Hackers' Guide to Thai Land Acquisition

ABSTRACT: It is a highly controversial topic whether it is (still) a good idea for a foreign investor to use a Thai company to hold real estate in Thailand – or whether a leasehold investment is the only remaining option. This article explains that under a typical scenario real ownership through a Thai corporation is the preferable and most reliable investment structure. The threatening full application of existing laws and regulations (a.k.a. crackdown) is not a game changer. Foreigners can smartly invest in Thai land ownership and this guide shows how to do it in full compliance with the laws and regulations of Thailand. YES, WE CAN DO IT LEGALLY.

Under the laws of Thailand there are no legal or regulatory restrictions for foreigners to buy real estate. A sale and purchase contract for land is unquestionable valid and often a necessary and advisable element in a smart investment strategy. However, such purchase contract should include a clause under which the buyer will now or later direct and instruct the seller, who the acquirer and legal owner of the land should be.

How to understand the foreign investment restrictions in Thai property

The Foreign Business Act is the primary statute, which restricts foreigners from conducting certain types of business activity in Thailand. The Foreign Business Act further governs the extent of foreign ownership in Thai entities carrying out such business activities and restricts Thai nationals from assisting foreigners and foreign-owned entities from acting as their so-called “nominees” or taking other steps to enable foreigners and foreign-owned entities in conducting the restricted business activities prohibited to foreigners under the Foreign Business Act.

The Thai Land Code sets forth legal principles applicable to real estate matters in general and the rights related to holding title to land in particular. Application of the Land Code to a specific transaction or set of facts depends on the application of numerous ministerial regulations and internal departmental rules of the Land Department. In addition to the Land Code, ministerial regulations and internal departmental rules, each of the Provincial Land Offices have their own custom and practice, which is not uniform throughout the country. Furthermore, if an ambiguity exists in the wording or application of the law, Land Department officials may exercise reasonable discretion in implementing the law.

Both Thai nominees and foreigners employing nominees are subject to significant civil and criminal sanctions under the Foreign Business Act: (i) fines to up to one million Baht and/or (ii) imprisonment for a term not exceeding three years. If nominees or foreigners who employ nominees fail to carry out a court order, the company and/or person who violates such court order is liable to a further fine of up to fifty thousand Baht for every day during the violation continues. Individuals found guilty of violating the Thai Land Code or acting as nominees of the foreign nationals, including directors of a company which has violated the law, are subject to one or both of the following criminal sanctions: (i) a criminal fine of twenty thousand Baht per violation, and/or (ii) a term of imprisonment not to exceed two years.

How to use the remaining Thai land acquisition options legally

According to Section 86 of the Land Code of Thailand, foreigners may acquire land if this is allowed by a specific treaty, a regulation, specific statutes such as the Board of Investment Act, the Industrial Estate Authority of Thailand Act and the Condominium Act, if they invest a premium payment of THB 40 million or in case of an inheritance plus ministerial permission as well as [add other most unlikely cases]. In the typical case, a foreign investment does not meet any of these criteria. Therefore, from a practical point of view foreigners can‘t acquire Thai land. That’s the law in Thailand and quite similar in other ASEAN countries.

However, Thai persons are allowed to acquire and legally own real estate. A Thai corporation does qualify as a „person“ as well and a Thai limited company (Co., Ltd.) can perfectly hold and own real estate, even when the shareholders are not 100% Thai persons. It is no secret that most of the luxury villas situated on Thai islands or other touristy places belong to Thai companies with foreign co-shareholders. The same is true with respect to hotels, resorts and certain other industries and areas.

Although it is clearly possible to structure the transaction the legal way, it is a well-known secret that a substantial percentage of the corporate land holdings are not in line with the foreigner legislation and regulations in Thailand and simply illegal. These ill-advised structures have to fear a crackdown by the new government which threatens to apply the existing laws not only to new real estate acquisition projects but also to existing corporate land ownerships. It is the visible reality in Thailand that illegal buildings are demolished and the government screens the land offices and local company registers for abnormalities and conspicuousness.

The following article addresses some legal aspects of land ownership by foreign shareholding in Thai limited companies. It comes to the conclusion that this acquisition model has to carefully meet certain requirements to be protected against a non-registration, but also against a later crackdown. However, if professional designed and clever accomplished, a comfortable and risk-averse structure can be achieved for the land acquisition from a Thai seller through a newly set-up company and for the acquisition of shares in a land holding company.

How to set-up a foreign co-owned Company Limited

A Thai Co., Ltd. needs three or more shareholders and one or more directors. The directors have to be individuals, but there is no requirement for them to have Thai nationality or to be resident in Thailand. The details of the company formation are described and documented in the Memorandum of Association (Articles of Incorporation) and the details of the corporate regulations are agreed in the By-laws (Articles of Association). Further conditions apply.

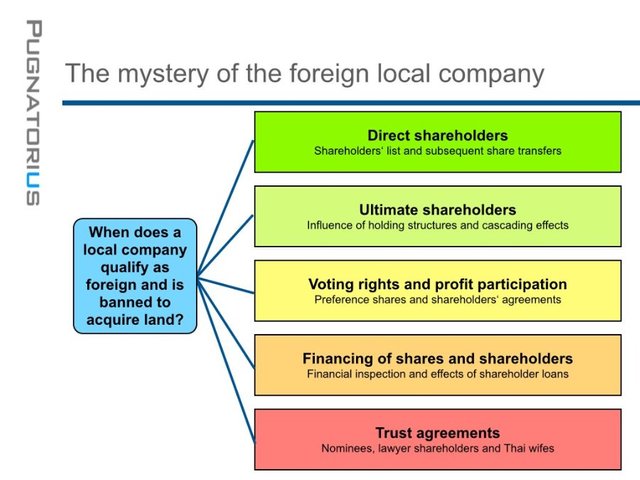

Foreign individuals and non-Thai companies are not allowed to be majority shareholders, if, above other activities, the company intends to acquire and hold real estate. While a foreign individual is clearly identified by his non-Thai passport, it is not so clear what a company duly registered under the laws of Thailand qualifies as foreign. In general, the law might gear to the direct or ultimate shareholders, distinguish between asset allocation, voting rights and profit participation, may consider the company‘s financing and the financing of the shareholders by foreigners. In addition, shareholders agreements, trust agreements and other limitations might be relevant. Luckily, the laws of Thailand concentrate on the asset allocation by the direct shareholders and everything else is under the current FBA legislation mostly ignored.

A simple company set-up („consumer grade investment“) is a skeleton building shell without windows and floor cloth, not ready for the foreign investor to move in. As a minority he is permanently at the Thai shareholders‘ mercy and could be easily ousted. He has insufficient rights to protect his investments and the payments made are seriously at risk. Therefore, there is an urgent need to improve his legal and factual position to obtain an investment grade corporate structure. The laws of Thailand are flexible enough to allow and enable such intention, without contravening Thai foreigner legislation. Therefore, such improvements could be characterized as „White Hat Tactics“, an Internet slang coined for methods to justified improvements of data security and website visibility.

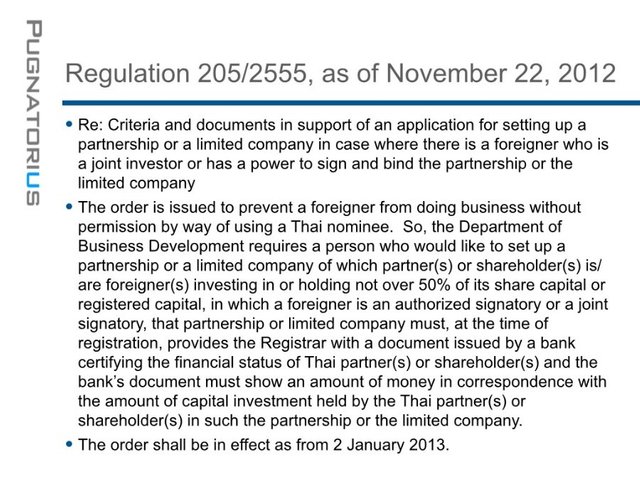

The Thai military government recently introduced new rules for the capitalization of the Co., Ltd. Order 13/2558 requires specific evidence that the registered capital has been paid in by the shareholders. The written confirmation by the director, that the equity amount is at his free disposal, is no longer sufficient. Instead, additional evidence is required. Proper supporting documents may be a bank statement in case of a cash contribution, a transfer agreement in case of a contribution in kind or any other documentation which supports the contribution value and the proper asset allocation to the new company. Details are promised to be published soon in a comprehensive guideline by the Ministry of Commerce. The new rules are effective (i) for any company set-up or capital increase carried out after February 2. 2015 and (ii) above the threshold capital amount of THB 5 million.

How to avoid to phreaking in the darknet of nominee-suspicious activities

Unfortunately, the legal limits and restrictions of white hat corporate tactics are often misunderstood or not taken seriously enough. Under the sceptical monitoring by the new government, failures in structure and performance are incriminated as illegal nominee arrangements or, in other words, as „Black Hat Tactics“. Obvious cases are (i) performance of a void agreement, (ii) non-compliance with concluded agreements and (iii) performance that has no other economic purpose than to avoid the nominee restrictions.

The experiences of the last years, what could qualify a Thai shareholder as a nominee, are mixed and confusing on the first site. Therefore, it is a cardinal question, where the red line is located. There are on the one side unjustified nominee accusations which have to be clearly rejected. And there are on the other side specifics of the case which have to be avoided because they justify the reasonable nominee suspicion. This is further illustrated by the following two examples:

Thai corporation laws explicitly allow different classes of shares. A preference shareholding structure in which the Thai shareholder receives a guaranteed dividend but has limited voting rights is perfectly in-line with this and, therefore, should not be seen as a little bit black hat. In contrary, if there would be no preference structure in place and the Thai shareholders do not receive dividends in accordance with their quota, such non-compliance with the company regulations is a strong indication that the Thais are nominees.

Contractual agreements, including leases, financings and usufructs between a married couple are perfectly legal and there is no conflict of interest that limits this. The legal cancellation right under Section 1469 CCC does not change this legal analysis. Acting within the framework of the laws should not be discriminated as indication for breaking the foreign investment legislation.

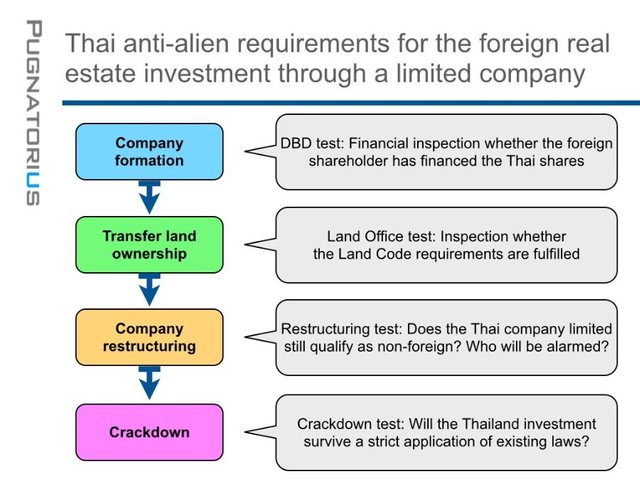

How to avoid zero-day vulnerability when registering the land holding company and transfer the land ownership

Under the laws of Thailand, a Thai company is entitled to acquire and hold real estate, if (i) 51% of the shares are in aggregate held by Thais, (ii) there are not more foreign shareholders than Thais, and (iii) the Thai shareholders do not qualify as nominee under Thai regulations. While conditions (i) and (ii) are hard facts, the third requirement has to be seen as a soft fact which is open to a wide scope of interpretation. As a consequence, the Thai government publishes announcements and decrees to support the Thai community to follow the rules and regulations.

Under the current anti-nominee rules and policies for 2013 and 2014 (which are not made especially for real estate investments) the company formation requires that the Thai shareholders provide additional documents, if (i) the company has foreign minority shareholders (even 1% only) or (ii) the company has a foreign director or (iii) the company has foreign financiers. In these cases, Thai shareholders have to supply a bank statement to certify the financial standing by bank book or credit advice by commercial bank upon the incorporation registration.

Sun Tzu, nowadays you might call him an elite hacker, teaches that the supreme art of war is to subdue the enemy without fighting. Therefore, the easy way to register a company intended to acquire land is to show no foreign participation on day one. This includes (i) no foreign shareholder, (ii) no foreign director and (iii) no foreign loan in the opening balance sheet. Without any foreign contact surface there should be no need for showing any piece of evidence because there is no foreign element visible.

Such procedure is advisable even in the event of a financial inspection would green-light the transaction and is, therefore, no indication for a nominee issue. It is just a reasonable time and cost saver for all participants. But even if the Thai shareholders have to sell the family jewelries to finance the equity distribution – or if they look for a loan financing from a bank, a third party or the foreign-co-shareholders – this would make no difference. The nominee accusation would be relevant only, if (i) the equity payment is granted without a valid loan agreement in place, (ii) if the loan conditions do not meet market conditions or (iii) if the companies assets – especially a mortgage in the real estate – are misused as collateral for the loan repayment claim.

The intention to restructure the company later and to modify the shareholders’ list after registration is not any fact or circumstance to be legally disclosed to the company register (DBD) at the point in time the company is registered. And it is no black hat operation by itself, if such intentions and plans are not disclosed at the land office on the day, the land acquisition is registered. After the land deal is sealed, the share transfers might be executed and when the new shareholders list is registered at the DBD there is no requirement either to explicitly highlight the fact, that the company in the meantime acquired real estate. The registration typically will be accomplished on a „no questions asked“-basis.

How to avoid a crackdown after the land acquisition is accomplished and the corporate structure is in place

If the foreign investor successfully avoided the financial inspection by the DBD, passed the ownership registration at the Land Office and even managed to receive his minority shares, he might feel relaxed. But he might be already under the screening by the DSI Department of Special Investigations which start a crackdown at a point in time convenient (for the government, not the foreigner). Therefore, it quite essential to be prepared to the last step.

There is a whole darknet of criteria and toolkits to define, which company has to be classified as high-risk. This starts at the shareholding quotas, the place of residence of the Thai shareholders and certain ill-advised clauses and structural particularities. In the event of a crackdown, these company files will be reviewed and tough questions asked. It will depend on a case-by-case decision whether the consequences will just be a time limit of a half or full year to get a restructuring done or whether assets are seized and companies are put on ice.

How to disagree to foreigner discrimination by a hidden dual pricing system behind anti-nominee arguments

The full enforcement of Thai corporate legislation might be the chance to wave farewell to some very cherished prejudices, which hide a dual pricing system behind anti-nominee arguments.

It is one of the proven real estate strategies all over the world to separate risk-avers land ownership in a separate corporation and, therefore, not to combine the land holding business with risky trade activities. A prudent businessman will not accept that trade business partners and creditors for the trade business have access to real estate as an additional collateral. It would be highly unreasonable if Thai anti-nominee regulations would require that a foreign co-owned land holding company has to act uneconomical and irrational by doing trade activities in the same corporate entity and, as a result, put the whole real estate investment at risk.

It is an unprofessional misinformation that Thai legislation requires that a partnership or company declares profits and pays taxes. Section 1012 CCC does not at all prescribe that “the purpose of forming a limited liability company is to make profit”, even if such false statement is published by unreliable legal sources. Instead, the purpose as described by Section 1012 CCC is “to unite for a common undertaking, with a view of sharing the profits which may be derived therefrom.” – and that is obviously something very different. Profits are intended over the overall lifetime of the company and there is no requirement that the business shows profits in its yearly balance sheet or pays taxes each year. It is the characteristic of real estate operations that the land keeps its book value and the buildings and other improvements are depreciated and, therefore, balance sheet losses occur year by year. In contrary to tax losses the market value increases and the hidden reserves are not taxes before the real estate is sold by the company. It is perfectly understood by Thai owned businesses that a company is a company even if it is dormant. It would be highly unreasonable if Thai anti-nominee regulations would require – they do not – that a foreign co-owned land holding company generates after a three years start-up phase yearly taxable profits, while this requirement is not made for 100% Thai owned real estate investments.

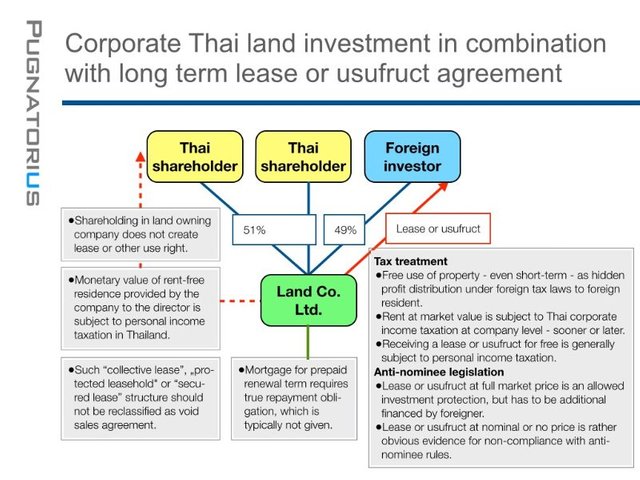

Can it be harmful for the shareholder in a property holding company, if he enters into a long term leasing agreement for the land? Lease combined with share holding may be branded as a “collective lease” or a “secured lease”. Lease agreements are the white hat investment tools and recommended by the government for a foreign “buyer”. Based on recent jurisdictions there might be the weird argument, that an investor who leases from a limited company and in addition acquires shares in that land owning entities, from an economic point of view purchases the land. Thai courts based on Section 155 CCC their legal opinion that a lease agreement plus share acquisition equals to a land acquisition. Since the land acquisition of the lessee is not duly registered, it is void. Even the lease agreement is void because it is a fictitious transaction under the law.

For these and other structural issues, a discrimination of companies with foreign minority shareholders against companies with 100% Thai shareholding is not justified and it is hard to believe that a Thai court would make such difference.

How to lease or not to lease the property to the foreign shareholder

It is one of the basic characteristics of a corporation that it distinguishes and separates the company level from the shareholders level. Assets owned by the company cannot automatically be used by the directors or one or all shareholders. In a foreign co-owned land holding company the foreign investor would be surprised if the Thai majority shareholders move in the villa and deem themselves the landlord, host, beneficiary or holder of use rights. However, the investor should understand that he himself has such legal position neither.

In practice, the foreign investor will reside in „his“ villa based on an informal lease for free. Such short term lease is effective without the requirement of written form or registration at the land office.Thai tax authorities traditionally have a blind eye with respect to loss of short term rent income and did not charge corporate income taxes until now. However, the “monetary value of rent-free residence provided by the employer” is generally subject to personal income taxation under Section 40 (1) of the Revenue Code.

Some corporate land holding structures include a 30 years land lease between the company and the foreign investor. However, it has to be taken into consideration that a prudent businessman will not donate such long term lease or usufruct and, therefore, such agreements have to reflect market value and will not come for free or a nominal amount. If the company purchases the land and immediately leases it out to the foreign shareholder, it needs convincing arguments to agree on a renumeration substantial below the purchase price. Such amount has to be financed by the foreigner and transferred to „his“ company. On the company level it has to be decided wether it is immediately booked and taxed as profit, whether it has to be allocated and taxed on a straight-line basis during the lifetime of the agreement or should be booked as investment.

The registration of the lease at the local land office without any substantial renumeration will sooner or later result in a tax claim at the level of the company of 20% of the land purchase price, because this is the current corporate income tax rate. Additional taxes might occur if a distribution of the amount immediately back to the foreigner is deemed and 10% withholding tax has to be paid for such dividend. Another aspect to be carefully considered is under which circumstances the donee has to tax this benefit under Thai income tax legislation. Apart from these tax issues it should be noted that it is rather obvious that a free long term lease for the sole benefit of the foreign minority shareholder is a clear indication for a nominee structure. Especially the foreign shareholder who enjoys an undervalued lease should be aware that he sits on a ticking time bomb by putting the nominee evidence too obviously on display, and will be one of the first ill-advised victims under a crackdown scenario.

Rent income from a property lease is subject to Thai taxation (Sections 41, 43 RC). If the lessee is a corporation or the lessor is not resident in Thailand, the lessee has to deduct withholding taxes at a rate of 5% (corporation case) or 15% (non-resident case). A local employee, agent or go-between of a non-resident corporation as a lessor results under Section 76bis RC in the corporation’s liability to file tax returns and pay taxes on the rental income, subject to the provisions for a permanent establishment by an agent in the respective double tax treaty (typically in Article 5). The local employee, agent or go-between is in this case jointly liable for any Thai tax obligations.

How to understand the cross-border risks when hacking the tax laws abroad

If a shareholder or director is permanently resident outside of Thailand, the investment structure has to be carefully designed taking into consideration cross-border tax aspects. Experience shows, that the tax consequences in the investor’s home tax jurisdiction are often neglected and ignored.

The non-Thai tax jurisdiction may qualify the rent free stay of a foreign resident in „his“ villa in Thailand as a hidden profit distribution by the Thai limited company and such foreign hidden dividend distributions may be subject to taxes in the investor’s country as income from foreign sources. Under such scenario, basis for taxation is the third party market value without consideration of saved expenses. Such non-Thai tax treatment may be enforced even if the Thai tax authorities ignore the case and do not tax the company.

Under the laws of the investor’s jurisdiction the tax residence of a corporation may be deemed at the company’s registered seat (incorporation test) and, in addition, at the location where the top management decisions are made (management and control test). Various national tax legislations define corporate residence choosing a factual test of where the central management and control actually abides. Therefore, the residence of the sole director may constitute a second tax residence of the company outside of Thailand. This results in a situation where the Thai company is taxable in Thailand, but also in the home jurisdiction. Whether such juridical double taxation can be avoided has to be decided on a case-by-case basis. Article 4.3 of the OECD Model treaty provides that legal entities are resident where the effective management and control is located. By contrast, the U.S. Model Treaty uses the place of incorporation as the preferred criterion to assign tax residence.

Based on the foreign tax implications mentioned above, a change of directors – or even of the company’s regulations – may result in a tax-wise cross-border-relocation of the company under the home country’s tax rules. Therefore, an ill-advised repair restructuring might result in a full taxation of the company’s overall hidden reserves without generating liquid funds for the shareholder. Such hidden foreign tax risks need to be part of a comprehensive due diligence in case of a real estate investment by an acquisition of shares in a land holding entity.

Under the laws of the home jurisdiction it is not uncommon to require the foreigner to immediately report a participation in a foreign corporation, if certain threshold amounts are achieved. If such legal notice requirement is not observed, this might be no tax crime but just a minor regulatory offense. However, experience shows that tax authorities qualify such non-reporting as strong indication for a criminal mind of the taxpayer and, as a result, will not accept asserted lack of knowledge of the tax consequences mentioned above by the tax payer.

Tax risks have the character to become visible years after the corporate structure has been implemented. However, the company register at the Department of Business Development is transparent even for foreign tax authorities and the long statutes of limitation for tax avoidance will assure that tax inefficient structures are sooner or later disclosed and the tax bill including handsome penalties and interests is presented to the foreign investor.

How to avoid the total loss of the Thailand investment while fulfilling Thai foreigner legislation requirements

Compared with the vague risk of a financial and corporate inspection of the company by friendly governmental officers with the requirement to adjust the shareholding and other corporate structures, the loss of foreign investment by non-cooperative Thai majority shareholders is by far the greater risk. The investor should be aware that the more cooperative his local law firm acts vis-a-vis DBD and land office, the weaker his protection will later be, if the Thai shareholders decide to sell „his“ villa, to request dividends and capital gains, to approve huge costs and expenses which do not benefit the foreigner or do other nasty things which result in a nightmare for the investment.

Pretended governmental restrictions are often mentioned by local counsel to avoid a cumbersome but proper structuring of the real estate investment. Experience, knowledge of the Thai laws and street wisdom know that without a strong corporate governance mechanism each real estate corporate structure by a foreign investor is sooner or later at risk. This includes white hat tactics as, above all,

dedicated registered AOA (Article of Association, By-laws) with respect to shareholder resolution mechanisms, share transfer restrictions and certain other provisions in deviation from the Thai majority friendly regulations under the CCC,

a non-registered dedicated shareholders’ agreement which on the one hand mirrors restrictions under the AOA and MOA (Memorandum of Association) and on the other hand provides additional foreign investment protection,

a preference share structure with weighted voting rights or other shareholder grouping mechanisms implemented in the MOA, the AOA and/or a separate shareholders’ agreement,

regulations which specify the powers of the company’s authorized directors, the names and number of authorized directors and the manner in which the company binds itself contractually, all implemented in the MOA as well as the AOA,

limited business objectives which are registered in “Form Wor” as part of the MOA,

specific marked share certificates clearly (in Thai and English) indicating transfer, voting and other restrictions,

financing package which reflects the loan agreements between foreign and Thai shareholders,

a share pledge agreement combined with physical possession of the share certificates by the foreign shareholder,

a comprehensive shareholders’ agreement containing a list of major business decisions requiring prior approval from the shareholders by supermajority approval and may address other issues such as buy-sell provisions, pre-emptive rights, distributions to shareholders, and

other matters, other tools and modules, customized to the shareholders’ structure, the investors needs and local practice of the Land Departments and Provincial Land Offices.

Experience shows that such proven and tested corporate governance mechanisms are underestimated and highly neglected, although it can make for the foreign investor the difference between to have and have not. However, the most unbounded cheek and impertinence is the n00b‘s recommendation to trust in signed blank share transfer instruments, which are illegal, ineffective and practically useless. Worthless blank share transfer agreements turn more foreign investments into a financial nightmare than all the bars in Pattaya.

Secure your place in paradise! This post has been published at https://www.linkedin.com/pulse/20141002110310-11220814-hackers-guide-thailand It is legal to set-up a Co., Ltd. with the sole purpose to acquire real estate.