Can Bitcoin Be Gold 2.0?

Summary

- As central banks across the globe actively manufacture inflation, why investors are (once again) turning to gold.

- A look at Bitcoin as an alternative to gold in the role of a 'non-paper' currency and 'storage of value'.

- Bitcoin's viability as an investment: market transparency, liquidity, security and volatility.

- A practical look into Bitcoin exposure and related investment vehicles.

In my previous article 'Inflation: The Beast in the Cage' we discussed how central banks are purposefully manufacturing inflation in the hopes of countering the global economy's prevailing deflationary headwinds, and the ramifications this could have for fiat currencies (currencies issued and backed by central banks).

While there is some evidence QE and easing monetary policies have helped spur growth, there is also increasing cause for concern that the continuation of these policies will do more harm than good. Already, these policies have largely acted as a 'reverse wealth redistribution' that has increased wealth inequality while also compromising central bankers' credibility. This standoff of central banks vs deflation can only end in one of two ways: central banks eventually admit defeat to deflation- or the markets force them to by questioning their credibility to make an impact- or central bankers successfully create inflationary conditions.

The possibility of either outcome has driven some investors to look for alternatives to the paper currencies backed by these central banks. Traditionally this alternative option has been gold, but in this article we'll look further at why this is, and also discuss the investment viability of a potentially revolutionary newcomer to the 'alternative to paper currency' and 'storage of value' scene Bitcoin. There are a growing number of Bitcoin related ETFs and investment vehicles that investors in gold and Bitcoin alike should be aware of, including ARKW, OTCQX:GBTC and (most notably) COIN.

Why Gold?

To understand the value of gold as an alternative to paper currency, one must first understand what currency is (and isn't). A currency has the following characteristics:

- It serves as medium of exchange and account

The function of currency is to facilitate economic exchanges. A farmer looking to sell one of his cows to the blacksmith in return for horseshoes has a problem if he doesn't need the exact number of horseshoes the cow is worth. Currency- by being easily divisible and neutral of value with respect to the parties in the transaction (unlike barter where value of payment is directly impacted by each parties preferences)- allows for easier and more efficient exchanges. Of course for this to hold true a currency must have wide acceptance and availability (otherwise it would no longer serve to make exchanges easier). - It must act as a 'storage of value'

A currency must have a fixed or controlled level of supply that contributes to a consistent value. If there were unlimited amounts available to everyone at any given time, obviously a currency would become worthless, but a limited supply alone is not enough, it must also be relatively stable. Otherwise, if amounts of currency available fluctuated wildly from day to day, and thus- all else equal- its value would significantly fluctuate. To return to our example, in such a case the farmer would be less willing to sell his cow for money because if the value of that money fluctuated wildly, when he most needed to buy hay to feed his animals that money might not buy what he needs- it would be safer and preferable to him to keep his wealth in the form of something with a more stable and known value, such as his cow. Without a value that is easily protected and relatively stable over time, the usefulness of a currency quickly breaks down, and when it no longer serves its purpose it is abandoned, like former currencies which have become obsolete and extinct due to hyperinflation.

Both conditions must be met to be a currency: things which generally hold their values but are not commonly used to facilitate transactions (homes or collectibles for instance) have the same basic issues as our rudimentary example: their values are highly dependent on the specific parties in the transaction. Likewise, things which are used for transactions but which do not store value- like a formerly stable currency now undergoing hyperinflation- quickly lose any practical function and usefulness as a currency. These criteria are why precious metals such as gold and silver were among the first forms of currency ever; gold is divisible but uniform in its properties from piece to piece, widely accepted, relatively scarce, and non-perishable.

Today, gold as a holding can be thought of in two ways: 1) as an industrial commodity and 2) as a currency. Often people refer to gold as a commodity even when the aspects of gold they have in mind have more to do with its functions as a currency.

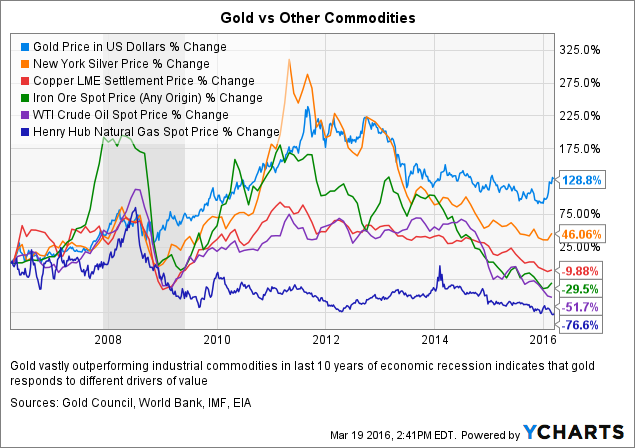

While gold has an industrial purpose that drives a portion of its value (just like other commodities: crude oil, iron, coal etc), evidence suggests that in many ways it is more appropriate to think of gold primarily as a currency. Like a currency, some government banks may pay interest on gold deposits, gold can be lent to borrow USD for more favorable or even net negative borrow rates (akin to a FX swap or forward), and spot gold literally trades as a currency exchange rate in the OTC Forex markets just like EURUSD or USDJPY trade. But perhaps the best indication that gold is unique amongst commodities and behaves fundamentally differently is how it has behaved vs other industrial commodities in the last ten years.

Gold Price in US Dollars data by YCharts

Though there is no 'intrinsic value' to gold as a non-commodity (at least no more than there is to the cotton fibers of a freshly minted Benjamin), gold derives a non-commodity value from its acceptance and function as a currency like the Euro, Yen, Yuan or Dollar. Gold is universally valued, divisible, fungible, scarce, securable, and non-perishable. Yet, unlike paper currency, gold's supply is governed by factors other outside the realm of central bank monetary policy, in fact it has been used as a currency for thousands of years before central banks even existed. And this is exactly why investors turn to gold when concerned about inflation, weakness in 'paper' currencies, or central bank credibility- it acts as an alternative 'storage of value' and has served in this capacity for quite some time.

Bitcoin vs Gold: Does Bitcoin Offer the Same Benefits?

Like gold, Bitcoin is divisible, universally consistent from one unit to another (fungible), and fixed in its available supply, with the rate of growth of the supply controlled by forces other than central bank policy. But can it provide investors the same potential benefits as gold? To answer that, we need to critically examine whether Bitcoin is actually a new form of currency, or something else entirely.

Criteria #1: Does Bitcoin serve as a medium of exchange?

The short answer is yes, to a sizeable and growing number of businesses and marketplace participants Bitcoin is an accepted or even preferred form of payment and exchange. Currently, an estimated 120-150 thousand businesses accept Bitcoins, including companies as large as Dell, DISH, Expedia, Overstock.com, and even nonprofits such as the Red Cross.

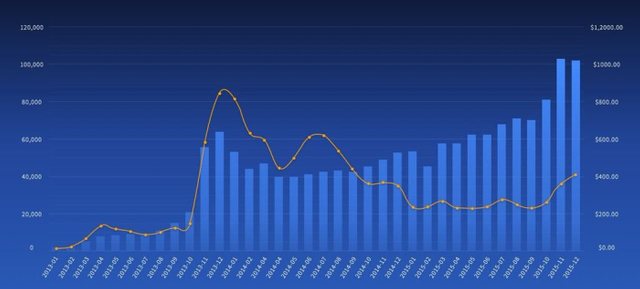

n line, with this growth in companies which accept Bitcoin, both the number of transactions per day, and the total dollar amount of those transactions, have steadily grown, even as Bitcoin prices themselves have fallen from all-time highs.

The total number of daily transactions (transactions, not trades on exchanges) in Bitcoin has steadily been on the rise and today measures in the several hundred thousand.

Bitpay's total dollar amount of transactions have continue to steadily grow despite falling prices.

Given the wide rate of Bitcoin's usage for conducting transactions, and the rampant rate of growth of that usage, it seems fair to say that Bitcoin does serve as a medium of exchange.

Criteria #2: Does Bitcoin act as a storage of value?

Answering this second question is a bit (no pun intended) more difficult and subjective. Compared to gold and paper currencies, Bitcoin has a very short history which makes it difficult if not impossible to answer whether Bitcoin can act as a long-term storage of value. Remember, gold has been used as a currency for several thousand years while Bitcoin has existed for less than a decade.

Bitcoin does however posses some of the prerequisites necessary for something to act as a storage of value:

- Bitcoin has a fixed total supply

- Bitcoin has a steady rate of growth in the supply that does not lead to wild fluctuations in the total supply

- Bitcoin transactions are virtually impossible to counterfeit

Together these factors mean that the supply of Bitcoins should be stable, which should allow it to potentially act as a storage of value. Yet while these conditions are necessary to act as a storage of value, they are not wholly sufficient. Just because something has a stable supply does not mean it is valuable, value requires there to also be demand.

There is reasonable evidence to support the argument that Bitcoin demand exists, is relatively stable, and is gradually on the rise as Bitcoin is adopted on a broader scale for conducting transactions (discussed in Criteria #1 above), but this answer is still a bit too qualitative for my taste.

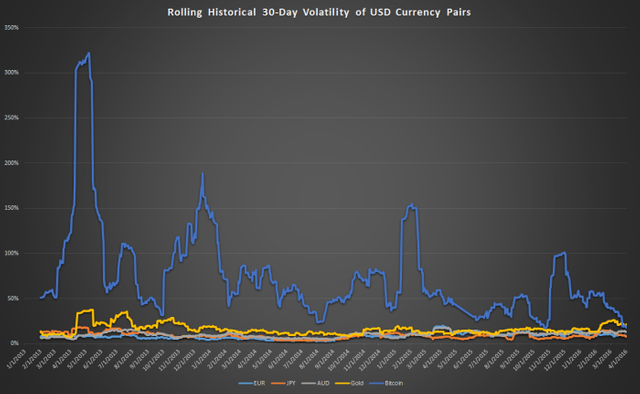

One way we can begin to more objectively answer the question of whether Bitcoin acts as a storage of value is to look at the what the hard data tells us about Bitcoin's volatility compared to that of other currencies. Something that acts a storage of value should have a relatively low volatility- it should remain roughly the same value from day to day and any changes over longer periods of time should be gradual. Thus, by comparing the volatilities of various USD currency pairs, we can begin to see where Bitcoin stacks up.

The above chart displays the rolling historical 30 day volatilities of the Euro, Yen, Aussie dollar (aka the 'dollarydoo'), gold and Bitcoin. As might be expected, historically Bitcoin's volatility has been vastly higher than these well established forms of currency, but there are some notable trends. First, Bitcoin volatility appears to be steadily on the decline, meaning that in relative terms it is gradually becoming more of a 'storage of value.' Secondly, and perhaps even more interesting, is that just recently, for the first time in history, the historical 30 day volatility of Bitcoin has dropped below that of gold. One shouldn't rush to make too much of this, but it is a small indication that Bitcoin may in fact have begun to serve in a similar capacity as gold for some investors, in regards to gold's role as a non-paper currency storage of value.

But does that mean Bitcoin is a currency? There is no single answer, but personally, I would tend to say yes. It is used as a medium of exchange by a large and growing number of companies and individuals alike, and using volatility as a proxy for indicating its usage as a storage of value, it seems Bitcoin is rapidly becoming comparable to other currencies. Of course, the major caveat is that Bitcoin's entire history only spans a handful of years, but given that trends indicate a continued growth in usage, and a continued wariness about paper currencies from investors, there are some arguments to be made that investors may be rewarded for the additional risks associated with Bitcoin.

In fact, though it is not without its own distinct problems, Bitcoin does have some areas of advantage over gold. Compared to physical gold, Bitcoin is much easier (at least for tech savvy investors) to purchase and store, with much lower transaction costs for Bitcoin compared to retail players in physical gold (more on that later). Also, since it is electronic by nature, Bitcoin is much easier, faster and simpler to use in everyday purchases and transactions than physical gold. And by some measures, Bitcoin may be significantly undervalued relative to gold.

For example, there are estimated to have been about 6 billion ounces of gold ever mined. At $1,200 an ounce, that means worldwide supplies of gold represent a $7.2 trillion USD value. If we think of those $7.2 trillion roughly as the worldwide demand for non-paper currency, even if we hold it constant and assume Bitcoin is only 1% of this demand, given the current level of about 15.5 million Bitcoins in existence right now, each one would be worth about $4,600 vs their current price around $400.

Obviously this is just a thought experiment and far from the only way to value Bitcoins, but if Bitcoin does become a popular option as an alternative storage of value, comparing it to gold to determine a relative price is a reasonable place to start. Readers should note that I am in no way advocating Bitcoin (or any investment) as right for everyone, or saying that Bitcoin ever should or will replace investors' gold holdings. However, given the evidence, some investors may find that allocating a portion of their portfolios to Bitcoin is an attractive option for much the same reasons they find would invest in gold.

And while actually buying Bitcoins may sound intimidating to retail investors, with recent improvements to trading exchanges and marketplaces, retail investors have a growing number of relatively low cost options.

The Bitcoin Marketplace: Price Transparency, Liquidity and Security

Like the Forex markets and the physical gold markets, the marketplace for Bitcoin is fragmented and OTC (over the counter). Though numerous marketplaces and exchanges for Bitcoin exist, they are disjointed. A central, aggregated source of pricing and liquidity- such as exists for stocks and futures- simply does not exist for Bitcoin, which means at any given time, any two willing parties can agree to buy/sell Bitcoins at any given price, regardless of the prices predominantly being traded elsewhere.

Price transparency, and liquidity, are improving though, with more aggregated sources of information becoming available and the recent launch of Gemini, the first non-tech savvy, retail investor friendly Bitcoin exchange with USD deposits actually FDIC insured.

The above depicts the price of Bitcoin on various exchanges, helping to better pinpoint the fair value of Bitcoins at any given time.

Though daily USD volumes traded in Bitcoin are still quite small, at under $10 million per day USD activity they are less than 1% of daily activity in the popular gold related ETF GLD, transactions costs are quite low compared to physical gold markets for retail investors. With Bitcoin bid offer spreads of just $.01, and the ~25 bps (.25%) fees/commissions charged by many exchanges on trades, investors can expect to pay round trip bid-offer spreads of about .505%, or about $2.13 per Bitcoin at current prices. This is anywhere from 3-10x cheaper than the enourmous big-offer spreads retail investors pay in the physical gold markets.

Another (significant) issue in the spot Bitcoin market is security, which has especially been on investors minds since the Mt. Gox fiasco. Though no form of Bitcoin (or gold) will ever be entirely riskless to hold, with additional exchanges such as Gemini forming in US jurisdictions, and in cooperation with existing financial regulations and consumer protections, risks in Bitcoin are considerably less than the wild west days of Mt. Gox. With increasingly sophisticated biometric verfiication and encryption security protocols offered by leading Bitcoin exchanges and wallets, investors who take the proper steps can virtually eradicate the risk of malicious attackers stealing their Bitcoins (cracking even a 'simplistic' 128-bit encryption key "would still take billions of years to brute force on current and foreseeable hardware.")

A Practical Look at Bitcoin Exposure: Related Investment Vehicles

While a number of Bitcoin related ETFs currently exist for investors who are looking for exposure, and there will likely be more to come, unfortunately those options leave much to be desired. Unlike gold and many other currencies, for which ETFs exist that have historically very closely tracked the spot currency (ex. GLD, UUP and FXE) the currents options for Bitcoin do not track well to Bitcoin spot prices.

One recently launched ETF in the Bitcoin space is the formidably named 'ARK Web x.0 ETF' . Unfortunately, the ETF is not a pure play on Bitcoin, and invests in what it calls 'disruptive technologies.' It's top three holding are currently Athenahealth, Netflix and Amazon, and the portion of the fund that is attributed to Bitcoin does not hold Bitcoins directly, but shares of the 'Bitcoin Investment Trust' .

Sadly, investors looking to cut out the middle man and directly use GBTC to invest in Bitcoins are also likely to be disappointed. Not only does GBTC charge an outrageous 2% fee (extremely high for a passive index fund and 5x times that of GLD's), but even putting the fee aside, GBTC does a poor job of tracking spot Bitcoin prices. This is because unlike other currency ETFs, GBTC has poor mechanisms in place to ensure Authorized Participants can create/redeem shares in a timely manner in order to keep GBTC share prices tied to the price of Bitcoin. This process typically allows Authorized Participants to arbitrage away small price discrepancies as they occur, as occurs for GLD, but unlike the immense physical gold markets, large pools of physical Bitcoin liquidity may not be readily available for would be arbitrages to complete the process.

Thus, GBTC regularly exhibits massive premiums to its NAV of 20-30%, and premiums have been known to even be upwards of 100%, making it an extremely ill-advised method of getting exposure to Bitcoins.

Finally, despite being the most widely discussed ETF linked to Bitcoin's, the Winklevoss' COIN has been held up for several years by regulators. The launch of the twins' Bitcoin exchange, Gemini, may be a sign that this reluctance and red tape is on the decline, but for now COIN remains stuck in the works. Once (or if) it does begin trading, investors would be wise to learn from the examples of ARKW and GBTC, and carefully examine the design of the fund and the mechanisms it has in place to minimize tracking error.

Conclusion

Despite the considerable risks, bitcoin as an investment has many advantages, characteristic of the gold; its best features are not yet widely appreciated as the structure bitcoin is difficult to understand and poorly understood. However, unfortunately, today does not yet exist a universal mechanism for investors wishing to play the volatility of the prices, while not buying bitcoins themselves, so before deciding on such operations, be aware of high prices and other problems already existing funds.