BLOCK66: The Future of Mortgage on the Blockchain

Cryptocurrencies is one of the most important inventions since the inception of the web. They are ushering in a new era of decentralization, privacy, and control of one’s own data that has the potential to revolutionize many parts of society. There are currently over one thousand cryptocurrencies in use, with hundreds more being released each year. Their combined market cap has grown from $10 billion in 2016, to over $400 billion at the time of writing, having previously been much higher. Only 1% of the world’s population own cryptocurrency. Companies involved with blockchain, the technology behind cryptocurrencies and altcoins are expected to experience significant growth over the coming years. Blockchain technology can solve dozens of previously intractable problems, like digital identities, supply chain integrity, data breaches and many, many more. The use of blockchain technology within society has been exponentially increasing since it was introduced to the world by Satoshi Nakamoto. The first use of blockchain technology was bitcoin. According to Gartner Insights, blockchain, the driving force behind the crypto market is estimated to grow in business value to $3.1 trillion by 2030. Blockchain is the fastest growing market in the world and the Block66 token offers investors an opportunity to benefit from the growth in value. The age of blockchain technology is just beginning.

Before I proceed lets take a look at this video

INTRODUCTION

Block66 is building a new blockchain-enabled marketplace for mortgages. Institutional and private lenders can use the service to offer loans to a wide range of borrowers, introduced by Block66 broker partners. Through the practical use of smart contracts, loans can be taken from origination to facilitation, quickly and efficiently. All loans are also represented as tradable tokenized securities, providing a liquidity mechanism as standard. The ability to trade fractions of loans, and reduced order and issuing fees makes investing more inclusive, providing an attractive investment vehicle for all manner of investors.

Block66 eliminates the need for a bank account, overcomes geographical lending restrictions and reduces counterparty risk to mere minutes. For borrowers, the transparent and competitive nature of the marketplace will benefit the consumer and give them confidence that they’re getting near enough the best offer achievable.

MISSION

To shake up the mortgage lending landscape by building the world’s first blockchain enabled mortgage lending network. The network will span borders, connecting private and institutional lenders with borrowers worldwide. All mortgages will be issued and managed on the blockchain.

PROBLEM

The mortgage market in the USA is $9.9 trillion dollars, $32.9 trillion worldwide, and growing but risk averse institutions are reluctant to lend to many creditworthy consumers. Willing small lenders struggle to enter the space at scale. Existing processes and technology are cumbersome and siloed, compounding the problem for borrowers.

SOLUTION

Block66 streamlines the entire mortgage software and operations stack. For brokers, a one-stop-shop, including credit scoring, property appraisals and lender matching. For lenders of all sizes, a sustainable loan pipeline, auditing tool and mortgage securitization platform. For borrowers, a quick, hassle-free way to access the best credit opportunities.

FEATURES

Block 66 network tokens

These are the tokens that will circulate in the platform for the borrowers, creditors, private lenders, and institutional lenders will use and earn or pay in the platform.

Virtual checkers or underwriters and solicitors

They were tasked by the Block 66 team to have the delegation of checking the first-hand documents and verifications of the borrowers and for the approval of the lenders.

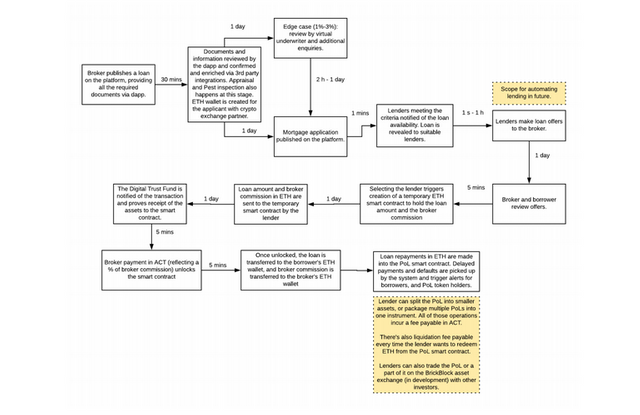

HOW DOES BLOCK WORKS

a. The broker and client perspective

i. Information gathering: The broker guides their client through the information gathering stage of the application. The dApp prompts the borrower for specifics around their borrowing needs and aspirations. Borrowers will be prompted to enter affordability data such as short and long-term credit balances, monthly expenses, regular income, and dependents.

ii. Identity checks: The platform uses third party APIs to carry out identity checks (KYC) to confirm the borrower identity, and to help brokers meet their regulatory requirements and detect fraud.

iii. Credit checks: Where possible, the system will perform cross-checks of affordability data by querying credit rating agency APIs and, in time, bank feeds to check income and monthly expenditure.

iv. Create crypto/fiat exchange account: Block66 will create accounts for all borrowers with a Block66-approved crypto exchange. This account will be used for loan repayments by the borrower after the mortgage is issued, and will act as a bridge between the conventional fiat banking system and the Ethereum/Block66 ecosystem.

v. Virtual underwriters: The system will refer an application to a virtual underwriter in the event it is unable to build a sound borrower file automatically. The broker, or their client, pay the virtual underwriter's fees in Ether (ETH).

vi. Application published: Once the system or virtual underwriter have signed off on a borrower file then the application will be made available to the matching engine.

vii. Matched: Matched when a borrower and lender(s) accept a pairing, and when sufficient lender capital has been matched to fulfill the applicant's borrowing needs, then the mortgage is ready to be funded.

viii. PoL contract funded: The lender(s) transfers the necessary ether (ETH) to the designated smart contract address.

ix. Repayments: The borrower sets up a standing order to a Block66 approved crypto exchange account, set up for the borrower during onboarding. When the system detects that funds have arrived, it automatically places a trade between the appropriate FIAT/ETH currency pair. Once the trade is filled, the system transfers the Ether (ETH) to the relevant PoL contract.

b. The Lender [Investor] perspective for new mortgages

i. Registration: Lenders [investors] register with the dApp at which point Block66's creates an account for the lender and makes a note of the Ethereum public key they wish to use.

ii. KYC: The platform carries out identity checks and enhanced due diligence on the lender and, if successful, flags the account as having passed KYC checks.

iii. Criteria: The platform prompts the lender to add their lending criteria before storing the result, before making it available to the matching engine.

iv. Approved: Once approved, a lender will begin receiving notifications whenever a match occurs. If the lender responds they will be invited to approve/reject a match.

v. Matched: Once a lender accepts a matching and the mortgage is fully funded, then a PoL contract will be created to reflect the loan agreement.

vi. Wait for remaining parties: Both parties must wait for their respective solicitors [lawyers] to confirm any additional conditions have been satisfied before the mortgage can progress.

vii. Contract funded: Lender transfers in ETH the correct dollar amount to the smart contract representing the mortgage.

viii. Loan repayment: As the borrower makes repayments, the PoL contract handles the distribution of funds to the respective lenders.

TOKEN SALE AND ICO DETAILS

B66 is a limited supply token that when stored in a special smart contract generates the network’s native token - BNET, that is then sold via the platform to network users (i.e mortgage brokers). The revenues generated by the sale are distributed to BNET holders.

TOKEN DETAILS

Symbol - B66

PreICO - Price 1 B66 = 0.10 USD

Price - 1 B66 = 0.15 USD

Platform - Ethereum

Accepting - ETH

Soft cap - 3,000,000 USD

Hard cap - 20,750,000 USD

Country - Singapore

Whitelist/KYC - KYC

Restricted areas - USA, Canada, China, Iran, North Korea

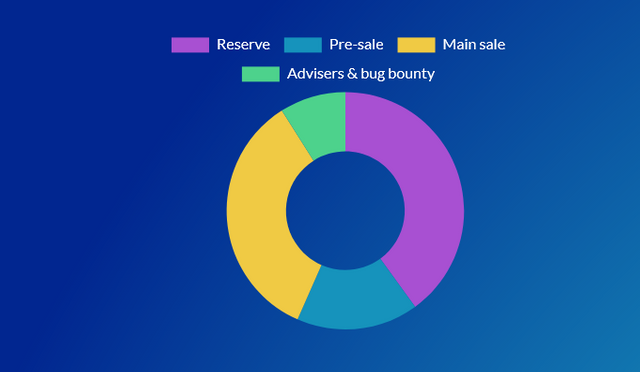

TOKEN DISTRIBUTION

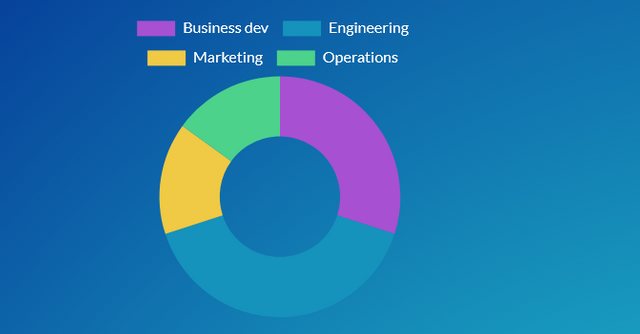

FUND ALLOCATION

ROADMAP

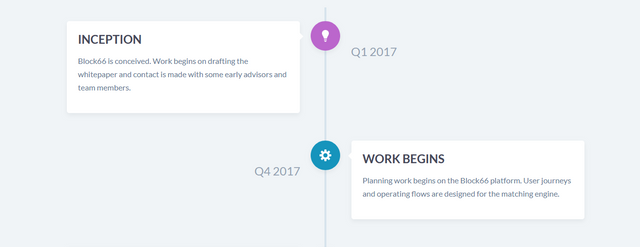

Q1 2017

INCEPTION

Block66 is conceived. Work begins on drafting the whitepaper and contact is made with some early advisors and team members.

Q4 2017

WORK BEGINS

Planning work begins on the Block66 platform. User journeys and operating flows are designed for the matching engine.

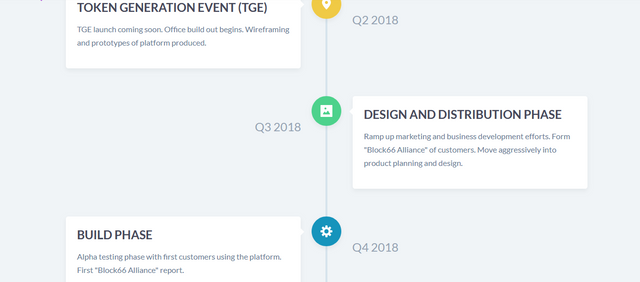

Q2 2018

TOKEN GENERATION EVENT (TGE)

TGE launch coming soon. Office build out begins. Wireframing and prototypes of platform produced

Q3 2018

DESIGN AND DISTRIBUTION PHASE

Ramp up marketing and business development efforts. Form "Block66 Alliance" of customers. Move aggressively into product planning and design.

Q4 2018

BUILD PHASE

Alpha testing phase with first customers using the platform. First "Block66 Alliance" report.

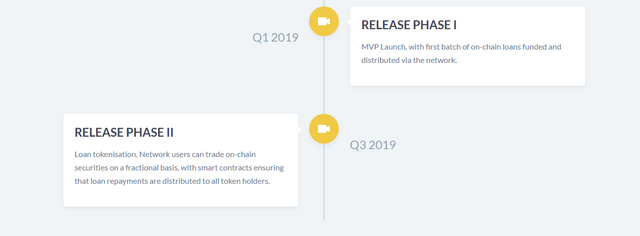

Q1 2019

RELEASE PHASE I

MVP Launch, with first batch of on-chain loans funded and distributed via the network.

Q3 2019

RELEASE PHASE II

Loan tokenisation. Network users can trade on-chain securities on a fractional basis, with smart contracts ensuring that loan repayments are distributed to all token holders.

MEET THE BLOCK66 TEAM

ADVISOR

For more information, please visit:

Website - https://block66.io

Whitepaper - https://drive.google.com/file/d/11ZevZaCwYSG_0iv8On810w3Sjj2E5FLq/view

Facebook - https://www.facebook.com/Block66Official

Twitter - https://twitter.com/Block66_io

LinkedIn - https://www.linkedin.com/company/block66/

Reddit - https://www.reddit.com/r/Block66/

YouTube - https://www.youtube.com/channel/UCHBDzsJ5aKcYr02lrDVxoag

Medium - https://medium.com/@block66

Whitelist - https://www.bit.ly/2tSzMFt

BountyOx : Seunola

MyBitcoinTalk profile: https://bitcointalk.org/index.php?action=profile;u=1925064

ETH Address: 0x3eb48CF7E0A5570540641DD8263cA40e307562e9