Exclusive Research Excerpts: “Why Crypto Assets Should Be Part of Your Portfolio”

The following article is a collection of excerpts from researchers associated with Cipher Assets. Cipher Assets owns the rights to this article. EOI Digital was granted permission to reproduce the article and does not claim ownership whatsoever.

Experts weigh in on crypto asset portfolios in published article not found on the internet.

And while cryptocurrency and blockchain have been making headlines since 2009, experts Zev de Zeeuw (left), Alex Fauvel (middle), and Amadeo Brands (right) have studied its practical uses. Following a series of fortunate events, blockchain and crypto found itself in the spotlight in some years—specifically 2011, 2015, 2017, and most recently in 2019. A local Dutch journal published an article containing the latest cryptocurrency research. And this research hasn’t been readily available online except in this blog.

The aim of this paper is to introduce crypto assets and motivate to include crypto assets in your portfolio.

And while most of this blog will contain excerpts from the text, I will try my best to give a short summary on top before introducing the excerpts.

The Beginning

In this part, we talk about the current digitalization problem, the solution it brings, and current popular use for blockchain. Basically, the world sees blockchain as a medium for digital money. And we thoroughly discussed the initial details of it here.

The Problem It Solves

To answer this, we introduce two concepts which are central to explaining why crypto assets are important:

- Computers can copy digital things perfectly.

- Anything of value that is easily copied is practically worthless.

Ever since the entertainment industry went through its digital transformation, it has been involved in a never-ending battle with piracy. It simply cannot stop anyone from copying and distributing intellectual property (e.g. music and films). Once content has reached a computer outside of the industry’s control, it can be easily duplicated and redistributed. This form of reproduction and distribution, which is considered such a nuisance to the entertainment industry, is prohibitive to the existence of a digital currency. The essential difference between information and value, is that value cannot be in two places at once. As a result, the consequences of allowing unchecked copying and reproduction of value are dire for any monetary system.

Solution

Bitcoin as invented by Satoshi Nakamoto (the pseudonymous person or group that invented the blockchain protocol for Bitcoin) allows different untrusted parties to reach consensus on a common historical truth. Cryptocurrencies have different methods of reaching consensus and thus solving the double-spend problem. In this section we will outline the original design, best exemplified by the Bitcoin blockchain.

It is important to point out that everyone who owns the currency is only able to modify the entry on the blockchain that corresponds to the value they possess. They control this value with a ‘private key’, which allows them to publish transactions to the blockchain.

Transactions on a blockchain are combined in pages of a ledger, called blocks. These pages or blocks are mathematically linked together so that they must occur in the order they are created and therefore remain unchanged. Consequently, everyone producing blocks has access to identical information. Blocks take computational work to create, requiring the consumption of resources (e.g. energy), thus incurring a cost to create. Block producers or the miners get rewarded for updating the ledger with transaction fees and newly created coins (block reward).

If anyone wishes to undo or change a particular transaction within any of these blocks they must invalidate all blocks that come after. To make the change valid, they must remake all the blocks following the change and create more blocks than the rest of the network. This is known as a 51% attack. The act of recalculating blocks (i.e. attacking the network) is economically irrational when compared with the profit that there is to be made by simply acting honestly. Honest miners can also choose to ignore malicious blocks and continue from the last-known valid point, introducing an additional risk to acting against the network. This cost-benefit analysis is the security mechanism of the blockchain. It is not that it is impossible to attack the network but that doing so is economically irrational...

A Store of Value or Medium of Exchange?

...Many believe that the fall of the US dollar, British pound, European euro, Japanese yen, Chinese renminbi or any other established fiat currency is unlikely. However, if we recognise that there is a possibility that weaker currencies such as the Venezuelan bolívar, Argentine peso, or Zimbabwean dollar may fail and be replaced by a kind of cryptocurrency, then we must also recognize that it is possible that more established currencies may someday be replaced by crypto assets.

Competitive Money

...Each money or currency has its own benefits and drawbacks, they can mutate, and they can fail. If currencies evolve due to for example, competition, what would the next generation of currencies look like in this digital information age? Permission-less, decentralised crypto assets could be that next generation, and the central monetary authorities of the world are starting to take notice. In a recent report, Dong He, deputy director of the IMF’s Monetary and Capital Markets Department, wrote:

“If central bank money no longer defines the unit of account for most economic activities – and if those units of account are instead provided by crypto assets – then the central bank’s monetary policy becomes irrelevant.” If there is even a slight chance that this scenario occurs, then the benefit of being exposed to crypto assets by far outweigh the risks that they currently present. If cryptocurrencies truly succeed, modern macroeconomics will have to be revisited."

Different Crypto Asset Categories

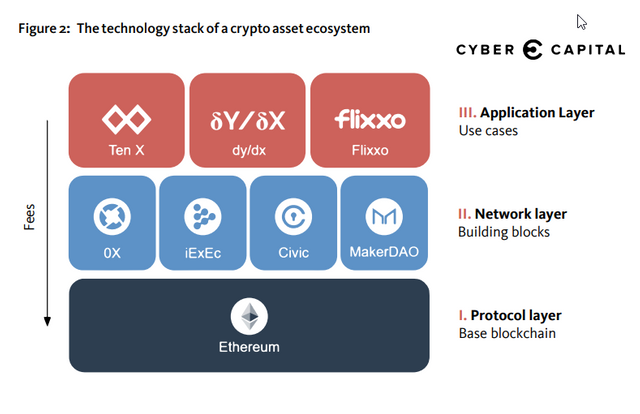

While the first part emphasizes the initial design for blockchain, we emphasized that it has more uses. In this section, we outline the other uses of blockchain. Figure 2 shows a diagram of its possible uses.

1. Protocol Layer

The idea that every token has its own blockchain is a widespread misconception. Services within the network layer are actually built on top of an existing blockchain i.e. the protocol layer. Under a set of very narrow circumstances they might require their own unique token. These network services facilitate the application layer by adding functionality to the protocol in such a way that it allows others to create applications. Example use cases of such network layer services can be data storage, computation, identity management and exchange solutions. This layer is not what consumers will normally be interacting with on a daily basis.

2. Network Layer

The idea that every token has its own blockchain is a widespread misconception. Services within the network layer are actually built on top of an existing blockchain i.e. the protocol layer. Under a set of very narrow circumstances they might require their own unique token. These network services facilitate the application layer by adding functionality to the protocol in such a way that it allows others to create applications. Example use cases of such network layer services can be data storage, computation, identity management and exchange solutions. This layer is not what consumers will normally be interacting with on a daily basis.

3. Application Layer

The third layer is the application layer. This is the layer that consumers mostly interact with. These applications look very much like traditional businesses that provide a service to consumers. At the time of writing, there are only a few functional applications, as the market is still very immature. Yet examples would be businesses like Coinbase, Binance, Facebook, Airbnb, Amazon or Uber.

The next set of paragraphs contain qualitative characteristics like economics models, security, fraud and hack and quantitative aspects like metrics, ratios, returns. These paragraphs contain the bulk of the research and are self-explanatory.

Economic Models

When looking at the complete technology stack, transaction fees are charged whenever layers interact with each other. This starts a chain reaction down the technology stack, where value is captured within each of the underlying layers. When looking at each individual service or token within the layers, they have different value propositions for token coin holders and maintainers of the ecosystem’s infrastructure. As such there are several different economic models (tokenomics). However, we can segment the different models into just two fundamental categories:

Currency

The currency model (i.e. cryptocurrency) makes the most sense for protocol layers, due to its security and network effect. Its value proposition is simply a global currency for use anywhere that accepts it as a form of payment.

To bring a currency into circulation, certain mechanisms exist to determine how and to whom it is distributed. Most mechanisms for protocol layers will distribute the coins to those that contribute resources typically known as miners, stakers or block producers. This is comparable to traditional money creation by a central bank. Some of these currency models do not have any money creation, or only use monetary growth to support maintenance of the network in its early stages. The incentives to continue maintaining the infrastructure would eventually transition into transaction fees, allowing the system to continue.

Securities

Some crypto assets act more like traditional securities, commonly known as security tokens. A share of the revenue or profit, generated by the entity behind the asset, is distributed to the investors in the token. Due to the efficient and transparent nature of the blockchain, this distribution can be done in real time. These more complex security tokens can also sometimes represent a vote on a subject related to the token’s function, just like traditional voting rights of a company. Furthermore, a security token could also represent a real asset, such as gold, fiat currency, or even a share in real estate.

Security, Hacks and Fraud

We also emphasized the security, hacks, and fraud risks cryptocurrency and blockchain has. While the research gave me examples (Mt. Gox, ICO frauds, DAO Hack) of popular security scandals. I will place here the general security description proposed in the research.

Traditional assets typically go hand in hand with custodial counterparty risks. The infrastructure required for such schemes is vast. Fiat currency for example: If a company would wish to store more than 10 million USD, they are unable to do so without oversight and management. However, with crypto assets, security can be as much or as little as one would like it to be. Since the security is based upon randomness of numbers, one of the most secure methods simply utilises some dice and an offline computer. Best practices are still being developed since this is an immature ecosystem. One such development is custodial services for institutions and individuals that do not wish to take on such overhead risk. This is the freedom that crypto assets provide, they do not force people to have a custodian and allow them to maintain their financial sovereignty.

Regulation

Most current crypto assets have no purpose other than to raise funds for the development of new business initiatives and would therefore fall under classic securities law. To circumvent this, the ‘utility token’ was introduced, which has none of the technical mechanics of a security token as outlined previously. Despite this, the objective of raising capital remains the same. Therefore, classic regulation still applies. New classifications are unlikely to be created for these offerings, which makes it likely that most utility tokens available today will be classified as non-compliant securities.

The Commodity Futures Trading Commission (CFTC) and the Securities and Exchange Commission (SEC) have made statements detailing their initial intentions to regulate crypto assets. These intentions seem to be that ICOs will be treated like classic IPOs, i.e. security offerings, whereas sufficiently decentralised protocol layers could be classified as commodities. It is as of yet unclear how a sufficiently decentralised protocol layer that previously performed an ICO will be treated within this legal framework.

Metrics, Performance & Risk

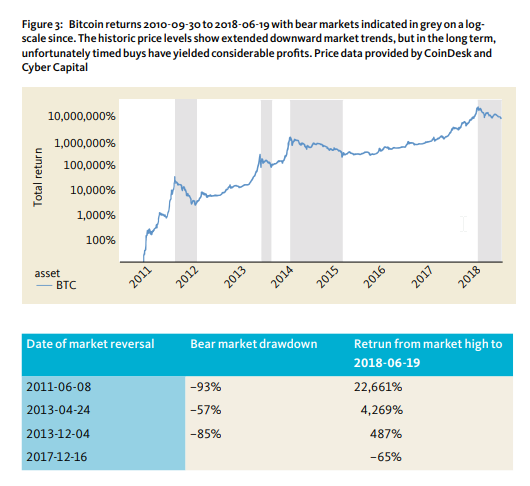

We believe the crypto asset class has the potential to be the best performing asset class for the next five years in terms of return on investment. However, such potential does not come without risk. In this section the equitability of the crypto asset risk premium will be evaluated. It should be noted, that the immaturity of this market means that there is a limited amount of data. Bitcoin, being the most mature asset, will be the focus of the following analysis.

Returns

Bitcoin has increased considerably in value since it first started trading in 2010. This historic rise has not been without its corrections. [We] have highlighted market reversals and shown that even when buying bitcoin at the peak of each cycle, substantial returns have been made.

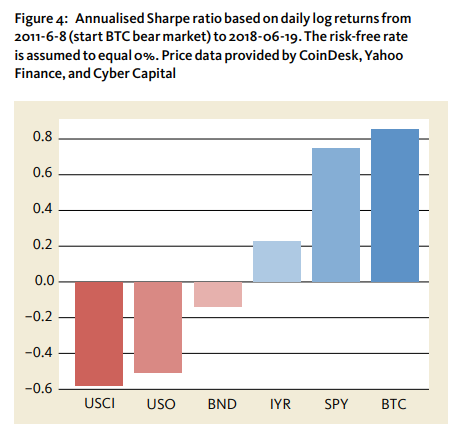

Sharp Ratios

To evaluate the crypto asset risk premium, we use the most popular risk-adjusted performance metric, namely the Sharpe ratio. In figure 4, the Sharpe ratio is provided for five traditional asset classes and Bitcoin (BTC) based on daily log returns from the June 8th 2011, the inception date of the first indicated bear market, until June 19th 2018. The other five assets are the United States Commodity Index (USCI), United States Oil Fund (USO), Vanguard Total Bond Market ETF (BND), iShares US Real Estate ETF (IYR), and SPDR S&P 500 ETF (SPY). The figure shows that BTC has an excellent Sharpe ratio similar to that of the S&P 500. Thus, from an investment perspective Bitcoin’s high volatility is transcended by its annual performance.

Protocol and Network Layers

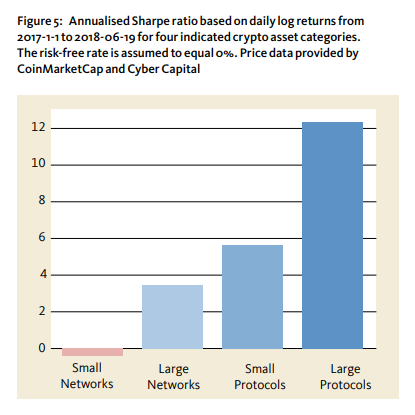

In Figure 5, we have analysed the difference in the network and protocol layer’s annualized Sharpe ratio. As of 2017-1-1 the application layer is only very meagrely represented in the top 100 crypto asset market capitalisations. Therefore, we have elected to omit this layer completely. We also separated large and small projects by respectively the top 20 and 21 to 100 in market capitalization. Clearly, protocol layer coins appear to perform better. This is in line with the perspective that this market is young, and the foundations of the technology still need to be solidified before further constructs are built on top. It can also be observed, that smaller assets perform worse on average. There seem to have been a large number of low quality projects in the top 100. But they are likely being identified as such by investors before reaching the top 20

Correlations and Volatility

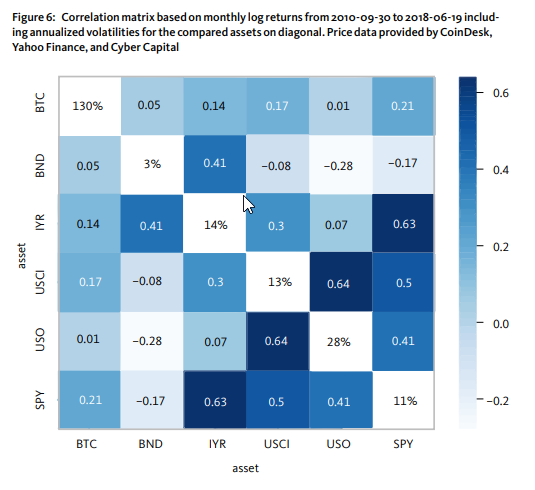

When examining the correlation matrix (figure 6), we can see that all traditional asset classes have a correlation of at least 0.41 with at least one other asset. Yet, Bitcoin has a maximum correlation of 0.21. This makes the role of Bitcoin in one’s portfolio irreplaceable. As indicated in the Sharpe ratio section, crypto assets provide a good risk return balance on their own. Furthermore, we can see that the correlation with more traditional investment classes indicate great potential for portfolio diversification benefits.

More than Meets the Eye

While the research (and this excerpt) is lengthy, it does give out certain points to cryptocurrency and blockchain. Though right now it’s currently used another form of fiat, we all agreed that blockchain has more than one uses. It’s current difficulty is the roadblocks of security and risks that undeniable irks some, but the benefits of diversification and digitalization outweighs the benefits.

Posted from the EOI Digital Transformation and Marketing blog : https://transform.eoi.digital/exclusive-research-excerpts-why-crypto-assets-should-be-part-of-your-portfolio/