Bitcoin Cash Soars to $700, Coinbase Customers Threaten to Sue

A new version of bitcoin hit the market on Tuesday and, on its second day of trading, it has already tripled in price and its market cap is now third biggest of all digital currencies.

Known as Bitcoin Cash, the new currency arrived via a so-called "fork" in which a faction of people who run the software that controls bitcoin started a breakaway version.

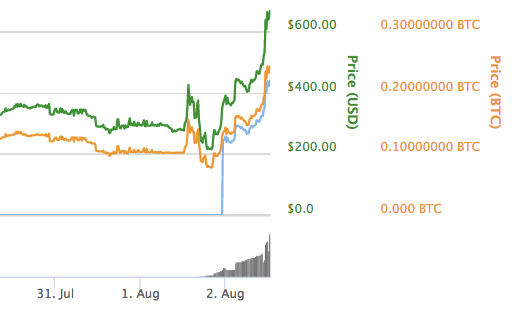

The price of Bitcoin Cash hovered between $200 and $300 for most of Tuesday and then suddenly shot up. As this screenshot from CoinMarketCap shows (look to the right of the graph), Bitcoin Cash has also appreciated in relation to bitcoin—one unit of the new currency is now worth about 30% of the original one:

Meanwhile, the price of the original bitcoin has, contrary to the fears of many bitcoin owners prior to the split, maintained its value. On Wednesday, bitcoin was trading around $2,700, which is not far from its all-time high of $3000.

As for Bitcoin Cash, it can be seen as a new asset class that achieved a valuation of $12 billion literally overnight.

It's unclear if Bitcoin Cash will be able maintain its value since, like other digital currencies, its real world use is limited and its value derives primarily from what investors assign to it.

And part of Bitcoin Cash's surge in value may be tied to a liquidity issue arising from a decision by some exchanges to refuse to distribute the new currency to their customers.

Lawsuits Brewing

The creation of the fork in bitcoin's blockchain—the software ledger that permanently records all transactions—by a minority of bitcoin operators followed a period of bitter infighting in the bitcoin community.

The details are esoteric (they center on the size and processing speed of the "blocks" on the blockchain), but the upshot is there are now two bitcoin blockchains, each with its own currency.

Upon the creation of the new chain, the breakaway faction chose to award Bitcoin Cash on a one-for-one ratio to every owner of bitcoin. So if a person owns five bitcoins, they are entitled to five units of Bitcoin Cash.

This scheme has been complicated, however, by the decision of the world's biggest bitcoin exchange, Coinbase, not to support Bitcoin Cash. For practical purposes, this means the millions of people who maintain a wallet on Coinbase did not receive the new "Cash" and, as of now, there is no way for them to do so.

Coinbase has clearly stated the company is not taking customers' Bitcoin Cash for themselves, but its decision to withhold the new currency has led one prominent legal scholar to suggest the company will be sued.

And, indeed, that now looks likely to transpire. An activist group, which claims Coinbase's decision is akin to a brokerage withholding new shares from its investors, warns it will commence a class action suit after August 15 if the company doesn't release the Bitcoin Cash.

Meanwhile, an attorney named Priyanka Ghosh-Murthy told Fortune he intends to file a complaint—invoking negligence, breach of fiduciary duty, and unjust enrichment—in Florida by the end of the week.Coinbase, which set out its decision on Bitcoin Cash in a July 27 blog post, did not immediately respond to a request for comment.

Originaly on http://fortune.com

While I agree it's unethical for Coinbase to not provide the BCC equivalent to it's user base post fork they did provide information prior to the fork stating,

"Customers who wish to access both bitcoin (BTC) and bitcoin cash (BCC) need to withdraw bitcoin stored on Coinbase before 11.59 pm PT July 31, 2017. If you do not wish to access bitcoin cash (BCC) then no action is required."

So am much as I want to also be angry, they did in my opinion provide ample notice to there users.

-IceBurst