FACILITATING INNOVATION IN CREDIT FACILITY

Facilitating Innovation in Credit Facility

Nothing can be achieved without finance. Practically nothing! But there’s a lack of it among individuals with ideas capable of making the society better than it currently is. The credit facility was born out of this need. Giving loans has its fair share of problems. There’s the need to confirm that an individual is capable of doing what’s right when the time comes. Also, credit providers have to deal with rectifying the accounts of recipients and collating information of potential ones. These are not easy tasks. While many might not be aware, the use of collaterals in granting loans was trendy at some point. The credit industry has indeed come a long way.

Challenges Facing the Credit Industry

The credit industry has lots of issues troubling it. One of the most pertinent is the unbalanced nature of information in the sector. This has led to the creation of a center with information acting as the middleman between the lenders and the borrowers. What happens next? Borrowers are left feeling burdened by higher interest rates, and their lending counterparts are reeling from been cheated so brazenly.

Having a centralized credit industry gives rise to various flaws which will only have a negative effect on every party involved. Like every business, there are good customers and bad ones. Normally, a lender should find a way of recovering debts from the bad ones. In a centralized credit industry, the good customers, who are known to pay regularly, will have to bear the brunt of the noncompliance of the unscrupulous ones. Lenders aren’t spared either as their revenues are cut short to make up for the loss.

The current structure in the credit facility sector is uneconomical and perhaps reckless. Excess time is spent on frivolities. One of such is the idea of assisting potential borrowers to confirm if they are qualified for a loan. There should be metrics which assist these individuals to do it themselves. No one should be spoon-fed at the expense of more resourceful tasks on the to-do list of those involved.

There is one thing which every enterprise have in common – profit making. The credit industry is no exception. Financial establishments, created to offer financial solutions to customers, have drifted from their actual purpose due to the increased possibility of more profit offered by posing as intermediates. They shortchange the lenders while extorting customers. This creates a vicious cycle where everyone wants to get on the gravy train without considering the affected parties.

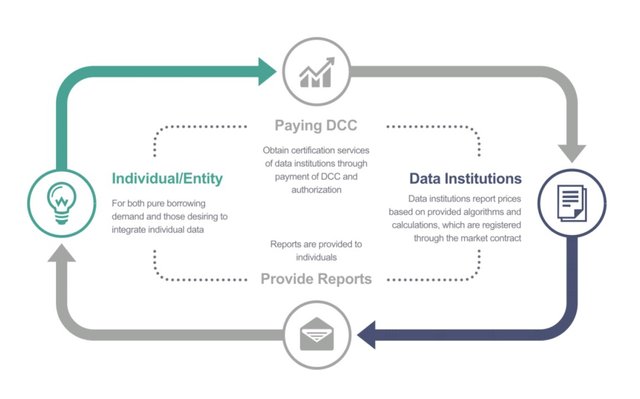

No doubt, a credit report is essential. You can’t have a credit facility without the accompanying glowing report to back it up. But humans will always be humans. So, borrowers tend to tell half-truths and withhold information from the lender. This only complicates the problem in the industry. There is a need for an exhaustive credit report which is objective and accurate. However, this is currently unavailable due to the lack of a harmonized data center, and many lenders have to shoulder this responsibility themselves.

Light at the End of the Tunnel

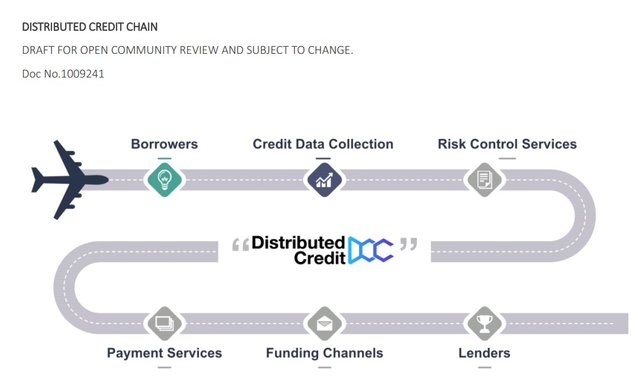

With the emergence of blockchain technology, there is hope for the credit industry. However, this will only spell doom for the intermediaries skimming off the effort of the lenders and genuine parties in the sector. The Distributed Credit Chain (DCC) is built on this innovative technology to ensure every stakeholder in the sector doesn’t feel cheated. The DCC will operate like an open market where participants can choose who they do business with. There’s no longer the need to accept just about any dick and harry just to improve your profit margin (for lenders) or out of desperation.

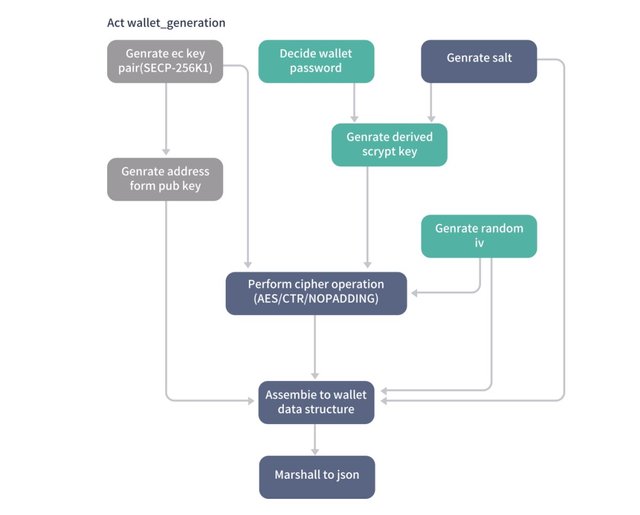

The DCC reduces the possibility of data theft due to the added advantage of cloud storage and encrypted data exchange. Users of the platform can carry out transactions without zero risks of loss of sensitive data which is a growing menace in today’s world.

With the DCC’s entry into the credit facility industry, middlemen are going out of business. Its theft proof platform ensures only the parties involved have access to shared data. No third party will be exploiting anyone since the centralized way of doing things in the sector has gone extinct.

The DCC ensures borrowers wouldn’t have to prove themselves multiple times to receive credit. The DCC platform, with the aid of blockchain technology, provides a credit report which with the consent of both parties can be utilized by other lenders in the future.

For the continued survival of the DCC platform, the DCC monetizes several tasks within its platform. Here, the DCC token is the medium of exchange. Every transaction which involves the interaction between the lenders and borrowers attract a nominal fee. With the DCC’s strong ties to the blockchain technology, these payments are transparent, and users don’t have to worry about hidden charges.

TOKEN INFORMATION

Token Symbol =>DCC

Total Supply=> 10,000,000,000 DCC

This is ERC20 token launched on Ethereum Blockchain network.

TOKEN DISTRIBUTION

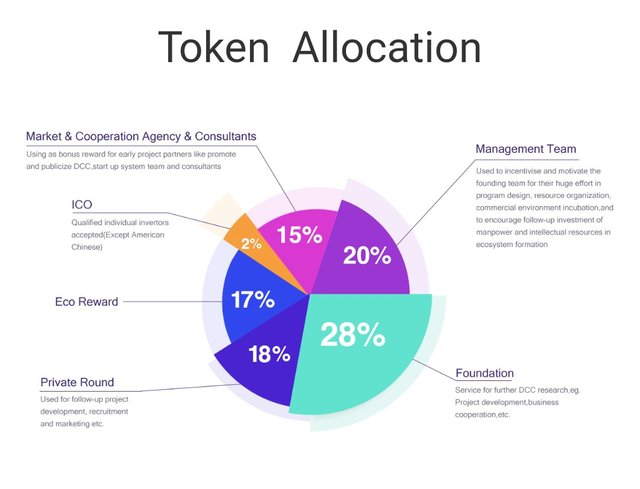

1,800,000,000 has been allocated to Private round which is 18% of the total supply.

200,000,000 has been allocated to ICO which is 2% of the total supply.

2,800,000,000 which is 28% has been allocated to the foundation which will be used for research and further development of the platform

1,500,000,000 which is 15% has been allocated to Marketing and Cooperation

1,700,000,000 which is 17% has been allocated to eco-reward

2,000,000,000 has allocated to management team which is 20% of the total supply

FUND DISTRIBUTION

30% Allocated for Labor cost

25% Allocated for marketing

10% Allicated for business cooperation

5% Allocated for consultancy

5% Allocated for ecosystem Operations

25% Allocated for a reserve fund

TEAM

For more information about the team, Check below

Stewie Zhu=>

Serial entrepreneur

Founder of TN Tech

Ph.D. candidate in Finance at LSE

M.S. in Financial Economics, Oxford University

M.S. in Statistics, Yale University

Stone Shi

TELECOM, Ingenieur

Former vice president at JP Morgan Chase

Nanjing University, Computer Science/Math

Nanjing University, Electronic Science, and Engineering

Dr. Daniel Lu

Ph.D. in Mathematics, Yale University

Postdoctoral Research in Financial Engineering, focusing on the Representation Theory, University of Leipzig, Germany

Advisors

Yu Chen

Partner of JX Capital

Famous angel investor

KOL in China with the net name as “Jiangnan Young Cynic (Jiangnan Fen Qing)”

Ming Yao

CTO of CCX Credit, the pioneer of China's domestic rating industry

Worked at Bell Labs, years of experience in big data technology

Zhiwu Chen

Former Professor at Yale University

Research Director at Hong Kong University

One of the most renowned and influential Chinese economist

Henry Cao

Renowned financial economist

Professor in CKGSB, finance

A former professor in UCB and UNC

Matthew Chang

Managing Director of KKR

Leading expert in the areas of private equity, fixed income, and capital markets

Former global senior partner at Roland Berger Strategy Consultants

EXCHANGES & PARTNERS

ROADMAP BELOW

USEFUL LINKS

Token=>http://dcc.finance/token/index.html

Explorer=>http://explorer.dcc.finance/

Website=>http://dcc.finance/index.html

Whitepaper=>http://dcc.finance/file/DCCwhitepaper.pdf

Facebook=>https://www.facebook.com/Distributed-Credit-Chain-425721787866299/

Twitter=>https://twitter.com/DccOfficial2018/

Telegram=>https://t.me/DccOfficial

Bitcointalk ANN=>https://bitcointalk.org/index.php?topic=4185316.0

Bitcointalk Profile=>https://bitcointalk.org/index.php?action=profile;u=1328480;sa=summary

Bitcointalk Username=>Lekatoo

Author=>Lekatoo