Rent-To-Own Scam Study- How Much You Are Actually Getting Ripped Off

Initially I looked for local privately owned rent-to-own centers in my area , but came up short. This is most likely because in my middle class suburban area, these places are not profitable and competition from bigger chains like Rent-A-Center, makes it hard to survive. In the end I decided to contact the local chain of Rent-A-Center which claimed to offer the best deals on rent-to-own merchandise in the area.

First, what is a typical rent-to-own plan and how does it work? According to investopedia.com, a rent-to-own plan is simply “An arrangement between a consumer and a seller that allows the consumer to rent furniture, appliances and other goods for a defined period of time.”(Investopedia.com) A typical plan would consist of paying a set amount either weekly or monthly, depending on various factors and ownership would be relinquished to the payer after a defined amount of payments. These types of transactions are seen as high risk due to many of the people who participate having a lack of good credit and most use it as an alternative to getting a loan.

![]()

The Rent-A-Center I contacted was a branch about 15 minutes away from me in, New Jersey.However, a quick Google search for the phone number lead to listings of over 30 locations within an hour drive of me, leading me to believe Rent-A-Center is the dominant rent-to-own center in my area. The company itself is publicly traded on the NASDAQ and according to Reuters, operates almost 3000 stores throughout the United States, Canada, Mexico and Puerto Rico, while also accounting for 35% of the rent-to-own market in the United States.(Reuters.com) The store itself offers everything from furniture and appliances to electronics and gaming systems. I talked to a woman named Stephanie and although she was helpful, she basically said I would need to either go onto the website or visit the store to apply for a plan. The few questions I did ask were if Rent-A-Center offered plans to students, if they did a credit check or if you even needed an income to enter into a plan. According to her they do rent to students, however whether or not they do a credit check or if you need an income is totally dependent on which plan you chose.

I then went to the website to check out some of the plans offered by Rent-A-Center and found out they offer three types of purchase plans, a flat out cash purchase, a 90 day interest free plan and finally a RAC flex plan, which offers a weekly payment option without a credit check. The 90 day interest plan was pretty straight forward if paid on time, but an asterisk at the bottom of the page indicated that if not paid on time you would be responsible for paying the monthly interest rate for all the months you received interest free. For the 90 day free interest plan it states that credit score would be checked upon application. If they actually do this who knows.

The RAC Flex plan seems to be their main product which boasts no credit checks, pay as you go, and a flat rate interest fee for everyone. This plan sounds great right, but upon further inspection the asterisks start to pile up. For example, there are service fees, installation fees, late payment fees, and exclusions for certain products. Worst of all they don’t even specify any of the fees unless you have the contract in front of you at the store. In order to sign up for this plan all that was needed was a verifiable income at minimum wage and four references who would be able to assist customer service if they had trouble contacting you if payments stopped. I wanted to see how much the costs of renting-to-own a standard item like a Playstation 4 would be so I examined the payment plan.

The price for the Playstation 4 weekly was 29.99 or 129.99 monthly, both including late fees if your payment was made past the deadline, within 2 months. If a payment was later than 2 months, information would be turned over to the authorities and either a repossession of the item would take place or a court order would be issued. The amount of payments needed before the Playstation 4 would be completely paid off would be 52, which with tax would amount to over 1600 dollars. Compared to newegg.com, which sells a Playstation 4 for about 400 dollars, the rent-to-own plan at Rent-A-Center would cost four times as much! Essentially you are looking at around a 400% annual percentage rate for renting from Rent-A-Center.

Although this plan seems ridiculous, Rent-A-Center does offer many programs available to the renter if payments become overwhelming. For example a customer can stop making payments at any time they want if they feel the program is not right for them free of charge, as well as freeze the payments and resume them at any time. However that being said, Rent-A-Center purposely keeps the real price of items relatively secret and prices everything on the site as weekly or monthly. I only was able to find out how many months the item would have to be paid before owning it by contacting the store itself. In my personal opinion I think Rent-A-Center does not want you to ever finish paying off the item because they make more money by having you stop making payments and returning the item.

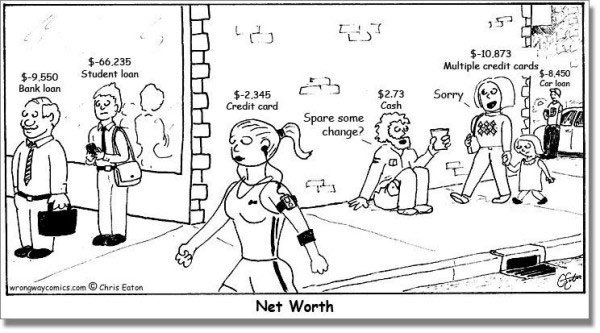

Rent-to-own centers provide a service, but is this service in question a form of predatory lending? Each situation is different and it is hard to distinguish whether or not a particular situation constitutes being called predatory. I strongly believe that Rent-A-Center is taking advantage of the poor and credit-lacking as a business model, but the majority of items they sell are not necessities. In one way it could be considered a type of predatory lending because they seem to hide information about how much the item would eventually cost, but it also should be the consumer’s responsibility to ask. In conclusion I think most rent-to-own plans are probably extremely overpriced and a rip off, but I don’t think they predatory if the information about the purchase is readily available. Its a scam no doubt, but like I said most of the things they offer in the store are luxuries.

-Calaber24p

Debt is slavery.

Unfortunately, many of us choose to be slaves for a little bit of comfort.

Its sad but true, I love this political cartoon, always makes me laugh a bit, but also cry at the same time.

Ah yes, one of my favorites. Have you read The Daemon and Freedom TM by Daniel Suarez (I have an old post reviewing his books, if interested)? It basically has a dark web version of exactly this cartoon where hackers know everyone's balance using special glasses. They Live! type stuff. I love it.

Great evaluation and good topic to share. I think it's the "fast-food mentality" which says give me what I want now even if I have to pay more for it later. For this matter, they pay more in money, with fast food they pay for it with their health.

Completely agree. Its the same reason so many people get hosed on ponzi schemes and high investment return scams. People cant be bothered to wait a small amount of time for the larger pay off when they can get it here and now. The sad thing is you end up waiting anyway by just living life, so its pointless in the long run. Thats why we have so much credit card debt in US.

Sad how low income communities are usually targeted instead of receiving a helping hand.

Next time you are about to throw away electronics or furniture, consider giving it away or reselling it.

Don't donate to Goodwill or other companies that are just out to make a profit.

Yeah, these companies are like scavengers picking up the last bits of flesh on a carcass. There is hardly any money in these poor communities and rather than enriching it, these companies pull even more money out of it.

It cannot be denied that consumer has a responsibility to ask complete implications of a transaction. But we should not be fooled, at some point these businesses bait such people who're prone to make rash financial decisions, as this demographic appeals there balance sheets the most.

Yeah sadly, like I said you wont find these types of businesses in wealthier areas, you only find them in poor ones. People who have no money sense are the only ones who are going to rent a ps4 for 129.99 a month. Plus half the time they put it on a credit card so they are paying even more as well.

These types of arrangements raise a host of issues from a consumer protection standpoint.

Legally speaking, a rent-to-own agreement does not involve "credit" and therefore does not trigger the protections afforded under the federal Truth-in-Lending Act. That being said, many states have recognized the predatory nature of these types of transactions and have enacted laws that require the same types of disclosures that accompany a typical credit agreement.

So while it might not be considered predatory in New Jersey, it can be in New Hampshire. The Department of Justice published an excellent resource on subject, which is available here.

Great article. I think the picture where it offers payday loans says everything. Payday loans have an APR of 400%-5,000% and are a truly terrible thing for low income people. They advertise relief, but promise debit and bankruptcy. It's sad that businesses like this are allowed to target those who are already struggling.

These places are HUGE scams! People need to stay as far away from them as possible.

I sell furniture in Savannah, Ga. My store is a Family Run and Operated for almost 75 years. We used to write our own paper "loans", but the Rent a Center mentality is something we had to deal with when the Savannah Stores opened. My main question is ,"How much is this a week". I started managing my own store and try very hard to explain the pitfalls of financing with a lease payment company. Rent a Center is actually inside of Ashley Homestores and Rooms to Go and is doing the same thing in those store. They set up this system to expand the type of furniture they have available in the Rent To Own outlet stores. When a customer cant pay.......its repoed......they are penalized and resell the stuff for the same price...they always get paid. The company I use reports to EQUIFAX and while its the same concept....they build credit. Rent A Center wants you as a customer for life........they want you stuck with them...its beyond a scam. I left working at an Ashley Homestore after my boss said that "I never told you that RAC Acceptance went on their credit".......and yes he did.....and my customer paid it off in ninety days.....but has nothing to show for it, except for the furniture.

Too many people only think in terms of what monthly payment can I afford. If they actually ran the numbers they would realize it is a lot cheaper to wait and save up the money.

Having worked inside the business for nearly a decade I'm afraid your article addresses some simplistic truths while ignoring the revelations of honesty. It's funny how the mindset of the masses follow what is believed to be "common knowledge".

The unforgiving truth is that Rent-A-Center and rental purchase agreements as a whole do not compete on even ground with the all mighty dollar. (Cash is king and always should be!) There can be an argument made for the value that most rental companies offer through their services. Most stores offer a cash option, while this cash option is almost always higher than you'll pay in a retail establishment, it does include delivery, setup and service plans. The cash option period can extend from 90 days all the way up to six months. There are times where you can find a television with little to no wear that has been discounted down under "retail" pricing that will include additional warranties up-to 4 years for parts & service. It is often overlooked but I thank you for referencing one of the biggest advantages to using RTO is that the customer can cancel for any time and any reason. This is not a luxury provided by a more affluent customer that gets buyers remorse or was unfortunate enough to place a purchase on a credit card that can no longer be paid. By the way, do the math on a $1,800 purchase with only minimum payments being made at a 24% interest rate and tell me who the real crooks are. I promise it will surprise you.

The "flex pay" plan that you reference is the rent-to-own option and the most expensive option of 3 that most stores offer. I can assure you that stores don't want you to return these agreements. There is no scam involved. There are many less fortunate, hard working people that can't provide what so many people take for granted. Whether it's a functional laptop for a child that needs it for school, a washer and dryer for basic daily cleanliness or a place to sleep when the alternative is the floor, these stores accept folks that most people don't even want to interact with. Much less trust them with thousands of dollars of product that can be delivered same day with the customer's "word" they'll make their payments on time or return the products in a condition that makes them able to be re-rented.

Many states have their own regulations on the RTO industry and I'm fairly certain that all states require a quasi-full disclosure that is much more simple to understand than you would have your readers believe. Not only is the maximum possible amount listed on each price tag but the rental lease itself discloses this amount. This is a very standard practice not only for RAC but even mom and pop stores countrywide.

In closing, there are many people who have acquired high quality durable home goods using the rto model that otherwise would not have access to credit or the financial means to do so. This service undoubtedly costs more than if a consumer had purchased the goods outright but in many situations cost less than financing an item and making minimum payments to a credit lender. There are a number of companies worldwide who now offer leasing services because of the simplicity of the design including Sears, Big Lots, and numerous online web based businesses.

I don't buy $8 coffee, but to some people it's justified. That doesn't make the $8 coffee a "scam". Is that predatory to the superficial?