The 7 Things You Need To Know From The Valuing Cryptocurrency Conference Call

The 7 Things You Need To Know From The Valuing Cryptocurrency Conference Call

<iframe width="560" height="315" src="

While the big take away from the call for me was how early we are in the development of valuation methodologies for cryptocurrency, I was immensely impressed by the thoughts shared by the four speakers. Below are what I believe to be the seven most important thoughts shared on the call. The 2nd, 3rd, and 4th thoughts below are pretty dense/include a lot of math, the others are more macro.

- The cryptoasset market can be broken in to three distinct assets:

Ryan Selkis stated that the biggest problem in the market today is that everything is valued as if it’s a currency/a store of value. This mis-categorization has lead to grossly overvalued cryptoassets in the long tail as there will only be a couple of winners for the money use case

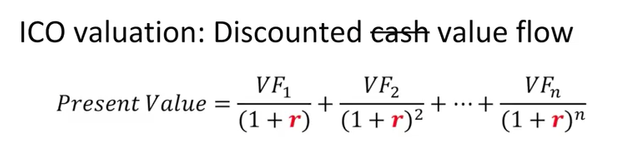

2. A first step in valuing a coin is valuing the entity/ICO by using traditional valuation methodologies and substituting “value” for “cash”. In traditional investment based DCF (discounted cash flow) analysis, the value of an asset is based on an estimate of the future cash flow it will generate, discounted back to the present based on the expected return (r). While utility tokens don’t offer cash flows, they do offer a “flow of value” (VF) that can be substituted for cash flow:

While estimating the VF can be challenging, estimating the expected return (r) is even more challenging. The traditional Capital Asset Pricing Modelmethod estimates “r” via the equation

r= Risk Free Rate + Beta x (Expected Market Return — Risk Free Rate)

Beta (B) is a measure of the volatility, or systematic risk, of an asset in comparison to the market as a whole. Beta is hard to estimate for crypto because the assets haven’t been around long enough to have enough data for analysis. And the data that does exist hasn’t been very stable. There is also significant regulatory risk that needs to be accounted for that can’t be addressed via diversification, as it’s inherent in all cryptocurrency.

3. When doing comparative analysis between different crypto assets, an early metric used for the analysis is “on-chain transaction volume”.

The equation above (known as “Network Value to Transaction Volume Ratio”or “NVT”) can be used to estimate the value of cryptoasset “j” by comparing it to the value of crypto asset “i”. This assumes that transaction volume is priced the same across different crypto assets. The equation also also assumes that on-chain volume is a proxy for demand for that asset.

However, we don’t really know how relevant on-chain transaction volume is across protocols (say Bitcoin and Ether) or in a time series (e.g. Bitcoin 2015 vs. Bitcoin 2017). There’s much work to be done here, but we do seem to have the beginning of a framework for comparative analysis.

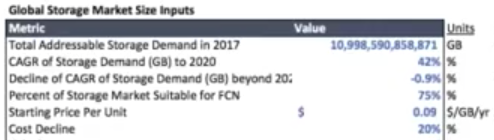

4. Chris Burniske’s Utility Token Model Is A Remarkably Thoughtful Tool.Chris started his talk by noting that the Filecoin model was not meant to set a price target, or as investment advice, but it allows him to put the underlying value drivers in to perspective.

Chris’s started by reviewing a series of storage market and Filecoin specific assumptions including market size, market growth, and Filecoin pricing:

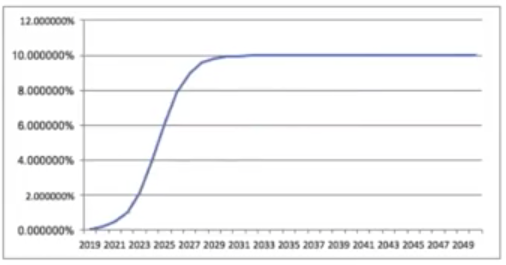

Chris then shared the “S-curve” aspect of this valuation methodology, which yields his estimate of market penetration over time. The rapidly climbing “S-curve” below, which Chris shared, was just an example, and is likely more aggressive then he’d estimate.

Chris’s model can now project the annual dollar turnover facilitated by Filecoin.

The next step is to estimate the coin’s velocity. In monetary economics, velocity refers to the number of times an asset turns over per year. Chris estimates a velocity of “4” for the Filecoin token, given the fact that Bitcoin has averaged a velocity of between 4 and 5 over most of it’s life. The simple math takes the dollar turnover divided by the velocity, to determine the “Network Value”. This leads to the perplexing anomaly that the more a token is used for utility purposes (thus the higher velocity), the lower the Network Value.

The Network Value is then divided by the number of tokens in float, to get the “Current Utility Value” of the token. The current market price of a token is then based on taking Current Utility Value of the token plus a Future Utility Value of the token discounting it back to the present. Chris took the estimated utility value of a Filecoin in 2029, and discounted it back by 25% (r), over 10 years, to get a Future Utility Value of $2.48 in 2019.

Chris finished his discussion by highlighting how the 2019 Filecoin value broke out between the it’s Current Utility value ($2.24 or 47% of the total value) and the Discounted Expected Utility Value (or the store value component) of the cryptocurrency ($2.48 or 53%):

Again, as Chris noted at the start of his talk, this is not a price target, but is helpful in understanding the impact the different valuation drivers have on the value of the coin. Chris noted that having more than 20% in current utility value is above average, as many tokens don’t have a current product so they can’t have a current utility value. If you find this math hard to follow here, Chris does a good job of walking though it on the call.

5. Uncertainty remains in the asset rotation thesis that money will flow out of gold in to Bitcoin (as it represents a better store of value). Many pundits estimate the value of Bitcoin by simply guessing it will get to 5% or 10% of the value of gold (which is currently about $8 trillion). Stephen pointed out that it’s not clear whether asset rotation from gold to bitcoin is occurring yet, and that we don’t have data on the topic. Stephen further pointed out, that even if you believe in the asset rotation thesis, it’s possible it could flow to Ether, Zcash, Monero, or other stores of crypto value.

6. The crypto accessibility discount is under-appreciated.

Ari’s discussion focused on the fact that as tokens become easier to buy, price appreciates.

For example, until recently, Coinbase only enabled the trading of Bitcoin and Ethereum. On May 3rd, when Coinbase announced and enabled the trading of Litecoin, it rallied 32%. That’s after Litecoin had rallied more than 300% in the preceding two months, as word likely leaked of Coinbase’s plans. In the week following an announcement by Bithumb (the largest South Korean exchange) that it would begin trading Monero, that coin appreciated 145%.

Ari also highlighted how greater accessibility is driving the ICO boom. The emergence of ERC20 not only made it easier to create ICOs by leveraging the Ethereum network, ERC20 also made it easier to invest, as once you’ve invested in one ERC20 ICO, it’s pretty simple to invest in the next one.

7. There is a massive amount of institutional demand for cryptocurrency waiting in the wings. Ari estimates that more than $100 billion in new cryptoasset demand from institutional investors would emerge if several obstacles were removed. $100 Billion represents less than 0.3% of the institutional assets managed by just the top 140 asset managers.

Obstacles include the lack of third party qualified custodial services. As a result, crypto investors have to self custody assets today. That’s not an option for most institutional investors. There is also a lack of institutional quality investment vehicles such as ETFs. Ari believes more than $100 billion would flow in to a well constructed index ETF of the 10 largest cryptocurrencies, in the first year, if the operational risk was dis-intermediated and insured by a third party and if the ETF was issued by a bulge bracket bank. As a result of this massive latent demand, Ari thinks there is a large accessibility discount across the cryptocurrency asset class.

Ari believes that this institutional accessibility discount will decline over the next three years with the emergence of crypto fund managers with track records, institutional quality investment vehicles, and third party custodial services. Ari thinks the early institutional movers could include Canadian and Scandinavian pension funds as well as sovereign wealth funds.

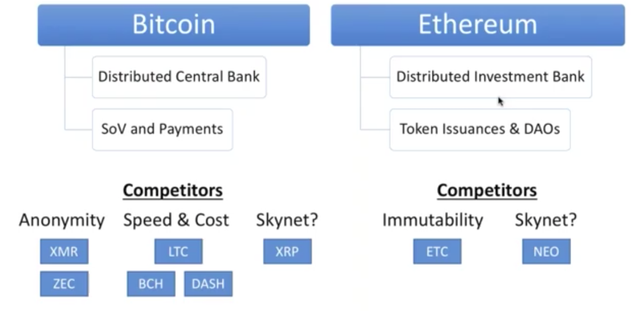

8. Ryan provided a good framework to think about the competition among cryptocurrencies to be the leading digital money/store of value:

Ryan started his talk by putting the attributes of money in to perspective (e.g. recognizability — how much adoption does a given currency have, how many exchanges and wallets support it and how “liquid” is it). Ryan then put forth some context for how different cryptocurrencies are trying to compete against Bitcoin. Monero and Zcash are competing by making their currency more censorship resistant and private. Litecoin, Bitcoin Cash, and Dash are competing by being faster and more and cost effective, which is key to being a payment rail. Ripple is trying to be more recognizable, so others, like central governments, could use Ripple as an international reserve since participants in the Ripple network are all known.

Interestingly, Ether has become a reserve currency of distributed investment banks/investors who issue Ether for token issuances.

Congratulations @fatos! You have completed some achievement on Steemit and have been rewarded with new badge(s) :

Click on any badge to view your own Board of Honor on SteemitBoard.

For more information about SteemitBoard, click here

If you no longer want to receive notifications, reply to this comment with the word

STOPHello & Cheers!! I'm a content detection and information bot. You are receiving this reply because a short link or links have been detected in your post/comment. The purpose of this message is to inform your readers and yourself about the use of and dangers of short links.

To the readers of the post: Short links are provided by url shortening services. The short links they provide can be useful in some cases. Generally their use is benign. But as with all useful tools there are dangers. Short links can be used to hide all sorts of things. Quite frequently they are used to hide referral links for instance. While not dangerous this can be deceptive. They can also be used to hide dangerous links such as links to phishing sites, sites loaded with malware, scam sites, etc. You should always be extremely cautious before clicking on one. If you don't know and trust the poster don't click. Even if you do you should still be cautious and wary of any site you are sent to. It's always better to visit the site directly and not through a short link.

To the author of the post: While short links may be useful on some sites they are not needed on steemit. You can use markdown to format your links such as this link to steemit. It's as simple as

[steemit](https://steemit.com)Unlike short links this allows the reader to see where they are going by simply hovering over the link before they click on it.