How blockchain technology evolve in the lending industry?

How the blockchain technology evolve?

Blockchain is no doubt a hot spot recently. A blockchain is a digitized, decentralized, public ledger of all cryptocurremcy transactions. Constantly growing as ‘completed’ blocks(the most recent transactions) are recorded and added to it in chronological order, it allows market participants to keep track of digital currency transactions without central recordkeeping. Each node (a computer connected to the network) gets a copy of the blockchain, which is downloaded automatically.

The words block and chain were used separately in Satoshi Nakamoto’s original paper in October 2008,and when the term moved into wider use it was originally block chain, before becoming a single word, blockchain, by 2016. In August 2014, the bitcoin blockchain file size reached 20 gigabytes.In January 2015, the size had grown to almost 30 gigabytes, and from January 2016 to January 2017, the bitcoin blockchain grew from 50 gigabytes to 100 gigabytes in size.

There are three phases that blockchain technology went through:

The First phase: blockchain 1.0 related APP which started with digital currency, mainly include the ideal money like Bitcoin, it is one of the most successful application in blockchain technology.

The second phase: blockchain 2.0 was started with digital assets, can be understood as the application of other financial area. Including the blockchain industry standards that Wallstreet bank currently wanted to make. That is, enhance the effectiveness of bank payment and settlement, and decrease the cost of cross-border payment; Exchange trying to use blockchain technology to realize fuctions such as share and transfer attornment.

The third phase: blockchain 3.0 put the blockchain into the area out of financial area, which covers multipal sides in human society, including the use of recording management,Intellectual Property Management, Internet of things, education applications and government administration. In all kinds of social activities, to realize the self-proof of information, no longer depends on a third person or institution to gain trust or establish credit, and improve the operation efficiency of the whole system.

The traditional banking faces three challenges:

One is monetary policy compression bank profit margins after the international financial crisis, central Banks launched quantitative easing and negative interest rates policy respectively, make bank spreads narrowed, challenged profitability and sustainability of traditional banking credit business.

Second, the regulatory standards continuously raise the cost of bank management international regulatory reform to constraint the risk-taking behavior of banking unnecessary and irresponsible, regulatory standards tighten make bank capital added pressure and compliance management costs continue to increase, coupled with the recent international capital markets being such as the European (Brexit) off the impact of the political and economic factors, dropped the valuations of banking, capital supplement capability is restricted by further.

Third is science and Technology Finance (Fintech) to seize the bank’s living space. The trend of Internet banking financial disintermediation is further evident, more technology companies to replace the traditional financial institutions to provide more personal savings, loans, investment, payments and insurance services for consumers to use financial technology. Data show that the global financial technology company has exceeded 2000, while the April 1, 2015 was only 800, the banking industry is the inherent territory from outside the system of financial institutions embezzlement.

How blockchain technology used in bank lending industry:

Internationally, more than 20 top global financial institutions in the past two years on the block chain investment funds including Goldman Sachs, Morgan, Citigroup, more than $1 billion, and is accelerating the introduction of private digital currency (such as Goldman has developed a virtual currency itself as “SETLCOIN”), and the national digital currency in the world there (such as Nigeria has launched from the beginning of last year the national digital currency), Britain, Canada and other countries are also on the development of digital currency plans. R3 block chain alliances including more than 60 Chinese financial institutions including 5 Chinese financial institutions, such as Ping An, Zhao shang and Ming sheng, have also begun in-depth research on block chain technology.

In China, many financial institutions have opened on the blockchain POC test, such as the Postal Savings Bank jointly launched IBM block chain asset management system based on micro public bank with the Rae Bank of the joint development of a set of block chain system for clearing and settlement of the two banks “loan loans with particles”. As of March 2017, China Merchants Bank has implemented the technology of block chain to cross-border payment. Shenzhen chain Nationwide Financial Services Inc has released its “ticket chain” product, marking the application of block chain technology to the bill market.

Finance is built on trust, and the credit system is the core of the bank. Block chain technology is often known as a “machine for creating trust” because of its information sharing mechanism, consensus mechanism, data tampering and high transparency. Through the application of block chain technology, banks will rebuild the credit risk system in an all-round way, effectively overcome the problems such as the distortion before the loan survey, the failure in the loan review, and the failure after the loan management. At the same time, compared to the 1 edition and 2 edition signed technology of big data technology, 3 edition block chain technology has great advantages in reducing costs and enhance business efficiency.

What is the newest breakthrough of the application of blockchain technology in lending industry?

Except banks, blockchain technology also be used in P2P lending, which is super popular nowadays. However P2P has boths Pros and Cons for lenders and borrowers:

For lenders

A benefit is that the interest rate (rate of return) that you receive on your funds may be higher that a cash deposit rate through a bank, building society or credit union. In the current low-return environment, this can be appealing.

A disadvantage is that your money is not guaranteed; the Australian government’s financial claims scheme only applies to banks, building societies and credit unions that are authorised by the Australian Prudential Regulation Authority (APRA). These institutions are known as authorised deposit-taking institutions (ADIs).

For borrowers

The interest rates on offer are also a benefit for borrowers as you may be able to secure a personal loan at a lower rate than your bank will offer. Don’t take that for granted though — it’s important to thoroughly research all your options.

The speed of the application process is also a benefit. P2P lending is essentially digital disruption of the institutionalised banking system and the www is its home. As such the online processes tend to be smooth and efficient.

One disadvantage of P2P lending is that it’s limited. Currently in Australlia P2P lending for general consumers is limited to personal loans. As such if you’re wanting to buy a house, it’s off to the mainstream financial institutions you must go.

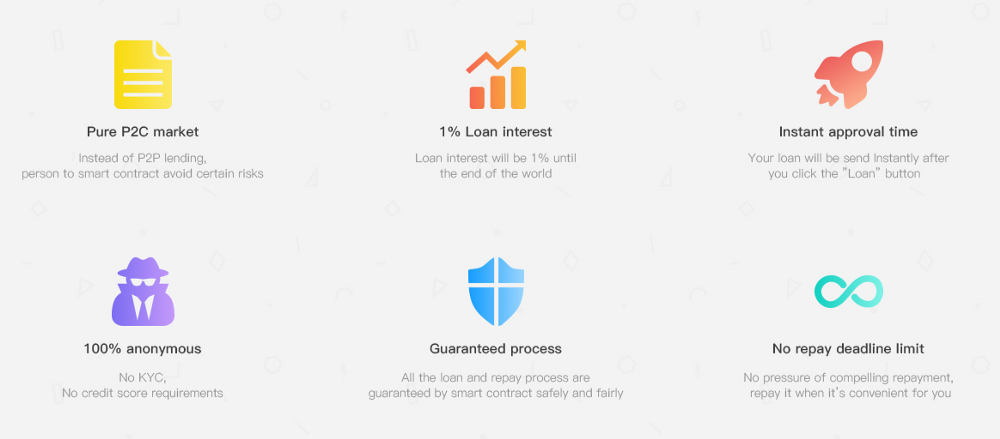

However here is another platform that can be seen as the unique one: Eash P2C lending platform:

With all these outstanding charateristics, Eash has become the most promising ICO project in 2017, it is aslo the revolution of lending industry, a sublimation of using blockchain technology. Don’t miss Eash’s ICO on Dec 2017, you will love it!

MVP of EASH is up and LIVE, you can click here to try now: app.eash.io

Note:

— You need to have MetaMask (Chrome/Firefox) browser plugin in order to make transactions.

— The smart contract is deployed on Rinkeby testnet.!

Hello!