoughts on the survey? Where do you see this heading? What do you think the answers are to solving the housing affordability problems in Australia?

Jason Staggers

Solid article.

The game of musical chairs that is the Australian property market will not go on forever. The music is going to stop and when it does many people are going to lose their homes and jobs. The depth of this correction will depend on how low they are willing to turn down the music volume.

Another issue is 'quantitive easing' - the pumping of funny money into the economy which keeps the music playing. America has been doing this since the GFC. It gives people a false perspective of the economy and their futures. All that it is doing is increasing debt levels and kicking the can further down the road for someone else to deal with. You don't reduce debt by borrowing more money but that is what is happening.

I'm expecting a huge global crash and correction at some stage but I don't know when because I don't know when they are going to tighten the screws by either:

A: raising interest rates

B: slow down the printing presses

C: combination of A & B

Plenty of truth there @steemtruth. I tend to think Australia's economic woes will come whenever the crisis you speak of begins elsewhere in the world. We're very dependent on debt markets in the US and Europe remaining stable.

A fourth possibility is they double down, or I should say quadruple down, on QE and print the dollar and euro into oblivion leading to mass or hyper inflation. But as you say, it's all in the government / regulators' hands. They'll do what they wish and hopefully we'll learn our lesson for entrusting it all to them.

I agree with you @jasonstaggers and all that you wrote in your article. A meltdown will start somewhere else and Australia will be hit as a by-product of events elsewhere. Many banks have excessive levels of toxic debt on the their balance sheets.

You probably know that Satander bought Spain's 6th largest bank (Banco Popular) for 1 euro. I read somewhere that it came with 32 billion of debt. Satander is asking it's shareholders to chip in almost 8 billion. If they don't they will be diluted in the capital raising.

Good point, hadn't thought of that but it is certainly possible.

Can you see an Australian government in the near future making significant changes to negative gearing, capital gains or the first home buyer schemes? I read what you said about the noise that Labour is making but I don't keep up with politics very much these days. There is a lot of sabre rattling and I try to avoid it for the most part.

You're right, there are so many insolvent European banks. Any disruptions in the bond market will likely bring them down. Who knows what that will mean for the derivitives plays. It could get really ugly.

Regarding changes to tax concessions and first home buyers grants, I think it depends on where the housing market goes. If prices remain elevated, then I expect public backlash from the have-nots to elect Labor who's already promised changes to negative gearing and the CGT discount. Regardless of who's in power, I expect the first home buyer grants to increase.

I'm with you; politicians are a joke. I tune them out for the most part as well.

True Flip {ICO} - Already running a transparent blockchain lottery! Bomb! Bonus 20%! Hurry! :)

The platform is already working and making a profit :)

https://steemit.com/ico/@happycoin/true-flip-ico-already-running-a-transparent-blockchain-lottery-bomb-bonus-20-hurry

Hey there Jason, awesome post it's good to see what other Aussies are thinking when it comes to the upcoming property disaster - I just don't see any way of avoiding it.

I live in a modest neighbourhood in a new housing estate and I have seen a massive increase in established houses being sold off, some streets have had seven houses for sale at once - this was not the case two years ago.

I think people are being more affected where I live, because of the rising prices and the fact most of them probably couldn't afford the houses to begin with.

I too dream of one day having a house (renting just feels like wasted money), but with prices as they are and the threat of impending doom when the property market does finally crash see us still renting.

We spend way too much money on rent, it is by far our biggest expense and it increases every year and we get no benefits.

With our kids needs owning a house would mean, being able to properly secure it for their safety and building/redesigning it around their needs - it would be a life changer for them, so it is a high priority for us but is just doesn't seem like a practical goal.

I was wondering if you knew what the deal was with rent to own homes? Are they just the scam they appear to be? Or is this a valid option generally (but probably not before property prices are going to plummet)?

Hi Krystle. Great question.

I wouldn't stress too much about renting for the next few years. We are also renting now, and are doing so by choice. The area we want to live in (for schools, convenience, lifestyle, etc.) is VERY overpriced and I believe there will be a better time to buy.

The homes in our area that would suit our family are selling today for well over $1m. Based on current wages and if interest rates were not artificially suppressed, these homes should be valued at between $600k and $700k. I expect the RBA to lose control of long-term interest rates sometime in the next year or two. That will put downward pressure on home prices.

Even if I'm wrong and prices do not fall, then wages will have to rise. The wide gap between home prices and incomes is not sustainable. If wages rise, that means inflation, and Aussie dollars will be easier to come by, and homes will not be as expensive relative to the value of fiat.

Queensland is a little different. Home prices there are lower relative to incomes, but if interest rates rise, you can bet home prices will fall there too, although perhaps not as much as Sydney/Melbourne to align with wages.

A helpful question to ask is, "what is the opportunity cost of buying a home?" For instance, if you had $750k cash and could afford to buy your dream home outright, what else could you do with that money if you instead chose to keep renting? You could buy a commercial property paying an 8% yield, which would pay you $60,000 per year passive income. It would likely cost you $30k per year to rent the same home, which means you are $30k per year worse off owning rather than renting. You need a lot of capital growth (above inflation) to justify that loss. Either that or just need to care more about the convenience of owning than the loss of that money.

When I explain that concept to my clients in Melbourne and Sydney, some of them decide to sell their homes because for them it's more like $80k per year they are losing by owning. That's enough for the wife to quit her job and look after the kids. Most people would rather rent than remain a slave to their jobs.

Some day, home values will be more in line with rent costs, which are a truer reflection of what the cost of housing should be relative to incomes. When that happens, you'll know it's a good time to buy.

Hopefully, that helps you feel like you're not wasting as much money on rent as you think :)

Regarding rent to own homes, it's a great idea when money is hard to borrow from the bank or you can't get a loan because of bad credit, but only when you expect home prices to rise. Essentially, you're buying the right to buy the home at a certain price in 5 years time. If the home goes down in value, you'll decide not to settle and will lose your deposit, which is often about 3 to 5% of the purchase price. You would also have been paying higher rent as well, a portion going to principal, which you would lose. In my opinion, the early 2000s was a good time to rent to own, but not so much today.

Great information. I think we are going to need to bite the bullet and stop propping up the housing market.

The government needs to look past the next 4 year term and at the bigger picture. Its great to see the price of my home rise, but now most housing markets are out of the reach of the average australian.

Time to get some foresight and good economic monetary policy happening in Australia or else we will find ourselves in the same situation as the US did in 2008/09 (if we are not there already).

The next few years will be interesting to see where the housing market goes.

Great comment. It will definitely be interesting.

That would be refreshing. Unfortunately, I have zero faith in either our politicians or the RBA to do what's best instead of what's expedient. Hopefully, when their policies fail, we'll move closer to liberty, personal responsibility, and a freer market.

Great post Jason - Aussie property market is in for a rude awakening one feels. Upvoted and resteemed - see you back at SirKnight's party.

Sorry for the delayed reply. @sirknight is trying to drink me under the table.

Thanks :)

Im here in Auckland, New Zealand.

South Auckland Suburbs such as Otara and Mangere have housing prices way above the average income. Otara and Mangere are the Low socio-economic areas and you are looking at 800+ for a 80+ year old 3 bedroom 1 bathroom home.

I feel for you Aus if things get as bad as they are here.

Yeah, that's pretty bad. Sydney is not far behind you. The government in NZ has been a little more aggressive making it harder for investors to borrow. We'll see if the same plays out here as well.

A very useful survey

Good post

Great post Jason, I can only see this ending in some type of disaster, sadly but we only have ourselves to blame. As for abolishing the RBA, the RBA and the government work for the same masters and it's not us the taxpayers. We will never relieve ourselves of this parasitic criminal organization. Cheers

I wonder if, at least for a generation or two, we'll wake up to how unnecessary they all are and overthrow them. I'm confident that sooner or later, liberty will win.

Hi Jason

Interesting post. I deal with a wide variety of industry in Australia and no matter who you talk to everyone is doing it tuff at the moment both on a personal level and business level including very large companies. Unfortunately the the Australian Government rely on the building industry to create jobs when other sectors of business are slow, dying or simply dead. This was clearly seen when we were in the mining boom that we all knew would go bust. Because of the vicious circle we live in when the mining boom took off housing prices also followed along for the ride. In small country towns like Chinchilla in QLd before the mining boom they had a deal where if you bought business into town you could buy a decent block of land for $1.00 believe it not that is a fact! When the CSG Fracking gained traction housing prices went skyrocketing up to 600K and now that the CSG programme has almost come to a halt there are now many houses for sale under 200K because there is no-one there to rent or buy them.

This pattern can be seen all over Australia where housing prices have risen with our mining booms but sadly the prices in major cities stay up and really do not go down, its a vicious circle that will continue to go around and around. You hear statements of housing prices going lower but unless you are desperate to sell then the housing prices will not fall. It simple really, say you bought a house for 600K there is no way your going to sell that house for 550K or 500K why would a person take that loss unless like I say that you are desperate to get out? Not only do house prices go up but so does the cost of living in Australia goes up along side it. Our Energy cost are going up and even though South Australia are now spending millions with Elon Musk building the largest storable energy battery to apparently save on Power Bills, this is a load of garbage, I can bet their power bills will only go up to pay for the scheme.

To summarise, I don't know what the answer is to get our housing market affordable again but getting handouts from the government is not the answer, its a vote grab and quick fix. I think the answer might be by getting businesses to reinvest in Australia, bring back manufacturing, farming and general industry into the country to raise the standard of living including wages not to mention prosperity. The government should give incentives to businesses to encourage manufacturing and farming back into Australia and stop mowing down Orange Groves and buying imports, support locals and grow this country.

Good point. The areas in the future that will get hit the hardest are those that are majority owned by investors. Owner-occupiers will hold on as long as they can. Investors will exit when times get tough. A lot of investors will be stuck holding properties. This is exactly what happened in mining towns, as you referenced.

Good suggestions. I think those things can be accomplished by getting government out of the way. I don't think incentives would be necessary if we cut the costs to companies of doing business in this country (taxes and regulations).

I appreciate your thoughtful comment. Thanks for stopping by.

Thanks again Jason, excellent report. Have resteemed and upvoted.

Thank you, mate. Appreciate the resteem.

This post has received a 6.51 % upvote from @booster thanks to: @jasonstaggers.